What does underwrite mean?

To underwrite means to examine a financial risk, price it, and agree to take it on in exchange for a fee. A bank underwrites a loan, an insurer underwrites a policy, and an investment bank underwrites a share issue. In every case the same thing happens: one party studies a risk, decides it is acceptable at a certain price, and accepts responsibility for it (Cornell Law School, LII).

The word is literally about signing under a risk. Underwriting first appeared at the Lloyd's of London insurance market in the 17th century, where financial backers would write their names underneath a description of a ship and its cargo to accept a share of the risk in return for part of the premium (Merriam-Webster). "Under" plus "write" is exactly what they did.

Three related words come from that single idea, and it helps to keep them straight:

- Underwrite is the verb: to assess and accept a risk. "The bank agreed to underwrite the loan."

- Underwriting is the process: the work of measuring and pricing the risk. "Your file is in underwriting."

- Underwriter is the person or institution that does it: the one who signs off. "The underwriter approved the mortgage."

So when a lender, an insurer, or a banker says they will underwrite something, they mean they have looked at the risk, set a price for carrying it, and put their name to the decision.

What does an underwriter do?

An underwriter reviews an application against a set of rules, verifies the supporting documents, measures the risk, and issues a decision: approve, decline, or approve with conditions. The underwriter is the checkpoint between "an application was submitted" and "the institution is now on the hook for this risk."

For a loan or mortgage, a loan underwriter works through a fairly consistent checklist:

- Income and employment. Confirm the applicant earns what they claim, using pay stubs, tax slips, or business financial statements.

- Existing debt. Total up current obligations (cards, car loans, lines of credit) to see how much room is left for a new payment.

- Credit history. Pull the credit bureau report and read the pattern of past repayment.

- Collateral. For a secured loan, confirm the asset is worth enough to cover the debt, usually through an appraisal.

- Fit to policy. Check that the whole picture sits inside the lender's risk appetite and the rules the regulator sets.

An insurance underwriter runs the same shape of process on a different risk: instead of "will this person repay," the question is "how likely is this person, car, home, or business to generate a claim," and the output is a premium rather than an interest rate. Most underwriters specialise by product, so a residential mortgage underwriter, a commercial credit underwriter, and a life-insurance underwriter are three different jobs.

Some of this work is now automated. Simple, low-risk files can pass through a rules engine that scores them in seconds, while files that fall outside the standard pattern go to a human underwriter for a closer look. The decision rules are the same either way, so the split is about which files need judgment, not about lowering the bar. For a closer look at the role inside a lending file, see what an underwriter does.

What does underwriting mean in lending, insurance, and securities?

The verb "underwrite" means the same thing in all three fields, but the risk being accepted and the way the underwriter gets paid are different in each. The confusion around the word usually comes from meeting it in one context and then hearing it in another. This table lines them up side by side.

| Field | Who underwrites | Risk they take on | How they get paid | What the applicant or issuer gets |

|---|---|---|---|---|

| Loans and mortgages | A bank, credit union, or other lender | That the borrower will not repay | Interest on the loan | Money now, repaid over time with interest |

| Insurance | An insurance company | That a covered loss (accident, illness, damage) will happen | The premium you pay | A promise to pay for covered losses |

| Securities (IPOs and bond issues) | An investment bank or syndicate | That the new shares or bonds will not sell at the expected price | The underwriting spread (the gap between what they pay the issuer and what investors pay) | Cash raised from the market, with the sale risk shifted to the bank |

Read across any row and the pattern holds: someone studies a risk, sets a price, accepts the risk, and earns the price. That is underwriting, whichever field you meet it in.

What does it mean to underwrite a loan in Canada?

To underwrite a loan in Canada means the lender measures your ability to repay against national rules, most importantly OSFI Guideline B-20 for residential mortgages, and only approves the file if it fits inside those limits. This is where the abstract word turns into concrete numbers on your own application.

For a residential mortgage, the underwriter checks two debt-service ratios set out in the affordability rules (FCAC):

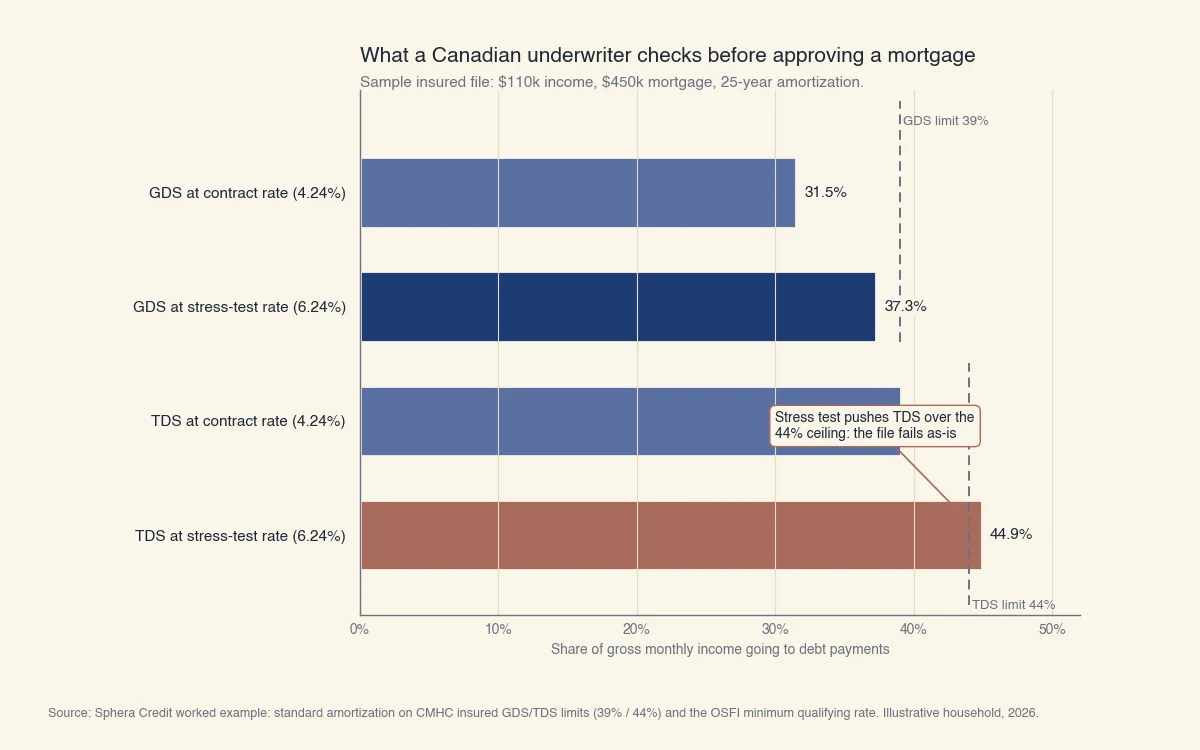

- Gross debt service (GDS) is the share of your gross monthly income that goes to housing costs (mortgage payment, property tax, heat, and half of any condo fees). For an insured mortgage the ceiling is generally 39%.

- Total debt service (TDS) adds every other monthly debt payment on top of housing costs. For an insured mortgage the ceiling is generally 44% (CMHC).

On top of the ratios, the underwriter applies the mortgage stress test. They do not qualify you at your actual contract rate. They qualify you at the higher of your contract rate plus 2% or a 5.25% floor, so that you could still afford the payment if rates rose (OSFI). This rule was left unchanged when OSFI reviewed it in early 2026.

Here is what that looks like on a real file. Take a household earning $110,000 a year ($9,167 a month) buying a $500,000 home with 10% down, so an insured mortgage of about $450,000 over 25 years. At a 5-year fixed contract rate of 4.24%, the payment is roughly $2,436 a month. Add $300 in property tax and $150 in heat and housing costs reach about $2,886, a GDS of 31.5%. Add $700 of other monthly debt (a car loan and a credit card minimum) and TDS is 39.1%. At the contract rate, the file passes both ceilings.

Now apply the stress test. The qualifying rate is 4.24% plus 2%, or 6.24%. At that rate the payment rises to about $2,966, GDS climbs to 37.3% (still under 39%), but TDS reaches 44.9%, just over the 44% ceiling. The file fails as underwritten, and the underwriter would decline it or ask the borrower to clear some other debt or put more money down first.

Source: Sphera Credit worked example. Ratios computed with the standard amortization formula on CMHC insured GDS/TDS limits (39% / 44%) and the OSFI minimum qualifying rate. Illustrative household, 2026.

That single example is the whole meaning of "underwrite a loan": the lender does not just glance at your income, it runs your file against defined rules and a built-in safety margin before it accepts the risk. For the full process behind these ratios, including the 5 Cs of credit, see what is underwriting, and for timing see how long underwriting takes.

Why does it matter to you?

Understanding what "underwrite" means tells you what actually decides your application: not a single number or a gut feeling, but a documented risk assessment against clear rules. When you know that, you can prepare for it. You can check your own credit report first, keep your debt-service ratios low, gather clean income documents, and understand why a lender qualifies you at a rate higher than the one you will pay.

It also explains why two lenders can reach different answers on the same file. Underwriting rules set the floor, but each lender layers its own risk appetite on top, which is why a file that sits just outside one lender's box can still find a yes elsewhere. At Sphera Credit we build underwriting technology that helps lenders make that assessment accurately and explain the reasons behind every decision, so borrowers who fall just outside the standard credit box get a fair, consistent read rather than an automatic no.