What is the current prime interest rate?

The current US prime interest rate is 6.75%, effective December 11, 2025. It has held at that level since the Federal Open Market Committee cut the federal funds target range by 25 basis points at its December 2025 meeting and the 30 largest US banks moved their own prime rates in step (Federal Reserve H.15).

The number you see published in the Wall Street Journal, on bank rate pages, and in your credit card disclosure is the US Prime Rate, sometimes written as the WSJ Prime Rate. It is a single benchmark that commercial banks use as a reference for short-term, variable-rate consumer and business borrowing. It is not the rate the Federal Reserve charges. It is not the rate banks charge each other. And, as the next section explains, it is almost never the rate you actually pay.

Here is how today's prime rate compares to the recent past:

| Date | US prime rate | What moved |

|---|---|---|

| December 11, 2025 | 6.75% | Fed cut funds rate 25 bps |

| September 18, 2025 | 7.00% | Fed cut funds rate 25 bps |

| December 19, 2024 | 7.25% | Fed cut funds rate 25 bps |

| November 7, 2024 | 7.50% | Fed cut funds rate 25 bps |

| September 18, 2024 | 7.75% | Fed cut funds rate 50 bps |

| July 27, 2023 | 8.50% | Fed hike, then a long pause |

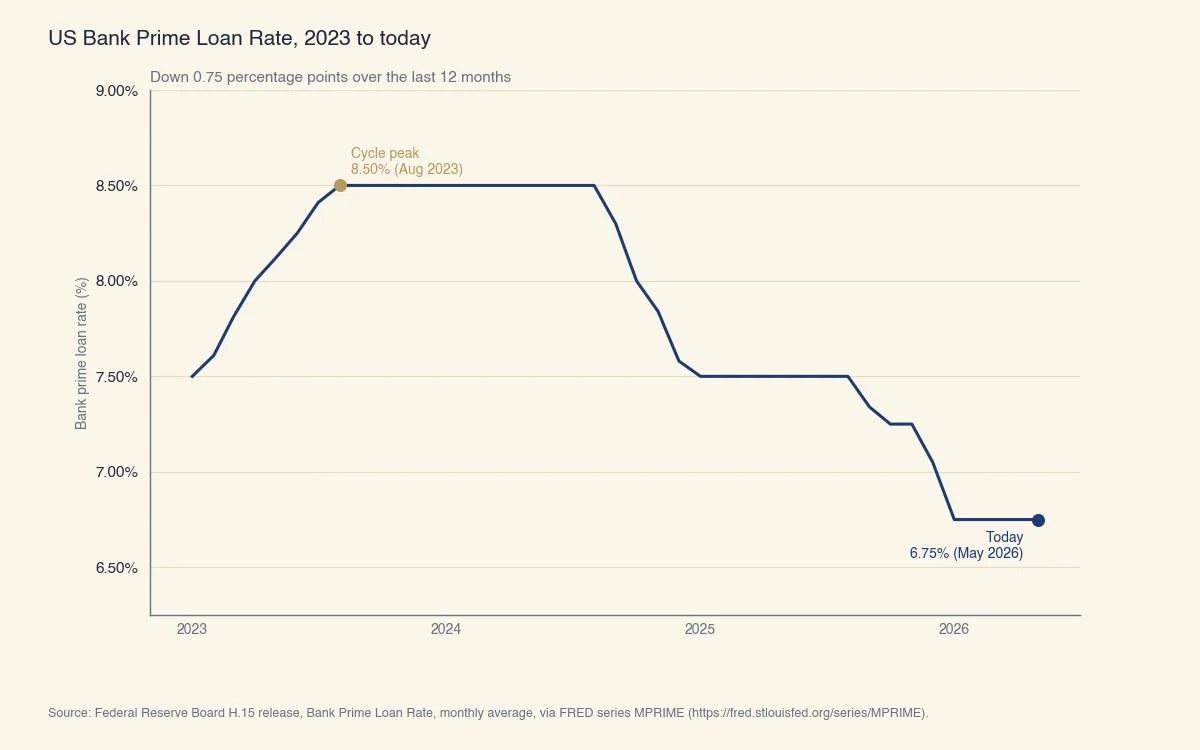

The FRED series DPRIME publishes the same number daily and runs back to 1955 (FRED, Federal Reserve Bank of St. Louis). The chart below puts the current 6.75% level in the context of the past three years of policy moves.

Source: Federal Reserve Board H.15 release, Bank Prime Loan Rate, monthly observations from January 2023 through May 2026.

Why the prime rate is not your rate

The prime rate is a benchmark, not a price tag. Almost every variable-rate consumer product is quoted as Prime plus a margin, and that margin is what actually determines what you pay. Reading the prime rate off the Federal Reserve website tells you the floor that the largest banks use among themselves. It does not tell you what your HELOC, credit card, or business line of credit costs.

The structure is consistent across product types. The lender writes the contract as:

Your APR = US Prime Rate + Margin

The margin is the spread the lender adds on top of prime; understanding interest rate versus APR explains why your posted rate and your APR can differ. It is fixed in your contract (for most variable products), but it varies between products and between borrowers. A super-prime credit card might price at Prime + 9%; a subprime card at Prime + 24%. A HELOC for a borrower with strong equity might price at Prime + 0.5%; a small business line of credit at Prime + 1.5% to Prime + 3%.

This is required to be disclosed up front. Under Regulation Z, the federal Truth in Lending rule that governs consumer credit disclosures, the lender must specify both the index (the prime rate) and the margin in the credit agreement (CFPB Regulation Z). If you cannot tell what the margin is on your current credit card, check the section of your cardholder agreement titled "How we calculate your variable APRs."

The practical consequence: when the Fed cuts the federal funds rate by 25 basis points, the prime rate drops 25 basis points, and your variable APR drops 25 basis points (on the next statement cycle). The cut does not change your margin. A subprime borrower paying Prime + 22% before a cut still pays 22% over prime after the cut. Lenders price the relative risk in the margin, and that part of the formula moves only when you refinance or when the lender re-prices the entire product.

What does today's prime rate actually cost you?

At 6.75% prime, a typical variable-rate product carries an APR between roughly 7.25% and 22% depending on the margin written into your contract. The table below works the math for three common variable products at the current prime rate.

| Product | Typical margin | APR at 6.75% prime | Interest on a $10,000 balance per month |

|---|---|---|---|

| HELOC (strong borrower) | Prime + 0.50% | 7.25% | $60.42 |

| HELOC (average borrower) | Prime + 2.50% | 9.25% | $77.08 |

| Variable-rate credit card (good credit) | Prime + 11.99% | 18.74% | $156.17 |

| Variable-rate credit card (average) | Prime + 14.99% | 21.74% | $181.17 |

| Small business line of credit | Prime + 2.00% | 8.75% | $72.92 |

Monthly interest is computed as Balance × APR / 12. Credit cards usually compound daily, so the effective cost is slightly higher than the table shows; HELOCs and business lines usually charge simple monthly interest on the average daily balance.

The numbers move with the index, not with the margin. If the Fed cuts at the next meeting and the prime rate drops to 6.50%, the same HELOC at Prime + 2.50% drops to 9.00% APR, saving about $2.08 per month per $10,000 borrowed. If prime rises 50 basis points instead, the same HELOC would cost about $4.17 more per month per $10,000 borrowed.

This is the answer to the most common follow-up question after "what is the prime rate today" (namely, "is that what I'm paying?"). The answer is almost always no, and the gap between the published prime and your actual APR is the lender's margin.

How is the US prime rate set?

The US prime rate is set by commercial banks, not by the Federal Reserve, but it tracks the federal funds rate so closely that the two move in lockstep. Here is the mechanism, in three steps.

Step 1: The FOMC sets the federal funds target

Eight times a year, the Federal Open Market Committee (FOMC) votes on a target range for the federal funds rate (FOMC calendar). The federal funds rate is what banks charge each other for overnight loans of reserves at the Federal Reserve. The current target range is 4.25%–4.50%, set at the December 2025 meeting.

Step 2: Banks set their own prime rate

Each commercial bank publishes a prime rate that it uses as a reference for its best-customer short-term lending. By long-standing convention, US banks set their prime at the upper bound of the federal funds target range plus 3 percentage points. With the funds target at 4.25%–4.50%, the math is 4.50% + 3.00% = 7.50%, but banks have actually held prime at 6.75% since December 2025, which reflects a market convention closer to the midpoint of the target range plus 3% (4.375% + 3.00% ≈ 7.375%, rounded to the 6.75% level adopted across the major banks). The number depends on which large banks anchor the market in a given cycle.

In practice, all 30 of the largest US banks change their prime rate on the same day after an FOMC move, because the index is meaningless if rivals disagree on it.

Step 3: The Wall Street Journal publishes the official benchmark

The Wall Street Journal surveys the 30 largest US banks. When at least 23 of them have changed their published prime rate, the Journal updates its US Prime Rate, and the new figure becomes the index that most consumer disclosures reference (Wall Street Journal Money Rates). This is the number you see quoted as "the" prime rate. Your credit card agreement, your HELOC disclosure, and most business line of credit contracts cite the WSJ Prime Rate by name.

The Federal Reserve does not set the prime rate. The Federal Reserve sets the federal funds rate. The prime rate is downstream of that decision.

Which products move with the prime rate?

Most short-term variable consumer and small business credit is tied to the prime rate; long-term fixed-rate products are not. Variable-rate borrowing is roughly 30% of US household debt at the time of writing, with credit cards and HELOCs dominating that mix.

Products that almost always move with prime:

- Variable-rate credit cards (covers about 90% of US credit card balances)

- Home equity lines of credit (HELOCs)

- Variable-rate private student loans

- Small business lines of credit

- Variable-rate auto loans (less common but exists at credit unions)

- Personal lines of credit

Products that almost never move with prime:

- Fixed-rate mortgages (priced off the 10-year Treasury, not prime)

- Adjustable-rate mortgages (priced off SOFR since 2020, not prime)

- Federal student loans (priced off the 10-year Treasury at origination, then fixed)

- Fixed-rate auto loans (priced off the lender's cost of funds and credit risk)

- Fixed-rate personal loans

The split matters because it tells you which parts of your debt portfolio will respond to a Fed cut and which parts will not. A homeowner with a 30-year fixed mortgage and a HELOC will see no change in the mortgage payment after a cut but will see the HELOC rate drop on the next statement.

When does the prime rate change next?

The prime rate changes only when the FOMC moves the federal funds rate, which can only happen at one of the eight regularly scheduled FOMC meetings or at an unscheduled meeting in a crisis. The next FOMC meetings in 2026 fall on June 16-17, July 28-29, September 15-16, October 27-28, and December 15-16 (FOMC calendar).

The CME FedWatch tool tracks Federal Funds futures prices in real time and translates them into market-implied probabilities for each upcoming meeting. As of late May 2026, the market is pricing in a roughly 60% probability of a 25 basis point cut at the June 2026 meeting, which would move prime from 6.75% to 6.50% the same day. These probabilities update minute by minute and shift sharply on new inflation or labor market data, so check them close to the meeting if you are timing a variable-rate decision.

If you are deciding whether to lock a fixed rate, refinance a HELOC, or pay down a variable-rate balance, the question is not "what is the prime rate" but "what is the prime rate likely to be in 6 to 18 months." That depends on the FOMC's inflation outlook, not on the current spot rate.