Can you sign over or lower a Parent PLUS interest rate?

No. You cannot sign over, reassign, or renegotiate the interest rate on a federal Parent PLUS loan, because the rate is fixed for the life of the loan and the loan legally belongs to the parent who borrowed it. The U.S. Department of Education has no form, election, or process that lets a parent hand the loan, the rate, or the repayment responsibility to a child (Federal Student Aid).

The question hides a common misconception: that an interest rate is a thing you can pass to someone else or argue down, the way you might transfer a car title. A federal rate does not work that way. It is set by statute the year your loan is disbursed and then frozen. Calling your loan servicer to "lower the rate" or "put it in my kid's name" will not work, because the servicer has no authority to change either one.

A Parent PLUS loan is a federal Direct PLUS loan a parent takes out to pay for a dependent undergraduate's education. There is exactly one way to move that debt to your child at a different rate: your child takes out a brand-new private loan in their own name and uses it to pay off your federal loan. That is refinancing, and it is a new loan with a new rate, not a transfer of the old one. Whether a private or local lender can actually offer a lower rate depends on the student's credit and the rate environment, not on anything the parent can negotiate on the existing federal loan. The rest of this page covers what the rate is, why it is locked, and whether refinancing is worth what it costs you.

What is the current Parent PLUS loan interest rate?

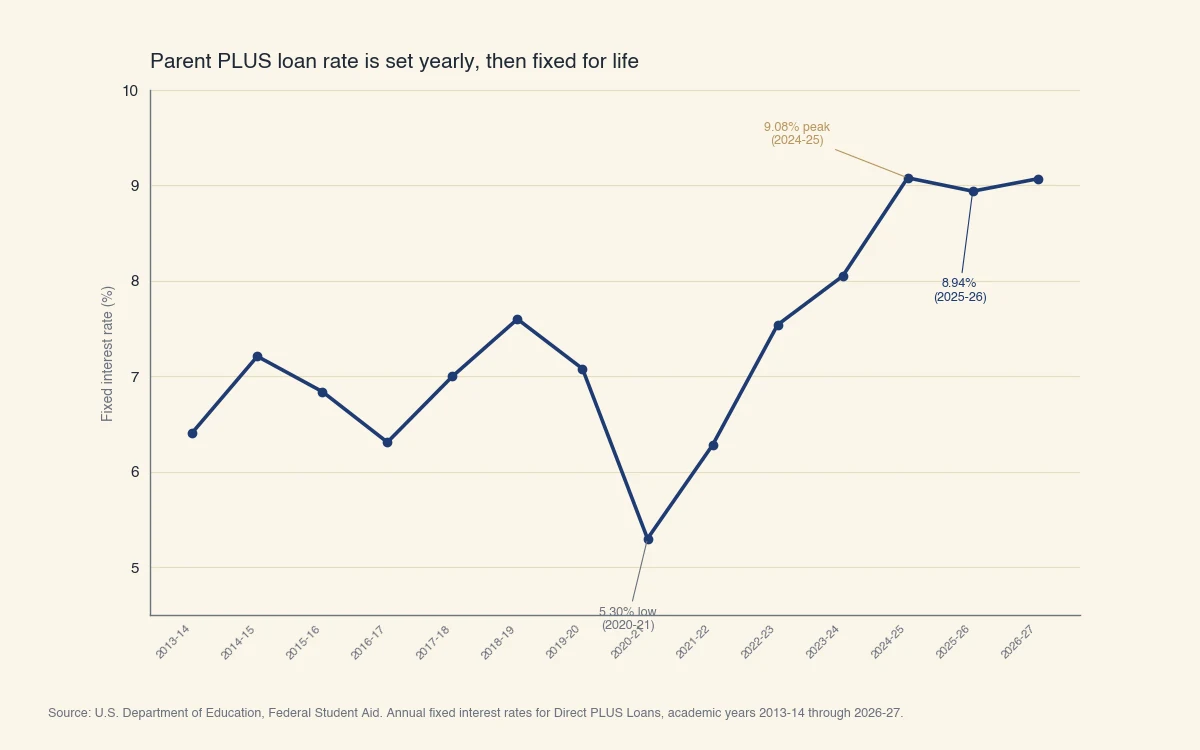

The fixed interest rate for Parent PLUS loans first disbursed between July 1, 2025 and June 30, 2026 is 8.94%, and loans disbursed on or after July 1, 2026 carry a 9.07% fixed rate (Federal Student Aid). On top of the rate, every Parent PLUS loan has a 4.228% origination fee, which the government deducts from each disbursement before the money reaches the school. Because that fee is part of the cost of borrowing, the loan's APR ends up higher than the stated interest rate.

The rate is not arbitrary. Federal law builds it from two parts each year:

- The 10-year Treasury note yield. Each year's rate starts from the high yield at the final 10-year Treasury auction before June 1.

- A fixed 4.60 percentage-point margin, with a hard cap of 10.5% for PLUS loans (Federal Student Aid).

Because the Treasury yield moves every year, the Parent PLUS rate is reset every July 1 for new loans. But that reset only applies to loans disbursed in the new window. A loan you already hold keeps the rate it was issued at, for as long as you owe it.

That fixed-for-life design is why "signing over" or shopping for a lower federal rate is impossible. The rate has climbed sharply over the past few years, and a parent who borrowed at the 2024-25 peak is locked at 9.08% even though earlier borrowers locked in far less.

Source: U.S. Department of Education, Federal Student Aid. Annual fixed interest rates for Direct PLUS Loans, academic years 2013-14 through 2026-27.

The takeaway from the chart: the rate you get depends entirely on the year you borrow, and once set it never changes. There is no lever to pull on an existing loan.

Can you transfer a Parent PLUS loan to your child?

A Parent PLUS loan cannot be transferred to your child through any federal program, so the only path to moving the debt is private refinancing in the student's name. Consolidating the loan, switching repayment plans, or pursuing forgiveness all keep you as the borrower (Federal Student Aid).

Here is how the realistic options compare:

| Option | Who owes the debt afterward | Does the rate change? | Keeps federal protections? |

|---|---|---|---|

| Do nothing | Parent | No (fixed for life) | Yes |

| Child reimburses parent informally | Parent (legally) | No | Yes |

| Private refinance into child's name | Child (and any cosigner) | Yes, a new private rate | No |

| Federal Direct Consolidation | Parent | No (weighted average of existing rates) | Yes |

To refinance into the student's name, the student applies for a private loan as if it were their own. Lenders look at the student's credit score, income, and debt-to-income ratio. Most new graduates cannot qualify on their own, so lenders often require a cosigner, a second person who is equally responsible for the debt. If that cosigner is you, the parent, you are right back on the hook, only now without federal protections.

Refinancing federal debt into a private loan ends every federal benefit attached to it (CFPB):

- Income-driven repayment, which caps payments as a share of income.

- Public Service Loan Forgiveness (PSLF) for borrowers in qualifying public-sector jobs.

- Deferment and forbearance during hardship.

- Death and disability discharge, which cancels a federal Parent PLUS loan if the parent or the student dies.

What would refinancing actually cost or save?

Refinancing to a lower rate saves interest, but the savings are often smaller than parents expect once you account for the federal protections you give up. A worked example makes the tradeoff concrete.

Say you hold a $30,000 Parent PLUS loan at the 2025-26 rate of 8.94%, on the standard 10-year (120-month) repayment plan. Compare that against the student refinancing the same $30,000 balance into a private 10-year loan at 6.5% fixed. The figures below are illustrative, rounded, and exclude the original 4.228% origination fee already deducted from your federal loan.

| Federal Parent PLUS at 8.94% | Private refinance at 6.5% | |

|---|---|---|

| Monthly payment | About $379 | About $341 |

| Total interest over 10 years | About $15,500 | About $10,900 |

| Income-driven repayment available | Yes | No |

| Loan discharged if borrower dies | Yes | Usually no |

The lower rate saves roughly $4,600 in interest over ten years and about $38 a month. That is real money. But notice what the $4,600 buys away: if the parent loses income, there is no income-driven plan to fall back on, and if the parent dies, the family inherits a private balance that a federal loan would have cancelled. For a household with stable income and no need for forgiveness, refinancing can be sensible. For a household that might need those safety nets, the cheaper rate can quietly become the more expensive decision.

This is the counterintuitive part most pages skip: a smaller number on the rate line is not the same as a smaller cost of risk. Run the interest math, then ask separately whether you can afford to lose the federal protections.

What is changing for Parent PLUS borrowers in 2026?

The One Big Beautiful Bill Act, signed July 4, 2025, places the first-ever borrowing caps on Parent PLUS loans and removes income-driven repayment for new ones, with most changes taking effect July 1, 2026 (U.S. Department of Education). For decades, Parent PLUS borrowing was limited only by a school's cost of attendance; that era is ending.

Starting July 1, 2026:

- Parent PLUS borrowing is capped at $20,000 per student per year and $65,000 in total per dependent student.

- New Parent PLUS loans disbursed on or after that date can only be repaid on the Standard repayment plan, not on income-driven repayment.

Loans you already hold are grandfathered: existing Parent PLUS borrowers keep their current terms, generally for the next few years or until the student's program ends. The practical point for the "should I refinance" question is that the federal safety net for new Parent PLUS loans is shrinking, which makes the protections on your existing federal loan more valuable, not less. Trading them away through refinancing deserves more caution in 2026 than it did a year ago.

None of these changes lets you sign over or lower the rate on a loan you already have. They change how much future parents can borrow and how they repay, but the core answer to the original question stays the same: a federal Parent PLUS rate is fixed, it is yours, and the only way to a different rate is a different, private loan.