How much do underwriters make in Canada?

The median Canadian underwriter earns about $72,010 a year, equivalent to $34.62 an hour at full-time hours, based on Statistics Canada's Labour Force Survey for the 2023 to 2024 reference period (Job Bank Canada). The national range runs from $25.00 an hour at the low end to $51.28 an hour at the high end, which translates to a full-time annual band of roughly $52,000 to $106,660.

That single national figure hides a lot of variation. Underwriting is not one job. Statistics Canada classifies insurance underwriters under National Occupational Classification (NOC) 12202 and mortgage underwriters under NOC 13201, and within each code the compensation spread widens further when you include bonuses, pension contributions, and group benefits. About 94.3 percent of Canadian underwriters receive at least one non-wage benefit, according to Job Bank.

The rest of this page breaks the question into the four distinct underwriter career paths in Canada, then builds a year-by-year worked example of total compensation. We close with the structural reason senior underwriters earn well above the national median while juniors do not.

National wage anchors for insurance underwriters (NOC 12202)

The Statistics Canada wage data, converted to annual at the standard 2,080 hours of full-time year-round work:

| Percentile | Hourly | Annual (CAD, 2,080 hrs) |

|---|---|---|

| Low | $25.00 | $52,000 |

| Median | $34.62 | $72,010 |

| High | $51.28 | $106,660 |

These figures exclude bonuses, commissions, and the value of pension and group benefits. Total compensation is meaningfully higher.

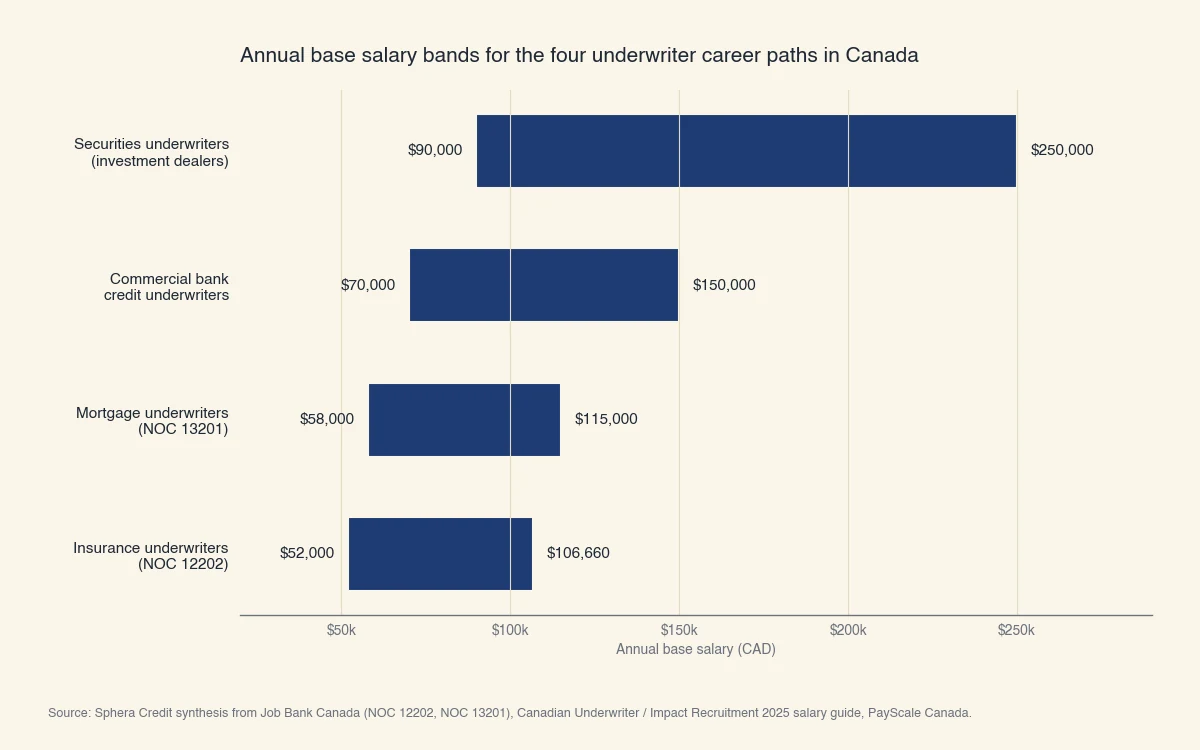

The four kinds of underwriter in Canada and what each earns

Most articles report a single "underwriter" salary, but there are four distinct career paths in Canada with different employers, regulators, and pay bands. Insurance underwriting and mortgage underwriting are separate occupations under the National Occupational Classification system. Commercial credit underwriting at the major banks and securities underwriting at investment dealers add two more career ladders that do not appear in Job Bank's main wage tables.

Source: Sphera Credit synthesis from Job Bank Canada (NOC 12202 insurance, NOC 13201 mortgage), Canadian Underwriter / Impact Recruitment 2025 salary guide for commercial roles, and PayScale Canada for securities underwriting.

Insurance underwriters (NOC 12202)

Insurance underwriters review applications for property, casualty, life, and specialty insurance policies and decide whether to issue coverage and at what premium. In field roles, a field underwriter's main task is gathering applicant information on site before the file reaches a desk underwriter. The national median is $34.62 an hour, or about $72,010 a year (Job Bank Canada). Within insurance, three sub-tracks pay differently:

- Personal lines (auto, home, tenant insurance): juniors $50,000 to $65,000; seniors $80,000 to $110,000.

- Commercial lines (business property, liability, cyber): juniors $55,000 to $75,000; seniors $95,000 to $140,000 in Toronto and Vancouver.

- Surety and specialty (bonding, construction, environmental): seniors $100,000 to $140,000 plus, with the top end on specialty risk in major centres (Canadian Underwriter).

Mortgage underwriters (NOC 13201)

Mortgage underwriters assess residential and small commercial mortgage applications against lender policy and the OSFI Guideline B-20 framework that governs federally regulated lenders (OSFI). Base salaries at Schedule I banks generally run $58,000 to $95,000, with senior commercial mortgage underwriters reaching $115,000 or more. Job Bank publishes provincial wage data separately for NOC 13201 (Job Bank Canada).

The work splits into prime mortgage underwriting (conforming, insured) and non-conforming or alternative mortgage underwriting (B-lender, private). Non-conforming underwriters typically earn more because each file requires more discretionary judgement and the lenders that hire them pay a premium for that judgement.

Commercial credit underwriters at banks

Commercial credit underwriters at the Big Five Canadian banks evaluate business loans, asset-based lending facilities, and corporate credit lines. They sit inside the bank's credit risk function rather than insurance, and pay reflects that. Greater Toronto Area commercial underwriters earn $60,000 to $80,000 at junior level, $80,000 to $100,000 at intermediate level, and $100,000 to $140,000 at senior level (Canadian Underwriter). Add bonus, pension, and benefits and the senior all-in figure is regularly $150,000 to $180,000.

Securities underwriters at investment dealers

Securities underwriters at investment dealers underwrite new debt and equity issues, syndicate transactions, and price risk for institutional placements. Base salaries start higher than the other three paths ($90,000 to $130,000 for analysts and associates) and rise into the $200,000 to $250,000+ range at vice-president level, with bonus often exceeding base. The role is concentrated in Toronto's Bay Street firms and a handful of Montreal and Calgary teams.

What does total compensation actually look like over a career?

Most public salary data quotes base pay only, which understates what a Canadian underwriter takes home by 20 to 40 percent depending on employer and seniority. A year-by-year build of total compensation for a commercial credit underwriter at a Big-Five Toronto bank illustrates the gap. The figures below combine Job Bank base data, Canadian Underwriter / Impact Recruitment bonus ranges, and typical Schedule I bank benefits packages.

Year 1: junior credit analyst

- Base salary: $68,000

- Annual bonus (10% target): $6,800

- Group RRSP match (typically 3% to 5%): $2,720

- Defined-benefit pension (employer-side, ~6% of base): $4,080

- Group health, dental, life insurance (employer cost): $3,500

- Total compensation: approximately $85,100

Year 5: intermediate underwriter

- Base salary: $92,000

- Annual bonus (15% target): $13,800

- Group RRSP match: $3,680

- Defined-benefit pension (~7% of base): $6,440

- Group benefits: $4,200

- Total compensation: approximately $120,120

Year 10: senior underwriter

- Base salary: $125,000

- Annual bonus (22% target): $27,500

- Group RRSP match: $5,000

- Defined-benefit pension (~8% of base): $10,000

- Group benefits: $5,000

- Total compensation: approximately $172,500

The same career at a regional credit union or insurance carrier typically lands 10 to 20 percent below these numbers, with the gap concentrated in bonus and pension rather than base.

What if you stay junior?

A junior underwriter at a regional insurance carrier who stays at the junior level for the full ten years rather than progressing reaches about $75,000 in base by year ten, total compensation around $90,000. The premium for advancement is structural, not cosmetic, and the rest of this page explains why.

Why senior underwriters earn so much more than juniors

The wage spread between junior and senior underwriters in Canada is widening, and the reason is the same reason routine consumer-credit underwriting has been getting automated since the 1990s: rules-based decisions are increasingly handled by software, while judgement-heavy decisions still require an experienced human. This is observable in the data. The Job Bank low-to-high spread for NOC 12202 is roughly 2.0x ($25.00 to $51.28 an hour). The commercial underwriting low-to-high spread reported in the Canadian Underwriter 2025 salary survey is closer to 3.5x once director and AVP roles are included.

Three forces explain the gap:

-

Routine underwriting compresses junior wages. Prime mortgages that fit Guideline B-20 cleanly, personal lines auto and home insurance with standard risk profiles, and small unsecured consumer loans are increasingly decisioned by rules engines and credit-bureau-driven models. The human role on these files is verification, not judgement, and the labour market prices verification cheaply.

-

Complex risk still requires judgement and the people who can do it are scarce. Non-conforming mortgages, asset-based lending, specialty insurance lines (cyber, environmental, construction), and securities underwriting do not reduce cleanly to a rule set. The 5 Cs of credit, OSFI Guideline B-20 expectations around lender prudence, and the regulatory requirement that "the lender" (not an algorithm alone) approve mortgages keep humans in the decision seat for these files.

-

Specialization pays an explicit premium. The Canadian Underwriter 2025 report finds that firms specifically reward expertise in cyber, environmental, construction, energy, and specialty lines (Canadian Underwriter). A senior who has spent five to ten years on these files earns the spread.

At Sphera Credit we work on this problem from the lender side: our AI agents handle the document-collection and verification work that previously consumed junior-underwriter time, so the underwriter's hours go into the judgement calls where they actually add value. The wage data suggests the market is already pricing for that division of labour.

How do you become a higher-paid underwriter in Canada?

The three highest-impact moves are choosing a specialization with structural demand, earning the credential that signals competence in that specialization, and moving to an employer that pays for it. Each of these is observable in the salary data. If you have not entered the field yet, start with how to become an underwriter, then optimize for pay.

-

Specialization. Cyber, environmental, construction, energy, and specialty surety pay measurable premiums over personal lines. Commercial credit underwriting at Schedule I banks pays measurably more than regional insurance carrier work.

-

Credentials. The Chartered Insurance Professional (CIP) designation from the Insurance Institute of Canada is the standard credential for insurance underwriters. The CFA designation and a business or finance degree are typical for commercial credit and securities underwriting. The CIP usually takes two to four years of part-time study while working.

-

Employer. Big-Five banks, the major Canadian insurance carriers (Intact, Aviva, Manulife, Sun Life, Definity), and Toronto investment dealers consistently anchor the top end of compensation ranges. Mid-sized regional carriers, credit unions, and B-lenders typically pay 10 to 20 percent less for an equivalent seniority.

Geography matters less than employer type in the senior bands. A senior commercial underwriter at a Big-Five bank earns roughly the same in Toronto, Vancouver, and Calgary; the bigger spread is between bank and non-bank employer in the same city.