Should I be worried about underwriting?

Probably less than you think. In Q4 2025, only 0.24% of Canadian residential mortgages from chartered banks were 90 days or more delinquent (CMHC), and most applications that reach formal underwriting are approved. The honest answer to "should I be worried" is conditional: worry is rational only when you know your file carries one of the specific red flags an underwriter will catch. The rest is process.

Underwriting is the lender's risk-assessment step. A real person (the underwriter) reads your income proof, your credit report, your debt obligations, the property appraisal if the loan is secured, and a stack of supporting documents. They then decide whether to fund the loan, at what rate, and on what conditions. For federally regulated mortgage lenders in Canada, the framework is OSFI Guideline B-20 (OSFI).

Three patterns make underwriting feel scarier than the data warrants:

- Most outcomes are not binary. The underwriter usually issues a conditional approval, not an instant yes or no. Conditions are most often documentation requests, not financial obstacles.

- The published data is reassuring. Canadian mortgages from federally regulated lenders perform better than any other major form of consumer credit.

- The red flags are knowable. OSFI publishes the ratios, the bureaus publish the scoring methodology, and the FCAC publishes the borrower checklist. You can walk into underwriting knowing what the underwriter will look at.

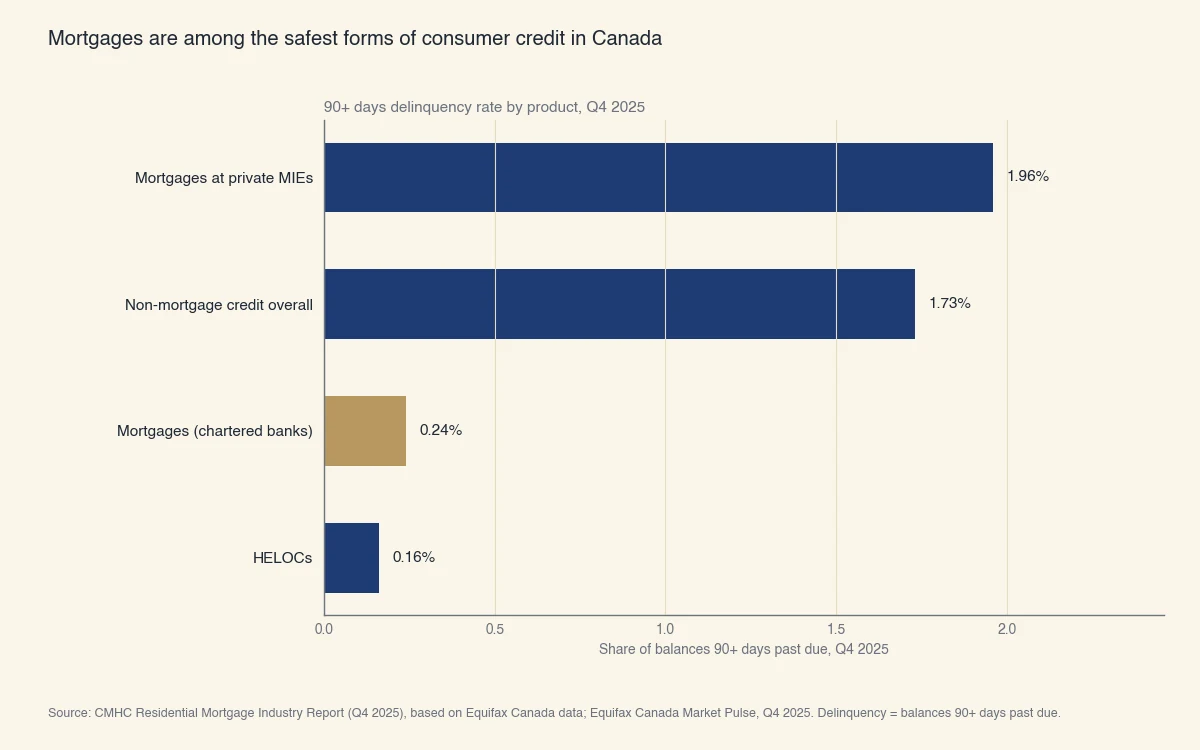

Source: CMHC Residential Mortgage Industry Report (Q4 2025), based on Equifax Canada data; Equifax Canada Market Pulse, Q4 2025. Delinquency = balances 90+ days past due.

The chart is the counter-intuitive headline of this article. Canadian mortgages from federally regulated lenders are among the safest forms of credit in the country precisely because OSFI's B-20 underwriting rules force lenders to filter out applications they cannot stand behind. The same rules that make underwriting feel intimidating are the reason almost everyone who clears it stays current on their loan.

What does an underwriter actually check?

An underwriter scores your file on three things: capacity, credit, and collateral. These are called the three Cs, and every Canadian lender, regulated or not, uses some version of them.

Capacity is your ability to make the monthly payment. The lender measures it with two ratios:

- Gross Debt Service (GDS) ratio: monthly housing cost (mortgage payment, property tax, heat, half of any condo fee) divided by gross monthly income.

- Total Debt Service (TDS) ratio: GDS plus all other monthly debt payments, divided by gross monthly income.

OSFI's published practice expects federally regulated lenders to keep GDS at or below 39% and TDS at or below 44% for prime mortgages (OSFI). Some lenders set internal caps tighter. Insured mortgages (CMHC, Sagen, Canada Guaranty) often run 35% GDS / 42% TDS as a working ceiling.

Credit is your score and your repayment history. Most prime Canadian lenders want a credit score of 680 or higher for an uninsured mortgage and 660 or higher for an insured one. The underwriter does not just look at the number. They scan the report for late payments in the last 24 months, collections, judgments, and any account currently in arrears.

Collateral is the property itself. The underwriter orders an appraisal (or accepts an automated valuation model for low-loan-to-value files), checks zoning and title, and verifies that the property is something the lender can take back and sell if it had to. That property-focused side of the file is the heart of real estate underwriting.

The stress test, in plain numbers

Under OSFI's Minimum Qualifying Rate, a federally regulated lender must qualify you at the greater of your contract rate plus 2 percentage points or 5.25% (OSFI). This is the mortgage stress test. It does not change the rate you actually pay. It changes the rate the underwriter uses when calculating GDS and TDS.

The Bank of Canada's 2024 analysis of stress-test resilience concluded that the rule has materially reduced the share of households that would default after a rate shock (Bank of Canada). The data behind the chart above is partly a result of this rule working as intended.

Since September 2024, a straight switch at renewal (same amortization, same loan amount) to a different federally regulated lender no longer triggers a re-test. Renewals at the same lender have never required one.

A worked GDS and TDS example

The fastest way to see why most files clear underwriting is to actually do the calculation. Consider Sarah and Marc, a married couple in Ottawa applying for a 25-year fixed-rate mortgage at a 4.74% contract rate.

| Input | Amount |

|---|---|

| Gross household income | $95,000 / year ($7,917 / month) |

| Mortgage payment at the 6.74% qualifying rate ($420,000, 25-year amortization) | $2,900 / month |

| Property tax | $325 / month |

| Heat | $130 / month |

| Half of condo fees (n/a, freehold) | $0 |

| Car loan payment | $450 / month |

| Credit card minimum (on a $4,000 balance at $200 / month) | $200 / month |

Their housing cost is $2,900 + $325 + $130 = $3,355 / month.

- GDS = $3,355 / $7,917 = 42.4%. Above the 39% OSFI working ceiling for prime conventional mortgages. This file would be conditional or declined at most chartered banks at full ratio.

- TDS = ($3,355 + $450 + $200) / $7,917 = 50.6%. Above the 44% ceiling.

Sarah and Marc are over both caps. The honest underwriter response is: "Reduce the price, increase the down payment, or pay down the car loan before we can fund." This is the kind of "decline" most borrowers misread as a permanent no. It is actually a math problem with three solvable inputs.

Now suppose they pay off the car loan ($450 / month gone) and lower the target purchase by $40,000 (mortgage payment drops to about $2,624). Housing cost becomes $3,079.

- GDS = $3,079 / $7,917 = 38.9%. Just inside the 39% cap.

- TDS = ($3,079 + $200) / $7,917 = 41.4%. Inside the 44% cap.

Same household. Same lender. Same underwriter. Different answer. The "should I be worried" question reframes from "Will the underwriter reject me?" to "Where am I against the published ratios, and what would move me inside them?" The Financial Consumer Agency of Canada publishes a free mortgage calculator that mirrors the lender's math (FCAC).

What actually triggers a decline?

Most declines come from one of five causes, and four of them are detectable before you apply. The fifth is the appraisal, and even that is partly manageable.

- Documentation gaps. A missing T4, a paystub that does not match the employment letter, an NOA missing for the most recent tax year, a gift-letter signature missing on a down-payment gift. The underwriter flags the gap, the file sits in conditions, and the closing slips. This is the most common reason files stall and the easiest to prevent.

- Credit issues uncovered at the hard pull. A 30-day late payment from 14 months ago that the borrower forgot. A collection account that was settled but never updated. A second hard inquiry from a car dealership that ran credit a week earlier. Pulling your own report from Equifax or TransUnion before applying eliminates almost all of these surprises (Equifax Canada).

- Undisclosed debts surfacing at the underwriter's pull. A line of credit with a zero balance still counts toward TDS at 3% of the limit. Co-signed debt for a child or sibling counts in full. Personal-loan obligations from a previous job still on the bureau count.

- Employment changes during the application. Switching from salary to commission, taking a new job in a different industry, leaving a job to start a business. Each one resets the income-stability clock. Underwriters generally want at least two years in the same line of work for variable-income files and three months in a new salaried role.

- Appraisal coming in below the purchase price. The lender will only lend against the lower of the appraised value or the purchase price. An appraisal gap shifts the cost to the borrower (larger down payment) or requires a price renegotiation with the seller.

The first four are knowable before the file goes to underwriting. The fifth is the one borrowers cannot fully control, but a realistic offer (informed by recent comparable sales) reduces the risk substantially.

What insured underwriting adds

If the down payment is below 20%, the mortgage must be insured. The three Canadian mortgage default insurers, CMHC, Sagen, and Canada Guaranty, each run their own underwriting layer on top of the lender's. They share most rules with B-20 but apply tighter caps in places (often 39% / 44% becomes 35% / 42%, and the maximum amortization is 25 years on insured purchases under most programs). The underwriter at the lender pre-checks the file against the insurer's rules before submitting; if the lender's underwriting clears, the insurer's almost always does too.

The MIE channel (private mortgage investment entities) operates outside B-20 and is the worst-performing slice of the chart above, with 1.96% of balances 90+ days delinquent in Q3 2025 (CMHC). If your file does not fit a chartered bank, your file is more likely to default, which is also why the rates at MIE lenders are higher.

How to walk into underwriting with the right file

Five steps remove the avoidable failure modes before the underwriter ever sees the file.

- Pull your own credit report from Equifax and TransUnion two to three months before applying. Address any errors, settle any open collections, and let the report refresh.

- Document your down payment trail. Save the last 90 days of statements for every account the funds will come from. If any portion is gifted, get a signed gift letter from the source named on the title.

- Pause job changes. Stay in the same role from application to closing if at all possible. If a job change is unavoidable, tell the broker the day it happens, not the week of closing.

- Stop opening new credit. No car loan, no new credit card, no buy-now-pay-later from the day you submit the application until the day the mortgage funds.

- Run your own GDS and TDS. Use the FCAC calculator with your real numbers, the qualifying rate (max(contract + 2%, 5.25%)), and the property tax estimate for the property you are buying. If you are over the caps, you know before the underwriter does.

A clean file with these five items handled is, in the data, an extremely strong candidate. The 99.76% of Canadian chartered-bank mortgages that are current on their payments started here.

When worry is rational

There are real cases where some worry is justified. Self-employed borrowers in their first or second year of business, borrowers with a recent consumer proposal, borrowers whose income depends on a single client, borrowers with thin or rebuilding credit files, and borrowers buying non-standard property (acreage, mixed-use, manufactured housing) all face higher friction. None of these mean the file cannot be approved; they mean the lender choice matters more, the conditions list will be longer, and the borrower's preparation makes a larger difference.

If your file is in one of these categories, the rational move is not to worry less. It is to work with a broker before the application, to know which lenders accept your profile, and to assemble the file the underwriter will ask for in advance. Most files in these categories that present clean documentation get approved. Most that do not present clean documentation get declined, regardless of the underlying numbers.

What "approved with conditions" usually means

Conditional approval is the default, not the exception. When the underwriter issues a conditional approval, the list of conditions usually falls into three groups:

- Standard documentation conditions (most common): a current paystub, a recent NOA, a property tax bill, an updated bank statement, a void cheque. These almost always clear.

- Verification conditions: an employment letter signed by HR, a confirmation of down-payment source, a survey of the property, a status certificate for a condo. These usually clear, sometimes with delays.

- Structural conditions (least common): a co-signer to bring the file inside ratios, a larger down payment, a reduced amortization, a different property. These require the borrower to change something material about the deal.

The conditions list itself is not a warning sign. Files with zero conditions are rare and usually involve very low loan-to-value, very strong income, and very clean credit. Two to ten conditions is normal. The work is in clearing them quickly so the closing calendar does not slip. How fast those conditions get cleared is also what drives how long underwriting takes overall.

The bottom line on worry

The base rate of trouble at Canadian mortgage underwriting is low, and most of the friction borrowers experience is either documentation or math, both of which are manageable. Worry without a specific cause is wasted; preparation is not. Pull your credit, calculate your ratios, document your down payment, stay in your job, stop opening new credit, and pick a lender that fits your file. The underwriter's main task is to confirm that the math works at the qualifying rate; your job is to make sure they can.