A field underwriter's main task is?

A field underwriter's main task is to gather complete, accurate information about the applicant and record it correctly on the application. It is not to assign a risk classification or make the final decision to approve or decline. The field underwriter is the licensed insurance agent or advisor who sits with the applicant, asks the questions, and completes the paperwork. Because they are the first person to assess the risk, the industry calls them the first line of underwriting.

This is the exact point that trips up candidates on the life insurance licensing exam. The common wrong answer is "assign a risk classification to the insured." That is the home-office underwriter's job, not the field underwriter's. The field underwriter collects the facts; someone else at the insurer judges them.

The task breaks down into four concrete duties:

- Gather accurate information. Ask the health, financial, lifestyle, and occupation questions and record the answers truthfully and in full.

- Complete the application correctly. Fill in every required field, obtain signatures, and avoid the gaps or shortcuts that send a file back.

- Observe and document. Note anything relevant the application does not directly ask for, such as an obvious risk the applicant did not mention.

- Submit a clean file. Pass the application to the insurer so its underwriters can assess a complete, honest picture.

Everything a field underwriter does serves one goal: give the insurer a truthful, complete basis for its decision.

Field underwriter vs company underwriter: who does what?

The field underwriter gathers information; the company underwriter decides what to do with it. These are two different people at two different stages, and confusing them is the single most common mistake about this role. The field underwriter is the licensed advisor in front of the applicant. The company underwriter (also called the home-office or formal underwriter) is the insurer's staff member who assigns the risk class, sets the premium, and issues the approve-or-decline decision.

| Task | Field underwriter (the agent) | Company underwriter (home office) |

|---|---|---|

| Meets the applicant in person | Yes | No |

| Gathers and records information | Yes, this is the main task | Reviews what was gathered |

| Assigns the risk classification | No | Yes |

| Orders medical exams or reports | Requests them | Reviews and requires them |

| Sets the premium | No | Yes |

| Approves, declines, or rates the policy | No | Yes |

| Issues the policy | No | Yes |

Read the licensing-exam question through this table and the wrong answers explain themselves. "Assign a risk classification," "approve or decline the applicant," and "set the premium" all sit in the right-hand column, so none of them can be the field underwriter's main task. The only answer that sits in the left column is gathering accurate, complete information. That is why it is correct.

The division exists on purpose. Separating the person who collects the facts from the person who judges them keeps the assessment consistent across thousands of applications, because the pricing decision runs against one set of company rules rather than the judgment of whichever advisor happened to write the file. For the formal side of that process, see what an underwriter does and what underwriting is.

How does field underwriting work?

Field underwriting runs from the first client meeting to the moment a complete application reaches the insurer, and its quality decides how smoothly the rest of underwriting goes. The advisor is not just filling out a form. They are screening the risk early so the insurer does not spend time and money on a file that was never going to fit, and so the applicant is not surprised later.

A typical field-underwriting sequence looks like this:

- Fact-find. The advisor interviews the applicant about health history, family history, income, occupation, hobbies, travel, and existing coverage.

- Match to product. The advisor checks the applicant against the insurer's guidelines to see whether a fully underwritten, simplified-issue, or no-medical product fits.

- Complete the application. Every answer is recorded exactly as given, with no rounding, guessing, or leaving blanks.

- Arrange requirements. Where the product needs them, the advisor helps set up a paramedical exam, fluid samples, or an attending-physician statement.

- Submit and follow up. The advisor sends the file to the insurer and responds to any requests for clarification.

Consider a simple case. An applicant mentions in passing that they saw a doctor last month about occasional chest tightness but were told it was likely stress. A field underwriter doing the job well records that comment, asks the follow-up questions the application prompts for, and notes the pending or completed tests. A field underwriter who treats it as small talk and leaves it off the form has changed the risk the insurer thinks it is taking. If a claim later turns on that omission, the difference between those two versions of the same meeting is what decides whether the policy pays.

The reason accuracy matters at this stage is that the field underwriter is capturing the raw evidence. Every later step, from the risk class to the premium to a future claim decision, rests on what the advisor wrote down. A vague or incomplete answer here becomes an underwriting delay, a wrong price, or a disputed claim later.

Field underwriting in Canada

In Canada the field underwriter is the licensed life or accident-and-sickness advisor, who qualifies through the Life Licence Qualification Program (LLQP) and is licensed by a provincial regulator. The task is the same as anywhere else, but the framework around it is Canadian, and that framework is exactly what generic international explainers leave out.

To sell life insurance in Canada, an advisor must pass the LLQP, a national qualification program overseen by the Canadian Insurance Services Regulatory Organizations (CISRO). Licensing itself is provincial. In Ontario, life agents are licensed by the Financial Services Regulatory Authority of Ontario (FSRA). In Quebec, insurance representatives are overseen by the Autorité des marchés financiers (AMF). British Columbia, Alberta, Saskatchewan, and Manitoba license through their provincial Insurance Councils. Whichever province the advisor works in, their field-underwriting duty to gather accurate, complete information is a core part of that licence.

There is a specifically Canadian reason accuracy carries weight: the contestability period. Under provincial insurance legislation, an insurer can generally contest a life policy for material misrepresentation during roughly the first two years after it is issued. If the field underwriter recorded a health or lifestyle fact incorrectly, a claim in that window can be challenged. Careful field underwriting is what protects the eventual payout, and those payouts are large. Canada's life and health insurers paid a record $143.3 billion in benefits in 2024 (CLHIA). Every one of those claims traces back to information an advisor first recorded at the application stage.

Why does accurate field underwriting matter?

Accurate field underwriting matters because it is the foundation every later decision is built on, and because the industry is automating the rest of underwriting on the assumption that the information coming in is clean. As insurers speed up their back-end decisions, the quality of the data the field underwriter collects becomes the limiting factor.

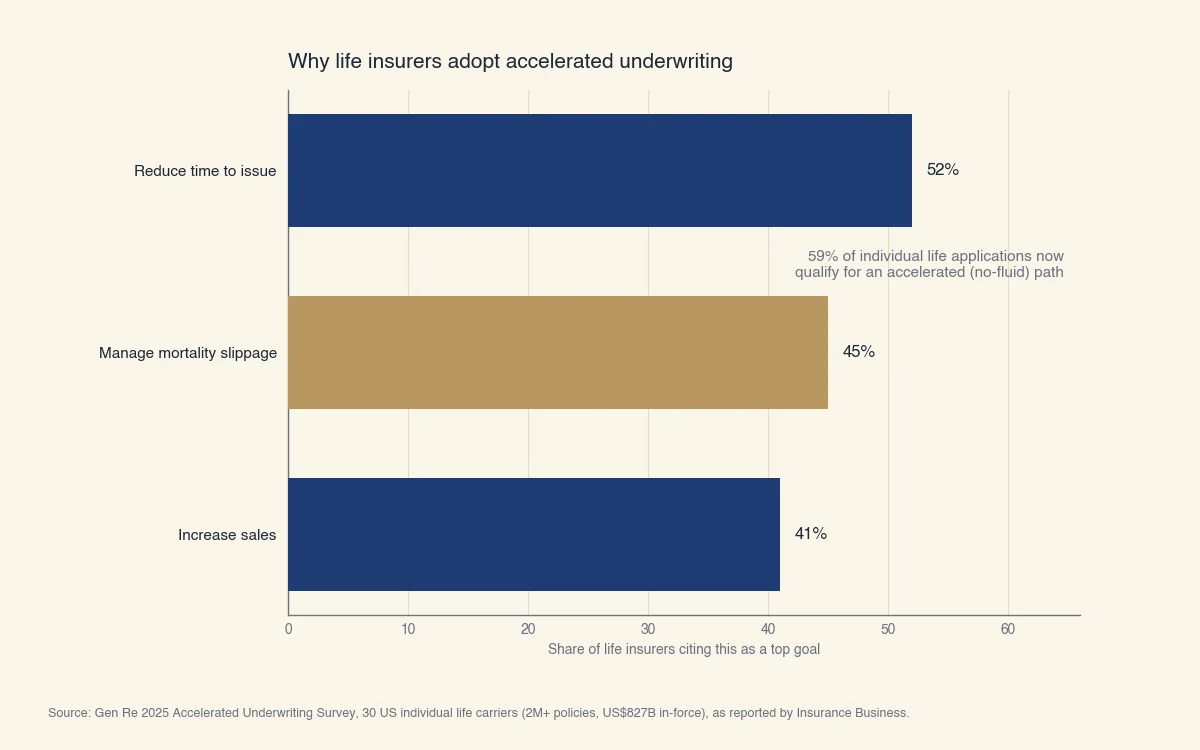

That shift is already well underway. In a 2025 Gen Re survey of 30 US life insurers representing more than two million policies, an average of 59% of individual life applications now qualify for an accelerated underwriting path, meaning they skip the traditional fluids and medical exam. When those insurers were asked why they adopt accelerated underwriting, their top reasons were speeding up policy issue, managing mortality slippage, and increasing sales.

Source: Gen Re 2025 Accelerated Underwriting Survey, 30 US individual life carriers representing 2M+ policies and US$827B in-force, as reported by Insurance Business.

The middle bar is the one that puts the field underwriter's job in focus. Mortality slippage is the risk that lighter underwriting lets under-priced risks slip through, so more claims arrive than the pricing assumed. Insurers manage it by leaning harder on the accuracy of the data they still collect, which is the application the field underwriter completes. Take away the medical exam and the advisor's questions and documentation become the main evidence the insurer has. Accurate field underwriting is what makes fast, automated underwriting safe rather than reckless.

This is the same principle behind good lending underwriting. A decision is only as good as the information it rests on, and the earliest, most human step in the process is where that information is either captured well or lost. At Sphera Credit we build underwriting technology for lenders that focuses on exactly this: assessing each file accurately and explaining the reasons behind every decision, so that borrowers who fall just outside the standard credit box get a careful, consistent read instead of an automatic no.