Do student loans affect your credit score?

Yes. Federal and private student loans are reported to the three credit bureaus as installment trade lines, and a 90-day delinquency on a federal loan can drop a US credit score by 87 to 171 points depending on the starting tier. The post-pandemic on-ramp grace period that suppressed delinquency reporting ended on September 30, 2024, so as of May 2026 the reporting cycle is fully restored. The Federal Reserve Bank of New York's March 2025 analysis is the cleanest current dataset on the impact (NY Fed).

Three things determine how student loans hit your score:

- On-time payments build positive history. Each on-time payment is reported and contributes to the 35% payment-history factor in FICO.

- The day count to delinquency. Federal direct loans report at day 90 past due. Most private lenders report at day 30. Hitting either threshold reverses years of positive history.

- The starting score. A clean 780 file falls further in absolute terms than a 600 file from the same event. This is counterintuitive but well-documented.

One federal loan type deserves its own note: Parent PLUS loans, which a parent borrows for a child, report under these same federal rules. Parents often ask whether they can sign the interest rate over to the student, but a federal rate is fixed for life and cannot be reassigned.

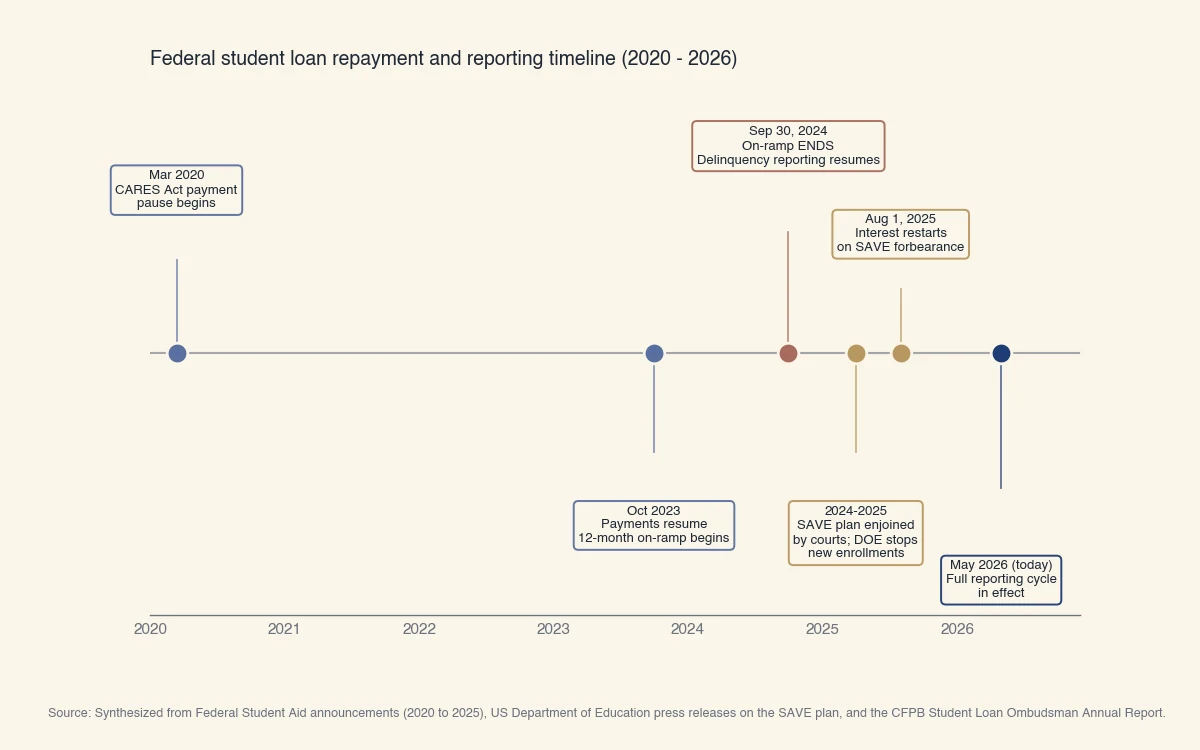

The rest of this page walks through the 2024-to-2026 timeline (which most articles have not caught up to), the score-drop magnitudes by tier, and what happens at each day-count threshold.

What changed since the COVID payment pause

The federal student loan repayment landscape has changed three times in 18 months: the on-ramp grace period ended September 30, 2024; the SAVE plan was enjoined and is being wound down by July 2028; and interest charging on SAVE-forbearance loans restarted August 1, 2025. As of May 2026, the post-on-ramp delinquency-to-credit-report cycle is in full effect.

Source: Synthesized from Federal Student Aid announcements (2020 to 2025), the US Department of Education press releases on SAVE plan litigation, and CFPB Student Loan Ombudsman reports.

The on-ramp explained, because most articles miss this: during the on-ramp (October 2023 to September 30, 2024), missed federal student loan payments were not reported to bureaus, did not count as delinquencies, and did not trigger default. Borrowers who fell behind in this window protected their credit. As of October 1, 2024, that protection ended. Borrowers behind on payments after that date are accruing days toward the 90-day delinquency threshold normally.

The SAVE plan complicates the picture for the roughly 8 million borrowers who enrolled in it before the injunction. Those borrowers are in administrative forbearance, which means:

- Payments are paused (not delinquent).

- Interest accrues (resumed August 1, 2025).

- Time in forbearance does not count toward Public Service Loan Forgiveness or income-driven forgiveness.

- The forbearance ends when the courts and Congress finish unwinding SAVE, no later than July 2028.

If you are in SAVE forbearance and miss a payment when the forbearance ends, the 90-day delinquency clock starts then.

How much can a delinquent student loan drop your score

The Federal Reserve Bank of New York's March 2025 analysis found that a 90-day federal student loan delinquency drops the average borrower's credit score by 87 to 171 points, depending on starting score tier. The counterintuitive finding: higher starting scores fall further. This is the cleanest current data on the impact.

| Starting credit score | Average point drop from a 90-day delinquency |

|---|---|

| Below 620 | -87 |

| 620 to 659 | -143 |

| 660 to 719 | -165 |

| 720 to 759 | -165 |

| 760 and above | -171 |

Why higher scores fall further: scoring models penalize a "clean file gets dirty" event more than a "dirty file gets dirtier" event. A 780 file with one new derogatory item shows the model that something materially changed in the borrower's credit behavior. A 580 file with one additional derogatory item is just another data point consistent with the existing pattern. The proportional impact on the model's estimate of default probability is larger when the starting baseline is clean.

The same 9.7 million borrowers who fell delinquent in Q1 2025 represent over $250 billion in past-due federal student loan debt. That damage stays on credit reports for seven years from the date of the original delinquency.

The day-count cascade: when each event reports

Federal student loans follow a predictable reporting cascade tied to days past due. Each step adds its own derogatory mark. Most articles describe the cascade loosely; the day counts are exact.

| Days past due | What happens | Reported to bureaus? | Typical score impact |

|---|---|---|---|

| 1 to 29 | Late fee from servicer | No | No score impact |

| 30 to 59 | Servicer outreach and late-fee compounding | Private lenders typically begin reporting | Minor impact (private only); none for federal |

| 60 to 89 | Increased collection pressure from servicer | Private continues; federal not yet | Compounding impact (private only) |

| 90+ federal | Federal direct loan goes delinquent | Yes, all three bureaus, monthly | -60 to -170 points (see tier table) |

| 120+ | Servicer may begin involuntary administrative wage garnishment for federal | Continues monthly | Compounds with each missed cycle |

| 270 days | Federal loan goes into default | Default derogatory mark added | Additional -50 to -100 points on top of delinquency |

| 270+ | DOE can withhold tax refunds, garnish wages, offset Social Security | Continues | Wage garnishment can be up to 15% of disposable income |

The 90-day threshold is the moment most credit damage happens. The 270-day default threshold adds more, but the bulk of the score drop is at the first 90-day report. Pulling out of delinquency at day 89 is materially different from pulling out at day 91. If you are close to the threshold, contact your servicer immediately, an income-driven repayment plan with a low or zero monthly payment can pause the day-count clock without triggering reporting.

What can move your score back up after a student loan delinquency

Cure the delinquency by paying past-due amounts in full or entering a federal rehabilitation program, but understand the damage stays on your credit report for seven years even after you cure. The mechanical recovery path:

- Pay all past-due amounts to bring the loan current. The trade line will change from "delinquent" to "current" on the next reporting cycle, typically 30 to 60 days later. Score recovery from this step is partial because the historical late-payment mark remains.

- Federal loan rehabilitation. For defaulted federal loans, the Loan Rehabilitation program allows nine consecutive on-time monthly payments at a reasonable amount (typically 15% of discretionary income or as low as $5). After rehabilitation, the default mark is removed from your credit report, though the prior delinquency marks remain visible to lenders for seven years.

- Federal loan consolidation. Consolidating defaulted federal loans into a new Direct Consolidation Loan can move the loan out of default in 30 to 90 days, though the prior default mark stays on your report. Less powerful than rehabilitation but faster.

- Income-driven repayment enrollment. Moving to an IDR plan (IBR, PAYE, ICR after SAVE is unwound) lowers the monthly payment to an affordable level, often $0 if your income qualifies. Future on-time payments at $0 still build positive history.

- Time. Each year a delinquency ages, its weight in the FICO calculation drops. A 90-day late from year one of the 7-year retention loses most of its score impact after 24 months even though the entry stays visible. For the broader diagnostic side of this question, see why credit scores fall and how to diagnose the cause. For the recovery-path tactics, see how to boost a US credit score.

What does NOT help

Paid student-loan-relief services that charge upfront fees for federal programs are almost always selling something the borrower can do for free directly through studentaid.gov. The Federal Trade Commission and CFPB have repeatedly warned against "student loan debt relief" companies that charge upfront fees to consolidate or rehabilitate loans. Federal loan consolidation is free. Loan rehabilitation requests are free. Any company charging a fee for these federal programs is selling a service that the borrower can complete at no cost.

Bottom line

Yes, student loans affect your credit score. Federal direct loans hit your credit at the 90-day past-due threshold; private loans typically hit at 30 days. The 12-month on-ramp grace period ended September 30, 2024, so the reporting cycle is fully restored as of 2026. The average 90-day delinquency drops a US credit score by 87 to 171 points depending on starting tier, with higher scores falling further. If you cannot afford a payment, contact your servicer before day 60 to enroll in an income-driven plan, deferment, or forbearance, any of which prevents the 90-day reporting threshold.