Can a local lender lower your interest rate?

Yes. Most lenders, including local credit unions, community banks, and the major national banks, will lower an interest rate if you ask the right way. Local lenders typically have more pricing flexibility than national banks because they hold loans on their own balance sheet rather than selling into Fannie Mae or Freddie Mac agency pools. The bigger barrier is not whether the lender CAN lower the rate. It is that most consumers never ask.

The first myth to dispense with: asking for a lower rate does not affect your credit score. A request to modify an existing loan or credit card APR is a soft inquiry at most, and a soft inquiry has zero impact on FICO or VantageScore. The only time a rate conversation triggers a hard inquiry is if it leads to a new credit application, and Fair Isaac groups rate-shopping inquiries within a 14-45 day window into a single inquiry for scoring purposes (Fair Isaac).

Why "local lender" specifically: the keyword carries a real structural insight. A national bank like Chase, Wells Fargo, Bank of America, or Citibank originates most of its mortgage and auto loans for sale into the secondary market. Once a loan is sold, the bank is bound to the rate sheet the buyer (typically Fannie Mae, Freddie Mac, or Ginnie Mae) publishes. A community bank or credit union that portfolios the loan on its own balance sheet is not bound by those agency rate cards, so it can price for its own risk appetite and reward relationship borrowers with rate concessions a national bank cannot easily replicate.

Three myths that stop people from asking

| Myth | Reality |

|---|---|

| "Asking lowers my credit score" | False. Modifying an existing loan or CC is a soft inquiry. No score impact. |

| "All lenders charge the same rate, set by the Fed" | False. The Fed sets the federal funds rate. Individual lender pricing varies by 50-300 basis points around that floor depending on lender type and borrower file. |

| "I will offend my lender" | False. Retention departments at every major issuer exist specifically to handle rate-reduction calls. You are not the first caller this week, and the agent is trained for the conversation. |

The lenders themselves treat these conversations as normal customer-retention activity. The borrower who avoids the call leaves money on the table.

Where local lenders actually have pricing flexibility

Lender type drives how much rate flex is available. Credit unions, community banks, and captive auto finance companies have meaningfully more pricing room than the Big Four national banks for the structural reasons below.

The structural mechanic is the portfolio vs sell decision. When a lender originates a loan, it can either keep the loan on its own balance sheet (portfolio it) or sell it into the secondary market. Portfolio loans are priced by the lender's own risk-and-return model, which has room for relationship discounts. Sold loans are priced by the buyer (Fannie, Freddie, or a private investor), and the originating lender is constrained by what the buyer will pay.

The ranking by typical pricing flexibility, from most to least flex on a standard prime-credit borrower:

- Credit unions. Member-owned cooperatives that portfolio most loans. Often the cheapest source of auto, personal, and HELOC pricing for members. Mortgage flex is mid-tier because credit unions sell some mortgage production to Fannie. Membership eligibility varies by charter (employer, geographic, association); NCUA-insured at the federal level (NCUA).

- Community banks. Typically defined as banks with under $10 billion in assets. Portfolio more of their commercial and CRE production than national banks. Mortgage and consumer flex varies by bank.

- Captive auto finance (Ford Motor Credit, Toyota Financial, GM Financial, Honda Financial, etc.). Promotional pricing and 0% APR offers come from the manufacturer subsidizing the loan to move inventory. Best deals appear when the manufacturer is overstocked on a specific model year. The lender will not match a 0% promo from a competing brand but will sometimes flex the captive's standard tier rate.

- Online and direct lenders (LightStream, SoFi, Marcus, Discover, Ally). Typically narrower pricing tiers, less negotiation room on rate, more room on fees.

- Regional banks ($10B to $250B in assets, e.g., US Bank, Truist, PNC, Fifth Third). Mix of portfolio and sold. Flex varies by product line and by how strong the borrower's relationship is.

- National banks (Chase, Wells Fargo, Bank of America, Citibank). Most production sold into the secondary market. Least rate flex of any lender type on mortgage and auto, but real flex on credit card APR and personal loans where the bank holds the loan.

The takeaway: if you are looking for rate flex on a mortgage or auto loan, start your shopping at the credit union and community bank tier. If you are looking for credit-card APR reduction, your existing national-bank issuer often has more room than you think because they hold the credit card receivable.

How to ask for a lower rate by loan type

The script changes by product. The same opening line ("I have been a customer for X years; can you review my rate?") works across all four types, but the leverage you provide differs.

Mortgage rate negotiation

Mortgage rates are negotiable in the window between loan estimate and rate lock. Once you sign the rate lock, the window mostly closes. The three concrete tactics:

- Shop 3-5 loan estimates within a 14-45 day window. All hard inquiries from rate shopping inside that window count as one inquiry on FICO. Get loan estimates from at least one credit union, one community bank, one national bank, and one online lender. Present the best estimate to your preferred lender and ask if they will match or beat.

- Negotiate discount points and lender credits, not just the headline rate. A "no-cost" loan at 7.00% might cost you the same as a 6.75% rate with one point paid upfront. Compare the APR, not the rate (see why APR and the interest rate are not the same), and ask the lender to restructure points or credits to your preference.

- Ask for fee reductions on top of rate. Origination fees (0.5% to 1.5%), underwriting fees, and processing fees are often partially waivable, especially for borrowers with 740+ FICO and 20%+ down payment (Experian).

For the mechanics of how discount points trade against rate, see how much to buy down interest rate.

Auto loan rate negotiation

Dealers receive a buy rate from each lender they work with, then add a markup (the dealer reserve) to set the contract rate you sign. The markup is typically 1 to 2 percentage points on prime credit and up to 3 points on subprime (CFPB).

Three tactics:

- Get pre-approved at a credit union before the dealership. The pre-approval is your floor. The dealer either matches or beats it or you finance through the pre-approval. Credit unions consistently offer the lowest auto rates because they portfolio. For the benchmark to judge any quote against, see what a good interest rate for a car looks like.

- Ask the F&I manager what the buy rate is. Most will not tell you, but the question signals you know how dealer reserve works. The F&I manager is trained to give back 50 to 100 basis points of the markup when challenged by a buyer who walks in with a competing pre-approval.

- Refinance the loan after 6 months. If you missed the negotiation at the dealership, refinancing through a credit union or online lender 6-12 months later (after you have established payment history on the original loan) is the second window. Auto refi has very low friction and the credit-score test for refi is typically the same as for the original loan.

Credit card APR negotiation

Credit card APRs are the easiest to negotiate because the issuer holds the receivable and the call goes to a retention department trained for the conversation.

Four tactics:

- Call the number on the back of the card and ask for a rate reduction. Open with "I have been a customer for X years and have a perfect payment record. Can you review my APR?" Be quiet after asking. The first agent's answer is often a small reduction (1-2 points). If declined, ask for the retention department or for a supervisor.

- Ask for a temporary reduction if indefinite is declined. A 1-year reduction of 2-3 percentage points is often available when an indefinite reduction is not. After the year, call again.

- Bring a competing offer. A 0% balance-transfer offer from another issuer is the strongest leverage. The retention team will often match or beat to keep the balance from migrating.

- Enroll in a hardship program if you are in active distress. A hardship program reduces APR to 0% or single digits for 6-12 months, freezes the account, and locks the minimum payment. Hardship programs do not show as derogatory on your credit report (the account remains in good standing) but enrollment is sometimes flagged.

Personal loan rate negotiation

Personal loan rates have less negotiation room than the other three product types because they are typically priced by automated decisioning. Two tactics still work:

- Apply at your primary banking relationship first if you have direct deposit or 12+ months of account history. Relationship pricing on personal loans is real, usually 25-100 basis points off the standard tier.

- Shop 3-4 lenders within a 14-day window. Online lenders (LightStream, SoFi, Discover) often have tiered pricing that beats banks for prime borrowers; banks beat online lenders for super-prime with deep relationships.

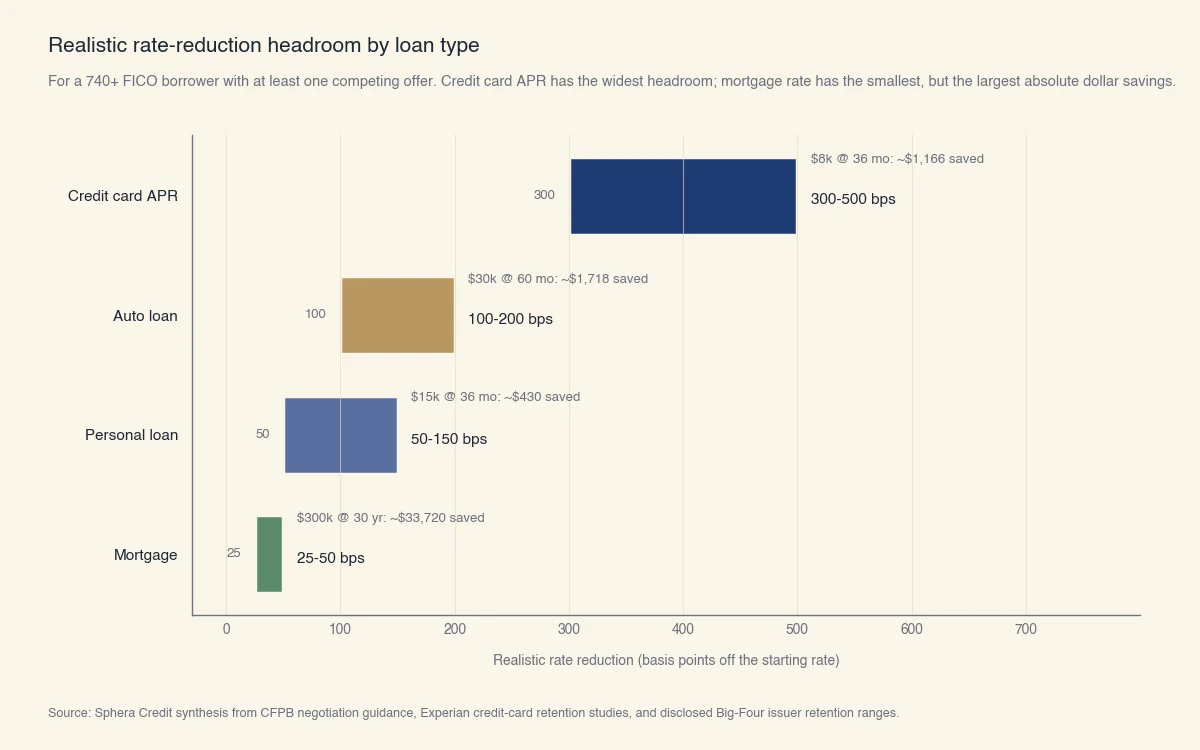

What rate reduction is realistic on each loan type?

A 740+ FICO borrower with competing offers can realistically expect 25-50 basis points off a mortgage, 100-200 basis points off an auto loan, 300-500 basis points off a credit card APR, and 50-150 basis points off a personal loan. The dollar impact varies by loan size and term.

Source: Sphera Credit synthesis from CFPB negotiation guidance, Experian negotiation studies, and disclosed retention-program ranges across major US credit card issuers.

Worked examples for the typical borrower at each product type:

Auto loan: $30,000 5-year loan. Starting rate 9.50%, target rate 7.50% (200 basis point reduction via credit-union pre-approval). Monthly payment drops from $630 to $601. Total interest savings over the 5-year term: $1,718.

Mortgage: $300,000 30-year fixed. Starting rate 7.00%, target rate 6.50% (50 basis point reduction via competing pre-approval). Monthly payment drops from $1,996 to $1,896. Total interest savings over the 30-year term: $33,720.

Credit card: $8,000 balance carried for 36 months while paying $300/month. Starting APR 24%, target APR 18% (600 basis point reduction via retention call). Total interest savings: $1,166.

The mortgage scenario produces the largest dollar savings because of the loan size and amortization length, even though the rate-reduction headroom is smallest in basis-point terms. The credit-card scenario has the highest reduction in basis points but smaller absolute dollars because of the shorter payoff period. Use the dollar-magnitude framing when deciding which conversation to have first: a 30-minute mortgage negotiation can save five figures over the life of the loan.

What to do if your lender says no

A "no" on the first call is not a final answer. Lenders give a no by default because most callers do not push back, but the actual policy almost always allows for a yes when the borrower escalates or returns. Three concrete next moves:

- Ask for the retention department or a supervisor. Frontline agents have lower authorization limits than retention specialists. Politely ask: "Can you transfer me to the retention team / a supervisor who can review this further?"

- Follow up in 3-6 months. If your credit score has improved, your relationship has lengthened, or a new competing offer is on the table, the answer changes. Note the date of your call, what you asked, what they said, and try again on a regular cadence.

- Refinance to a different lender. If your current lender will not flex, the rate-shopping window across 3-5 competitors (within 14-45 days for credit-inquiry purposes) often produces a real alternative. A refi from a national bank to a credit union or online lender is one of the most common paths to a lower rate.

The only product where "no" is more durable is a fixed-rate mortgage already past rate-lock. There the answer is genuinely refinance, not renegotiate. For every other product (credit card APR, auto loan, personal loan, mortgage pre-lock), the no-on-first-ask is the start of the conversation, not the end.

The dollars at stake are large enough to justify the effort. A single hour spent on the right three or four phone calls and pre-approval applications can produce thousands of dollars in interest savings on the products most US households hold. The conversation costs nothing, does not affect your credit score, and is the routine retention activity your lender's team is trained for.