Why is my credit score going down?

A credit score drops when one or more of five things changes: a payment shows as late, a balance went up relative to your credit limit, a new application added a hard inquiry, an account was closed, or an item was added to your file as a derogatory mark. A sixth, less obvious cause is that the scoring model itself changed, which can move your score even when your underlying report did not. The next sections walk you through how to identify which of those happened to you.

The five visible causes account for the vast majority of score drops. The sixth, invisible cause is increasingly common in 2026: the Federal Housing Finance Agency approved FICO 10T and VantageScore 4.0 for use by Fannie Mae and Freddie Mac in 2024, and lenders have been phasing in those newer models ever since. The same consumer file can produce a different score under FICO 8 (still common on free monitoring apps) versus FICO 10T (increasingly used in mortgage underwriting).

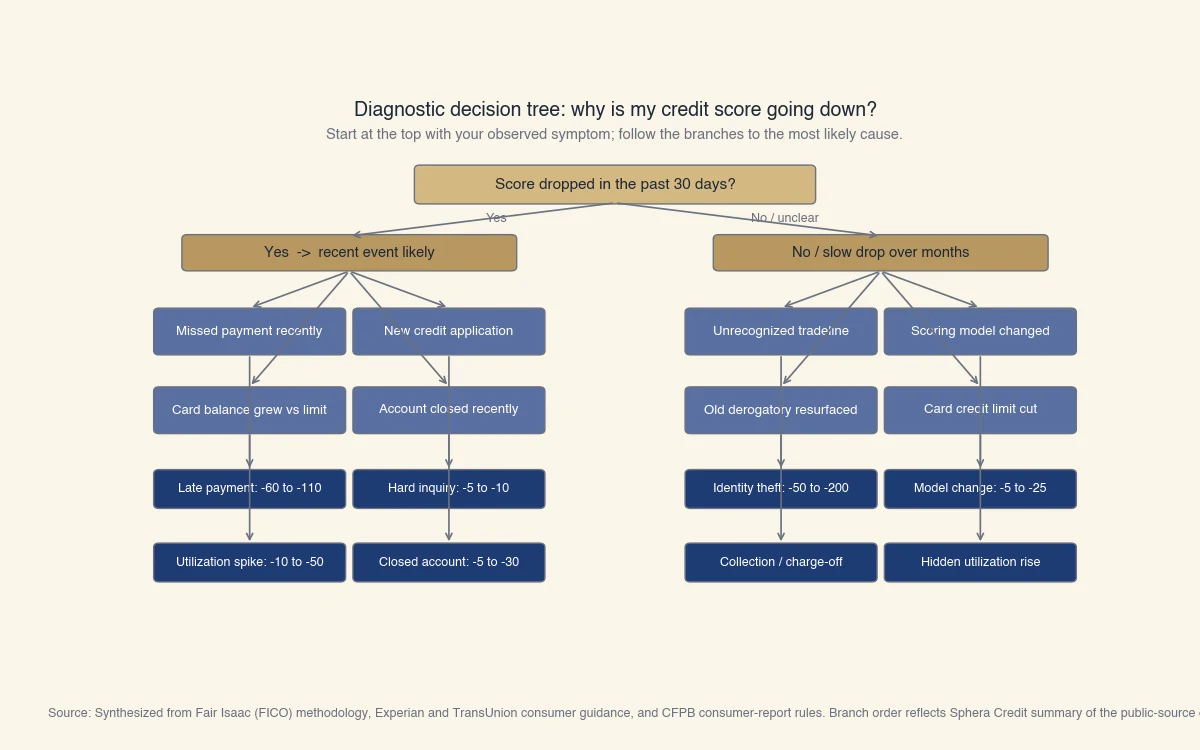

The rest of this page is structured as a diagnostic. Start with the decision tree, then map your observed symptom to a likely cause, then check the specific quantitative impact in the reference table.

Use this decision tree to identify the cause

Start with the most recent change you can observe and follow the branch to the most likely cause. The tree is ordered by frequency: the top branches are the events that explain most score drops.

Source: Synthesized from FICO methodology, Experian and TransUnion consumer guides, and CFPB consumer-report rules. Branch frequencies reflect Sphera Credit summary of the public-source coverage cited inline in the sections below.

Walking the tree linearly:

- Did your score drop in the past 30 days?

- Yes, and a payment was missed in the last 60 days → see "Late payments" below. Typical drop: 60 to 110 points.

- Yes, and a new credit application was submitted in the last 60 days → hard inquiry. Typical drop: 5 to 10 points.

- Yes, and a card balance went up substantially → utilization spike. Typical drop: 10 to 50 points.

- No, the drop happened slowly over months → most likely an account closure or derogatory item that posted with a lag. Skip to the table below.

- Did the drop happen with no observable change to your activity? → model transition or report error. Skip to "Why your score dropped with no change to your report."

How much each event typically drops your score

Specific events have known impact ranges. The table below is what no other top-ranked guide on this topic consolidates: each common score-changing event with the typical point drop and the time the event stays on your file. Ranges come from Fair Isaac's published research and bureau-published consumer education.

| Event | Typical point drop | How long it stays |

|---|---|---|

| 30-day late payment (700+ score) | 60 to 110 | 7 years |

| 30-day late payment (650-700 score) | 50 to 90 | 7 years |

| 60-day late payment | 80 to 130 | 7 years |

| 90-day late payment | 100 to 150 | 7 years |

| New hard inquiry | 5 to 10 | 12 months scoring impact; 2 years on report |

| Utilization moves 30% to 60% | 10 to 30 | Reverses next billing cycle once paid |

| Utilization moves 60% to 90% | 20 to 50 | Reverses next billing cycle once paid |

| Account closed by you (low-balance card) | 5 to 25 | Permanent loss of credit-line capacity |

| Account closed by issuer | 10 to 30 | Stays on report 10 years |

| Collection account added | 50 to 150 | 7 years from original delinquency |

| Charge-off | 75 to 175 | 7 years |

| Bankruptcy filing (Chapter 7) | 130 to 240 | 10 years |

| Bankruptcy filing (Chapter 13) | 130 to 200 | 7 years |

| Identity theft fraud tradeline | 50 to 200 | Removed after dispute under FCRA |

The ranges are population-typical and vary with starting score, credit-file age, and the other items on your file. A consumer with a thin file and a 720 score sees larger drops than a consumer with a thick file and the same 720 score, because each negative event represents a larger share of a thinner file's data.

How long the drop actually lasts

The "how long it stays" column reflects how long the item remains on your credit report under the Fair Credit Reporting Act. The scoring impact decays faster than the persistence. A 30-day late from year one of a 7-year retention loses most of its score weight after 24 months even though the entry stays visible.

Why your score dropped with no change to your report

The most counterintuitive cause: your file did not change, but the model used to read it did. In 2025 and 2026 a growing share of US mortgage and auto lenders started pulling FICO 10T, which reads trended-data (your 24-month utilization trajectory) instead of FICO 8's single-month snapshot. A consumer who carries a high balance most months but pays it down before a single check looks better under FICO 8 than under FICO 10T. This is the "score dropped no changes" symptom that almost every other guide treats as a footnote.

Three flavors of this happen in practice:

- Model transition by your monitoring service. Some free apps quietly migrated from VantageScore 3.0 to VantageScore 4.0 over the past 18 months. VantageScore 4.0 weights medical-debt collections differently and excludes them after twelve months unpaid, but it also treats trended-data on revolving balances differently. A consumer who had no report change can see a 5 to 25 point swing in either direction. The same model-transition gap also affects buy-now-pay-later trade lines: see does Affirm affect your credit score for the bureau-by-bureau picture.

- Different lender, different model. The score your free monitoring app shows (typically VantageScore 3.0 or FICO 8) is not the score your mortgage lender pulls (increasingly FICO 10T or VantageScore 4.0 for conforming mortgages). A 740 on your monitoring app can correspond to a 715 in a mortgage underwriter's view, with no underlying change.

- Score model rollover schedule. FICO is updated roughly every five to ten years. FICO 10 and 10T were released in 2020. The FHFA approved them for Fannie and Freddie purchases in 2024 (FHFA, 2024), with lenders phasing adoption through 2025 and 2026.

How to confirm a model-transition cause

If your score drop has no report-level explanation, pull the same bureau's data on two different sources within the same week. If a FICO-based source shows a 715 and a VantageScore source shows a 740, the gap is the model. If both show identical numbers, the cause is elsewhere on your file and likely buried in a tradeline change you missed.

What can move your score back up

Once you have identified the cause, the recovery path is mechanical: address the underlying event, wait for the scoring weight to age out, and let positive payment history accumulate. Common-path recoveries:

- Utilization spike: pay the balance down below 30 percent of the credit limit. Most score models reflect this on the next monthly reporting cycle.

- Hard inquiry: wait. A single inquiry's score impact fades within 12 months.

- 30-day late: pay the balance, set up autopay so it does not repeat, and let the late mark age. The first 24 months carry most of the score impact; the remaining five years carry diminishing weight.

- Closed account: open a new account only if your overall credit mix needs it; otherwise, do not open new credit just to replace lost capacity. The credit-line loss is real but the recovery from a new account takes 12 to 18 months.

- Derogatory mark you do not recognize: dispute it with the bureau under the FCRA dispute process. The bureau has 30 days to investigate. If the furnisher cannot verify, the item must be removed.

There is no shortcut. Pages that promise "raise your score 100 points in 30 days" are typically selling credit-repair services that work by disputing accurate items en masse, hoping the furnisher does not respond in time. The CFPB has documented this practice in its consumer guidance and the FTC has brought enforcement actions against several of the largest providers. The legitimate version is identifying real errors and disputing them through the standard FCRA channel. For the recovery-path side of this question, see how to boost a US credit score (which tactics actually move which tiers and how fast).

How to confirm exactly what changed

Pull all three credit reports from AnnualCreditReport.com and compare them line by line to your previous month's snapshot. The Fair Credit Reporting Act guarantees free weekly reports from each bureau.

What to look for in the comparison:

- New tradelines: any account that was not there last month. Common: a card auto-converted from store-financing to a revolving account.

- Closed accounts: most issuers do not notify the consumer when they close an inactive card. Closures usually appear in your report before they appear in any email.

- Balance changes: a card balance you thought you had paid may be holding from a reporting-cycle timing gap.

- New inquiries: including soft inquiries from prequalification offers you did not realize were happening.

- Derogatory items: new collection accounts, charge-offs, public records.

- Identity-theft signals: any account that is not yours, in any combination of bureau and product type.

If a tradeline is wrong, dispute it directly with the bureau using the form linked from your report. Under FCRA the bureau must investigate within 30 days, contact the furnisher, and either verify or remove the item.

Bottom line

Most credit-score drops have a single identifiable cause, but the cause is sometimes invisible to standard one-shot guides because it lives in a model transition rather than your file. Use the decision tree to triangulate. Cross-check the point-drop magnitude in the table to confirm. If nothing on your report explains the change, pull two scoring-model views of the same data and compare; the gap is the answer.