What does "underwriting in business development" mean?

In commercial banking, underwriting in business development refers to commercial loan underwriting: the lender's risk decision on whether to fund a business loan, at what rate, and on what terms. The deal is sourced and structured by a business-development team, then decided independently by a credit underwriter. The two functions are deliberately kept separate inside every Canadian chartered bank.

The keyword reveals a common misconception. Many readers assume "underwriting" and "business development" are the same activity. They are not. Business development (BD) is the revenue-generating function: BD officers find borrowers, build the relationship, structure the deal, and recommend it forward. Underwriting (also called "credit" or "credit risk") is the approval function: a credit officer or credit analyst reviews the file against the lender's risk policy and signs the decision. The same person never holds both roles because the same person should not both pursue revenue and approve risk.

Why the split matters in practice: the BD officer is your contact for the deal but does not approve it. Your file moves to a separate desk, often in a different city, for the credit decision. The two desks may agree, or the credit officer may push back on the BD officer's structure, ask for additional collateral, or decline outright. The borrower-facing language ("we have approved your loan") usually credits BD, but the decision authority sits in credit.

Who is the business-development officer in a Canadian bank?

At the Big Five Canadian chartered banks (RBC, TD, BMO, Scotiabank, CIBC), the business-development function carries different titles depending on deal size:

- Account Manager Small Business for revenue under roughly $5 million

- Commercial Account Manager for revenue $5 million to $50 million

- Vice President Commercial Banking for revenue above $50 million

- Director Corporate Banking for syndicated and capital-markets-adjacent deals

In each case, the BD officer is your relationship contact. The credit decision sits with a separate Credit Officer (small business) or Credit Director (mid-market and corporate) who often never speaks to the borrower directly.

How does commercial underwriting differ from personal underwriting?

Commercial underwriting uses the same 5 Cs framework as consumer underwriting but applies each one differently, weights cash flow over credit score, and almost always requires a personal guarantee. The mechanics shift in three concrete ways.

First, Capacity is measured by Debt Service Coverage Ratio (DSCR) instead of personal Debt-to-Income. DSCR equals trailing EBITDA divided by annual debt service. Canadian commercial banks generally require DSCR of at least 1.25 for term debt. A DSCR below 1.10 typically pushes the deal toward alternative lenders or BDC's complementary financing.

Second, the underwriter pulls both business and personal credit:

| Credit type | Source | What it measures |

|---|---|---|

| Personal credit | Equifax Canada, TransUnion Canada | Owner's track record on consumer credit (cards, mortgages, auto, lines of credit) |

| Business credit (Canada) | Equifax Canada Commercial | Trade-payment history of the business with suppliers |

| Business credit (US-rooted) | Dun & Bradstreet PAYDEX | International trade-payment history; widely used by Canadian banks for export-exposed borrowers |

| SMB scorecard | Fair Isaac SBSS (FICO Small Business Scoring Service) | Combined personal + business model, 0 to 300 scale, used by many lenders to fast-track decisions under $100k |

The two credit pulls run in parallel and are weighted differently depending on business age. For an established business (2+ years of audited statements), business credit and cash flow dominate. For a newer business or sole proprietor, personal credit carries most of the weight.

Third, Collateral and the personal guarantee work together, not separately. Most Canadian SMB loans take security on business assets (a General Security Agreement covering inventory, receivables, equipment) AND a personal guarantee from each owner holding more than 20% equity. Incorporating the business does not shield the owner's personal credit from the underwriting review, because the underwriter pulls personal credit as part of evaluating the guarantee.

The 5 Cs of credit, commercially applied

| The 5 Cs | Consumer application | Commercial application |

|---|---|---|

| Character | Personal credit score and payment history | Owner's personal credit + business payment history with suppliers + management resume |

| Capacity | Debt-to-Income on personal income | DSCR on business EBITDA, trailing 12 months |

| Capital | Down payment and personal savings | Owner's equity in the business; retained earnings |

| Collateral | The asset purchased (home, car) | General Security Agreement on business assets + specific collateral for the purpose |

| Conditions | Loan purpose + macroeconomic context | Loan purpose + industry conditions + business cycle + management quality |

The framework is taught in every Canadian commercial credit program (RBC, TD, Scotiabank, BMO, and CIBC all run formal credit-academy programs for analysts in their first 18 to 24 months). It also underlies the published OSFI prudential expectations for bank commercial portfolios (OSFI).

A worked example: $250,000 restaurant expansion loan

Walk a real DSCR calculation, then watch how the deal moves when the requested loan size grows. The mechanics below are how a Big Five commercial credit officer would evaluate this file in 2026.

The scenario. A Toronto-based independent restaurant, incorporated for 4 years, two co-owners (60/40 ownership), trailing 12-month revenue of $1,200,000, audited EBITDA of $180,000. The owners request a $250,000 5-year term loan to renovate the kitchen and add a private dining room. The bank's rate sheet quotes prime plus 3.5% (call it 8.50% with prime at 5.00%) for the credit tier this file is heading into.

Step 1: calculate annual debt service. A $250,000 loan at 8.50% amortized over 5 years (60 months) creates a monthly payment of $5,127, or $61,524 per year.

Step 2: calculate DSCR. $180,000 EBITDA divided by $61,524 annual debt service equals a DSCR of 2.93.

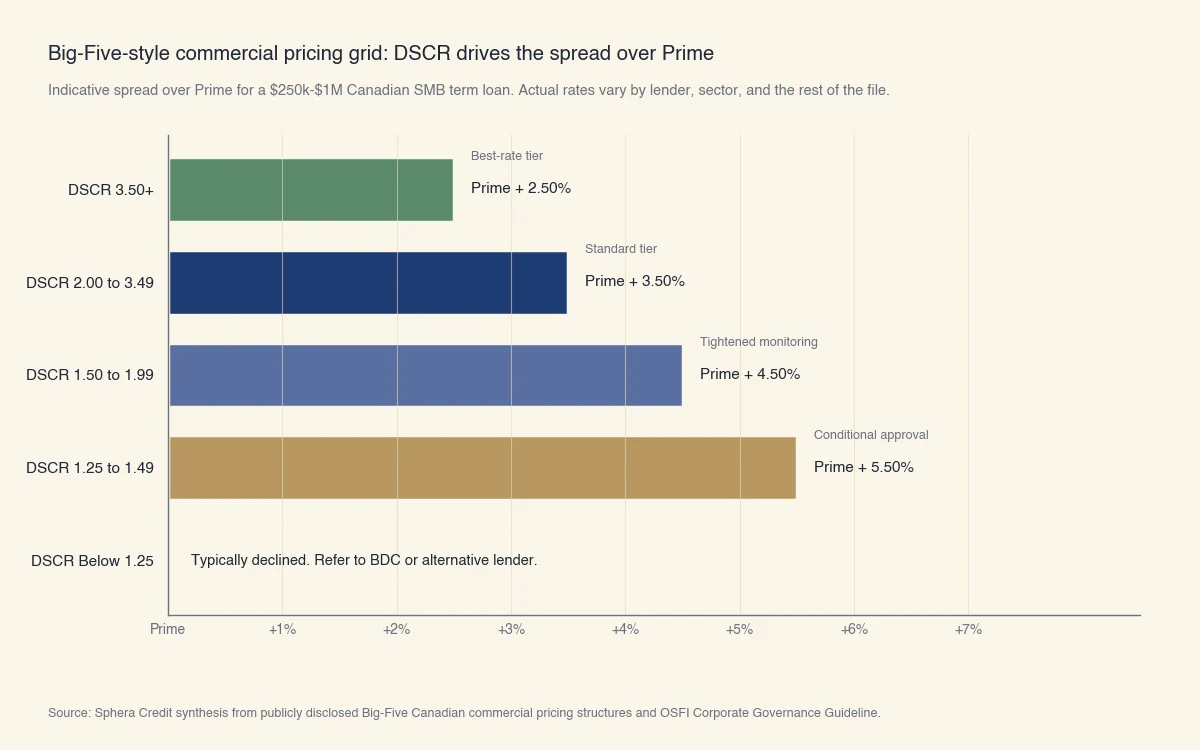

Step 3: map DSCR to the pricing grid. A simplified Big-Five-style pricing grid looks roughly like this:

| DSCR band | Pricing | Decision posture |

|---|---|---|

| 3.50+ | Prime + 2.50% | Best-rate tier, light conditions |

| 2.00 to 3.49 | Prime + 3.50% | Standard tier, normal covenants |

| 1.50 to 1.99 | Prime + 4.50% | Tighter monitoring, may require additional collateral |

| 1.25 to 1.49 | Prime + 5.50% | Conditional approval, often requires CSBFP wrap |

| Below 1.25 | Typically decline | Refer to alternative lender or BDC |

At DSCR 2.93, this file sits in the Standard tier and the bank's quoted rate (Prime + 3.50% = 8.50%) holds.

Step 4: add the personal-guarantee requirement. Both owners hold more than 20% equity, so both sign full personal guarantees. The underwriter pulls Equifax Canada personal credit on each owner and checks for clean payment history over the past 24 months.

Step 5: layer the collateral. A standard General Security Agreement registers a first-priority lien on the restaurant's business assets (inventory, receivables, equipment, leasehold improvements) at the Personal Property Security Registration in Ontario.

Now flex the deal. Same restaurant, same $180,000 EBITDA, but the owners ask for $500,000 instead of $250,000. The new annual debt service at 8.50% over 5 years is $123,000, so DSCR drops to 1.46. The file moves from the Standard tier into the Conditional-Approval tier. The bank now wants either an extra $200,000 of real-estate collateral (the owners' residential property, which the owners almost never accept), or a CSBFP partial-guarantee wrap on the loan, or both. Pricing widens from Prime + 3.50% to Prime + 4.50%. If the owners can not produce the additional collateral and the file does not fit CSBFP eligibility, the underwriter declines.

The arithmetic shows why DSCR is the dominant variable for established businesses. A 25 basis-point change in interest rates moves the calculation only slightly. A doubling of the loan size moves it materially.

Source: Sphera Credit synthesis based on Big-Five Canadian chartered bank commercial pricing structures and OSFI Corporate Governance Guideline prudential expectations.

How does commercial underwriting work in Canada?

Canadian commercial underwriting runs through three distinct institutional channels: the Big Five chartered banks, the federal Crown corporation BDC, and credit unions or alternative lenders. Each channel has its own underwriting standard and pricing grid, and the same borrower can receive materially different decisions across them.

The Big Five chartered banks

Royal Bank (RBC), Toronto-Dominion (TD), Bank of Montreal (BMO), Scotiabank, and CIBC underwrite most Canadian commercial lending. Their commercial divisions follow internal credit policies anchored to OSFI's prudential framework. The credit policy at each bank is confidential, but the structural elements (DSCR floors, personal guarantee thresholds, GSA standard, covenant package, pricing grid) are broadly comparable. Statistics Canada's Survey on Financing and Growth of Small and Medium Enterprises reports that roughly 90% of Canadian SMBs that successfully obtain debt financing use a chartered bank or credit union as the primary lender (Statistics Canada).

BDC: the federal Crown corporation

BDC is the Business Development Bank of Canada, a federally owned development-finance institution. BDC underwrites complementary financing for SMBs whose risk profile falls outside the Big Five's appetite. The institution is mandated by federal statute to act as a lender of last resort for SMBs with viable business plans but credit profiles that chartered banks decline (BDC). BDC's underwriting accepts lower DSCR (often down to 1.10), higher leverage, and earlier-stage businesses, but typically prices 100 to 300 basis points above the chartered banks for comparable size and term.

CSBFP: the partial-guarantee program

The Canada Small Business Financing Program (CSBFP) is a federal partial-guarantee program administered by Innovation, Science and Economic Development Canada and accessed through participating chartered banks, credit unions, and caisses populaires. Eligible SMBs can borrow up to $1.15 million per loan. If the borrower defaults, the federal government reimburses the lender for 85% of the realized loss (ISED). The borrower pays a 2% upfront registration fee and a 1.25% annual administration fee on the outstanding balance. The program is the closest Canadian analogue to the US SBA 7(a) loan but the mechanics differ in important ways: CSBFP funds must be used for fixed assets, leasehold improvements, or intangibles (not working capital), and the eligible categories are narrower.

Alternative and online lenders

A growing layer of alternative lenders (Lendified, Thinking Capital, Merchant Growth, OnDeck Canada, and several US-rooted platforms operating in Canada) underwrites using cash-flow data from bank-account aggregation rather than full financial statements. Funding times of 1 to 5 business days are common. Pricing is materially higher (effective annual rates of 18% to 60%, sometimes higher in the form of factor-rate merchant-cash-advance structures). The trade-off is speed and access for the borrower at the cost of higher carrying cost.

For the underwriting framework that applies on the consumer side of Canadian lending and how it differs from the commercial framework above, see what is underwriting and how long does underwriting take. For the plain-language meaning of the term itself, see what does underwrite mean.

What does a commercial underwriting decision actually contain?

A commercial underwriting decision is not a single yes or no. It is a structured offer that combines pricing, term, collateral, covenants, and conditions precedent. Borrowers who expect a simple approval letter are often surprised by the document a Canadian bank actually delivers.

The components of a typical approved commercial decision:

- Pricing. Stated as Prime plus a spread, or as a fixed rate locked at funding. Most term debt is variable; most CSBFP-backed loans are fixed.

- Term and amortization. Term is the period before the loan renews or matures; amortization is the payment schedule. A common structure is a 5-year term with a 15-year amortization, with a balloon at maturity.

- Collateral and security. General Security Agreement, specific collateral, real-estate mortgages, and (for syndicated deals) inter-creditor agreements.

- Personal guarantees. From each owner above the 20% threshold, sometimes limited in amount or duration.

- Affirmative covenants. Reporting requirements (quarterly financial statements, annual audited statements, tax-compliance certificates) and operational requirements (insurance, environmental compliance, minimum DSCR maintenance).

- Negative covenants. Restrictions on additional borrowing, dividends, asset sales, and changes of ownership without lender consent.

- Conditions precedent. Items the borrower must satisfy before the loan funds: corporate authorizations, legal opinions, insurance certificates, title searches, lien searches at the Personal Property Security Registration (PPSR), independent appraisals for material collateral.

A typical Canadian commercial credit-approved file runs to 30 to 80 pages of documentation. The reading is technical but every clause exists because at some point a previous deal failed in a specific way. The covenants section in particular is where most of the post-funding monitoring lives. A missed quarterly statement or a covenant breach (typically a DSCR breach below the contracted floor) gives the lender the right to demand the loan or restructure on tighter terms.

The Bank of Canada's Financial Stability Report tracks commercial-credit conditions and recent default trends at the system level (Bank of Canada). For an individual borrower the document on your desk matters more than the system aggregate, but the system context shapes how aggressively or cautiously lenders enforce their covenant package across the cycle.

Commercial underwriting rewards preparation. The borrowers who get the cleanest decisions are the ones whose financial statements reconcile to their tax returns, whose monthly bookkeeping is current, and who can answer the credit officer's questions on cash flow without having to look anything up. The mechanics of the decision are not mysterious. They are documented, applied consistently, and assessed against measurable thresholds the borrower can plan for.