Do medical bills affect your credit score?

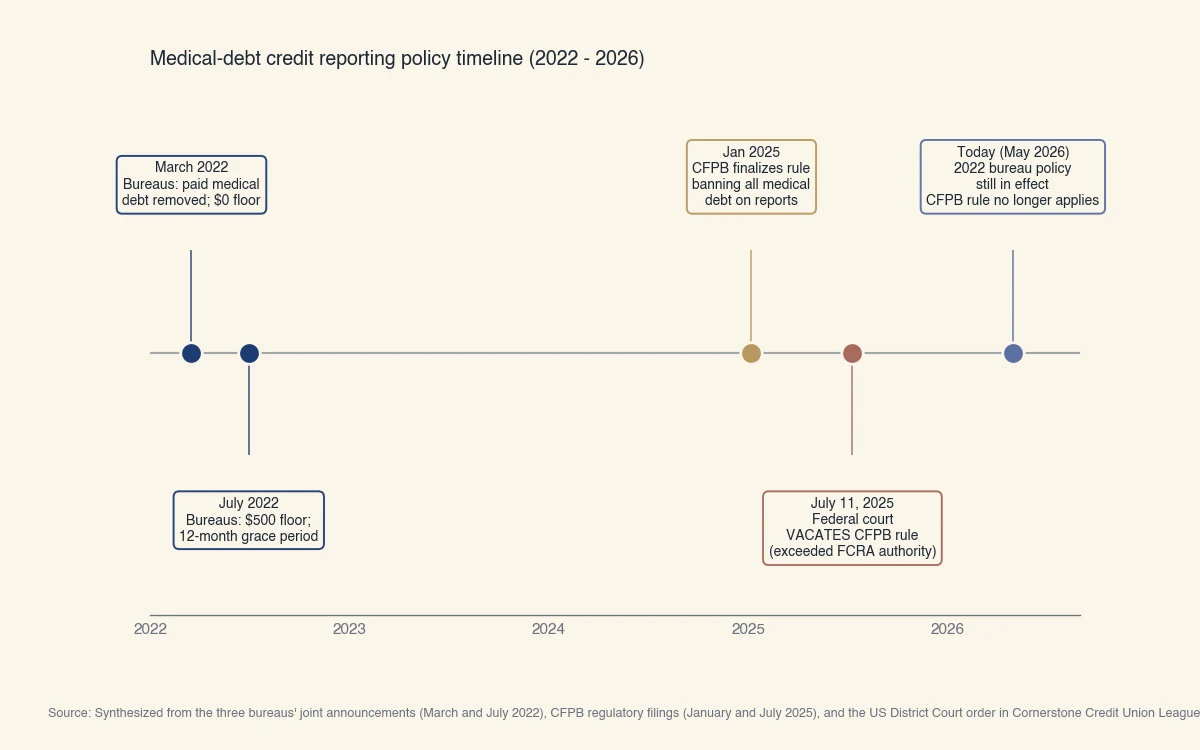

Yes, but only after the bill is sold to a collection agency, the debt is at least 12 months old, and the balance is over $500. As of May 2026, the CFPB's January 2025 rule that would have banned medical debt from credit reports has been vacated by a federal court, so the three bureaus' voluntary 2022 policy is what currently applies. Three separate things determine the answer, and most articles online conflate them.

The three things:

- The Fair Credit Reporting Act (federal law) currently permits the reporting of coded medical debt (debt that does not identify a specific provider or medical condition).

- The three bureaus' voluntary 2022 policy removes paid medical collections, removes medical debt under $500, and gives a 12-month grace period before any medical collection can be reported.

- The CFPB's 2025 medical-debt rule would have prohibited the reporting of all medical debt, but a federal court vacated the rule in July 2025, so it no longer applies.

The result for a borrower in 2026: a medical bill can reach your credit report only if it goes unpaid for at least 12 months, is over $500, is sold to a collection agency, and the collection agency reports it to one or more bureaus. The original provider does not report directly.

What changed in 2025 with the medical-debt rule

The CFPB rule that would have removed medical debt from credit reports was finalized on January 7, 2025 and vacated by court order on July 11, 2025. As of writing, the rule does not apply. The Bureau estimated the rule would have removed $49 billion in medical debt from the credit files of 15 million Americans and raised the affected consumers' scores by an average of 20 points (CFPB, 2025). None of that took effect.

Source: Synthesized from the three bureaus' joint announcements (March and July 2022), CFPB regulatory filings (January and July 2025), and the US District Court order in Cornerstone Credit Union League v. CFPB.

The court's reasoning matters because it tells you what is still permitted. The Eastern District of Texas ruled that the CFPB exceeded its statutory authority under the FCRA. The FCRA expressly permits the reporting of coded medical debt (debt that does not identify a specific provider or medical condition). The vacated rule attempted to prohibit what the FCRA explicitly allows.

After the vacatur, what currently applies is the 2022 voluntary bureau policy, which has three pieces:

- Paid medical collections are not reported. If you pay a medical collection, it should drop off your report within 30 to 60 days.

- Medical debt under $500 is not reported. The dollar floor was raised from $0 to $500 in July 2022.

- The 12-month grace period. A medical collection cannot be reported until the underlying debt is at least 12 months past due, raised from 180 days in July 2022.

These bureau-level policies are not law. They are commitments the three bureaus made in 2022. They can be changed by the bureaus at any time, though as of writing they remain in effect.

What the three different rules actually require

The FCRA, the voluntary bureau policy, and the vacated CFPB rule each cover a different scope. Conflating them is the single most common error in articles on this topic. The table below isolates each.

| What it requires | Currently in effect? | |

|---|---|---|

| FCRA (federal law) | Permits reporting of "coded medical debt" that does not identify a specific provider or medical condition. Sets the 7-year retention window for negative items. | Yes |

| 2022 bureau policy | Paid medical collections excluded. Medical debt under $500 excluded. 12-month grace period before reporting. | Yes (voluntary) |

| 2025 CFPB rule | All medical debt prohibited from reports used in most lending decisions. Lenders banned from making credit decisions based on medical debt. | No (vacated July 11, 2025) |

The practical takeaway: a $1,200 unpaid medical bill that has been in collections for 14 months CAN appear on your report today. A $400 unpaid medical bill cannot. A medical bill you have paid off cannot. Anything from a hospital that has not yet been sent to collections cannot.

How much can a medical collection actually drop your score

A single $1,000+ unpaid medical collection can drop a FICO 8 score by 50 to 150 points, while the same item is ignored entirely under FICO 9 and VantageScore 4.0 if paid, and weighted less heavily than non-medical collections in the newer models even if unpaid. The model your lender uses matters as much as whether the item is there.

| Starting score tier | FICO 8 impact | FICO 9 impact | VantageScore 4.0 impact |

|---|---|---|---|

| 760+ | -100 to -150 pts | -50 to -100 pts (unpaid only) | -50 to -100 pts (unpaid only) |

| 700-759 | -90 to -130 pts | -40 to -90 pts (unpaid only) | -40 to -90 pts (unpaid only) |

| 640-699 | -70 to -110 pts | -30 to -70 pts (unpaid only) | -30 to -70 pts (unpaid only) |

| 580-639 | -50 to -90 pts | -20 to -50 pts (unpaid only) | -20 to -50 pts (unpaid only) |

Two patterns to notice:

- Higher starting scores fall further in absolute terms. A clean 780-score file penalizes a single derogatory event more than a 600-score file already absorbing other negatives. This is a general scoring pattern, not unique to medical debt.

- Paid medical collections are ignored under FICO 9 and VantageScore 4.0. If a lender uses one of these newer models, paying off a medical collection removes the score impact entirely. Older FICO 8 still considers paid medical collections, though the weight diminishes over time.

Many mortgage and auto lenders still use FICO 8 or even older "mortgage FICO" variants (FICO 2, 4, 5). Consumer monitoring apps mix VantageScore 3.0, VantageScore 4.0, and FICO 8 depending on the provider. The same paid medical collection may not appear in your monitoring app while still costing you points in a mortgage underwriter's view.

What can move your score back up

Pay any medical collection in full and confirm the bureau removes it within 60 days. Dispute any medical entry you do not recognize. Use the 12-month grace period and the under-$500 floor to your advantage by negotiating with the provider before the debt reaches collections. The mechanical recovery path:

- Pay the collection. Under the 2022 bureau policy, paid medical collections are removed from credit reports. Confirm removal within 60 days by pulling all three reports.

- Dispute unrecognized items. Under the FCRA, the bureau has 30 days to investigate and the furnisher must verify the debt or have it removed. The CFPB has documented that medical collections have one of the highest dispute-success rates because hospital billing data is often incomplete when sold to collection agencies.

- Negotiate before collections. Most providers will accept a payment plan, a settlement at 50 to 70 percent of the original balance, or a one-time financial-hardship reduction. None of those routes triggers a credit-report entry as long as the provider does not refer to collections.

- Use the 12-month grace period. Even if the bill is in dispute or partial payment, the bureau policy gives you a full year before any medical collection can be reported. Use that window.

What does NOT help: paying for credit-repair services that promise to remove medical debt. The Federal Trade Commission has warned consumers that "permanent removal" promises are usually based on disputing accurate items en masse, which fails when furnishers respond on time.

Bottom line

Yes, medical bills can affect your credit score in 2026, but only through a narrow path that requires unpaid debt over $500, in collections, for at least 12 months. The CFPB rule that would have banned medical debt from credit reports was vacated in July 2025 and no longer applies. The three bureaus' voluntary 2022 policy is what currently protects consumers, and it can be changed by the bureaus at any time. Pay any medical collection in full and confirm bureau removal within 60 days; dispute any entry you do not recognize.

The legal landscape may move again. The CFPB has the option to issue a narrower medical-debt rule that survives FCRA scrutiny. Several state legislatures (New York, Colorado, Illinois, Connecticut, and Rhode Island as of writing) have passed or proposed their own state-level prohibitions on medical-debt reporting that apply to credit decisions made under state consumer-protection statutes. Watch the bureaus' voluntary policies as the primary indicator of practical change; watch state laws as the second indicator. For the broader question of why a credit score might be falling, see why credit scores fall and how to diagnose the cause. For the recovery path after a medical-collection drop, see how to boost a US credit score.