How do you check your credit score in Canada?

You have three free paths: sign up directly with Equifax Canada or TransUnion Canada, use a free third-party app like Borrowell or Credit Karma Canada, or check it inside your bank app. Every Big Six bank except National Bank now offers a free in-app credit score. Every one of these is a soft inquiry and has no impact on your score (FCAC).

One important calibration before you pick a method: the score the lender pulls when you apply for a mortgage or car loan is not necessarily the score any of these tools shows you. Bureau-direct and consumer-app scores are educational. Lenders run their own score, almost always a FICO model from whichever bureau they have a contract with, at the moment you formally apply. The consumer score is a strong proxy but rarely an exact match.

A credit score in Canada is a three-digit number from 300 to 900 that summarises how reliably you have repaid borrowed money. Two credit bureaus maintain it: Equifax Canada and TransUnion Canada. Both calculate scores from your credit report data using their own models, and the two numbers usually differ by 20 to 40 points because the underlying data and the models are not identical.

Which path should you use first?

Pick the method that matches your situation:

- You want a thorough first look: Sign up with Equifax Canada directly (free monthly Equifax score) and pair it with Borrowell (free weekly Equifax score with weekly alerts). You will see both your score and your full report.

- You bank with RBC, TD, BMO, CIBC, or Scotiabank: Open your bank app. Your free monthly TransUnion score is already there via CreditView. Pair with Borrowell if you also want the Equifax side.

- You bank with National Bank or a credit union: Use Borrowell plus Credit Karma Canada. You get free coverage from both bureaus with no bank-app shortcut.

- You are in Quebec: TransUnion Canada offers free online score access only to Quebec residents under provincial consumer-reporting rules. Use both TransUnion direct and Equifax direct to see both bureaus for free.

How can you check your credit score for free?

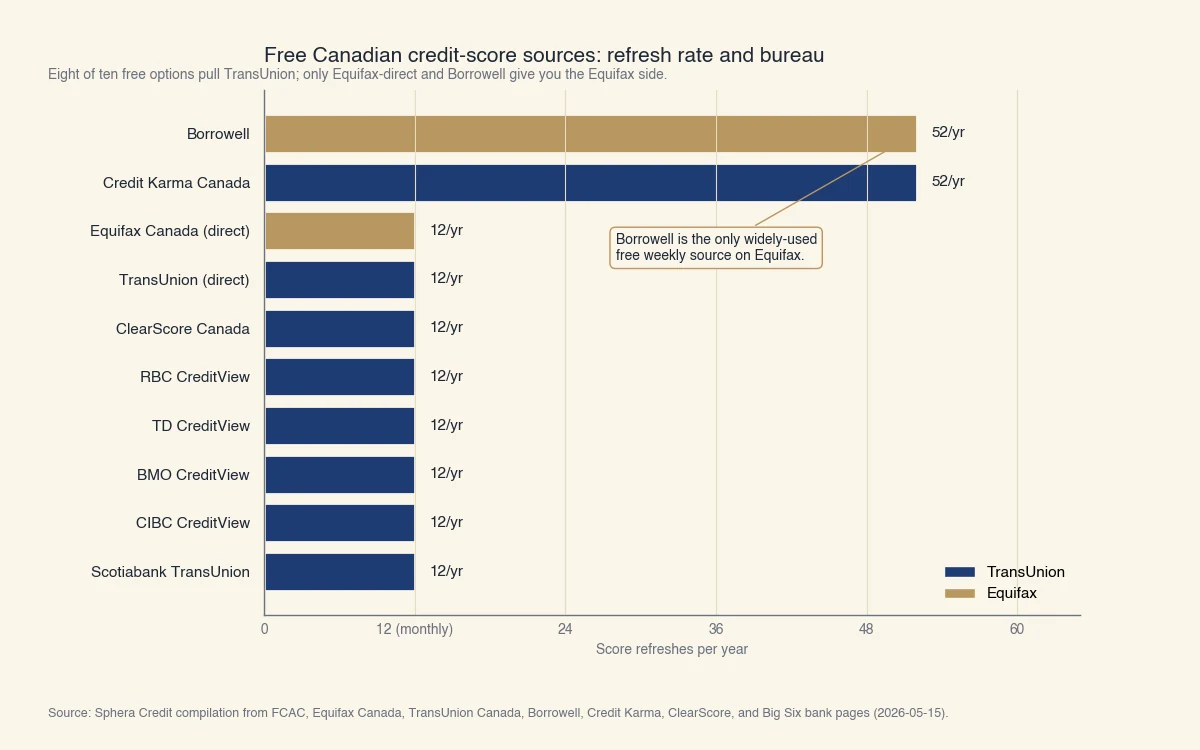

Six legitimate sources give Canadians a free credit score: Equifax Canada direct, TransUnion Canada direct, Borrowell, Credit Karma Canada, ClearScore, and any Big Six bank app except National Bank. None require a credit card and none use a trial-then-charge model. Different sources use different bureaus and refresh at different cadences, so the score you see depends on which one you open (Equifax Canada, Borrowell).

The complete map of free sources in Canada:

| Source | Bureau used | Refresh | What you see | Catch |

|---|---|---|---|---|

| Equifax Canada direct | Equifax | Monthly | Full Equifax score + report (payment history detail limited on free tier) | Paid tiers push monitoring add-ons |

| TransUnion Canada direct | TransUnion | Monthly | Full TransUnion score + report | Free online tier limited to Quebec residents |

| Borrowell | Equifax | Weekly | Equifax score + product offers | Income-from-affiliate offers; ignore if not relevant |

| Credit Karma Canada | TransUnion | Weekly | TransUnion score + report + offers | Income-from-affiliate offers; ignore if not relevant |

| ClearScore Canada | TransUnion | Monthly | TransUnion score + report | Smaller user base, fewer educational features |

| RBC CreditView | TransUnion | Monthly | TransUnion score + simulator | RBC Online Banking client only; web-only access |

| TD CreditView | TransUnion | Monthly | TransUnion score + history | TD client only; in-app and web |

| BMO CreditView | TransUnion | Monthly | TransUnion score + report | BMO Digital Banking client only |

| CIBC CreditView | TransUnion | Monthly | TransUnion score + report | CIBC Online or Mobile Banking client only |

| Scotiabank TransUnion Credit Score | TransUnion | Every 30 days | TransUnion score + report + history | Scotia client only; sign-in required |

| Free annual mailed report | Equifax or TransUnion | Once per year | Full report (most complete version) | Mailed; allow ~4 weeks for delivery |

A practical reading of the table: most free Canadian options are TransUnion-based because five of the six Big Six banks chose TransUnion as their consumer-score partner. The most prominent free Equifax option is Borrowell, which is why Borrowell has grown to be the most-used free credit score app in the country.

Source: Sphera Credit compilation from FCAC, Equifax Canada, TransUnion Canada, Borrowell, Credit Karma Canada, ClearScore, RBC, TD, BMO, CIBC, and Scotiabank consumer-facing product pages as of 2026-05-15.

What does each bureau actually give you on the free tier?

The free tier from each bureau gives you the score plus the bulk of the report, but not the payment-history payment-by-payment detail that the mailed annual report includes. Equifax Canada notes that its free online report "excludes payment profile tables" spanning up to 25 months. If you are checking your credit because you suspect a missed payment is being reported incorrectly, request the mailed report so you get the full history view (Equifax Canada).

How do you check your credit score through your bank?

Five of Canada's Big Six banks (RBC, TD, BMO, CIBC, Scotiabank) offer a free in-app credit score via TransUnion's CreditView; National Bank does not provide one and directs customers to request a report from Equifax or TransUnion directly. All five bank-app scores update once a month, are soft inquiries with no impact on your score, and are accessible inside the same banking interface you already use (CIBC).

How to find it in each bank's app:

- RBC: Sign in to RBC Online Banking on the web (RBC's CreditView is web-only). In the dashboard, look for "Credit Score" under Services or in your accounts overview.

- TD: Open the TD app, tap "More" in the bottom navigation, then "TD CreditView". The TransUnion score appears on the dashboard.

- BMO: Open BMO Digital Banking on web or mobile, tap the "More" menu, then "My Credit Score". Access requires that you are enrolled in BMO Digital Banking.

- CIBC: Open CIBC Online Banking or the CIBC Mobile Banking App, navigate to "Credit Score" in the dashboard. The CreditView dashboard shows the TransUnion score plus the report.

- Scotiabank: Open the Scotia app, tap "Advice+" in the main navigation, then "TransUnion credit score", then "Credit score report". On the web, select "See your credit score" from the Accounts page.

- National Bank: No in-app score. National Bank's help-centre article directs customers to Equifax (1-800-465-7166) or TransUnion to request a report.

Why do all the bank apps show the TransUnion score?

CreditView is a TransUnion product that TransUnion has licensed to most major Canadian financial institutions, which is why it appears with the same brand inside multiple bank apps. There is no equivalent dominant Equifax-distributed product on the bank side. If your bank app shows you a TransUnion score and you want the Equifax side as well, Borrowell is the standard free choice for Equifax coverage.

Why is my credit score different in different places?

Three things move independently: the bureau holds slightly different data, the scoring model weights factors differently, and the refresh date varies by source. A 730 from Borrowell on a Tuesday and a 715 from your bank app on Wednesday can both be technically correct. This is the single biggest source of confusion when consumers first start checking their score, and almost no provider explains it on their own page (FCAC).

Concretely, here is the same person checking their score from four free sources on the same day:

- Borrowell: 728 (Equifax, refreshed Sunday)

- CIBC CreditView: 715 (TransUnion, refreshed last month)

- Equifax direct: 731 (Equifax, refreshed this morning)

- Credit Karma Canada: 718 (TransUnion, refreshed last night)

All four numbers are correct snapshots of two different bureaus on two different days. The lender pulling a fresh FICO model at the moment of application would see something else again, usually within 10 to 30 points of the consumer scores but not identical.

Which score do lenders actually use?

Most Canadian lenders pull a FICO Score at the moment of application, almost always FICO Score 8 or FICO Score 9, from whichever bureau they have a contract with. Auto lenders often pull a FICO Auto Score (a tuned variant). Mortgage underwriters at the Big Six usually pull all three of FICO from Equifax, FICO from TransUnion, and the bureau's own score, and then use the middle number. The free bureau-direct score is the closest analogue to what the lender sees; consumer-app scores are slightly further away.

The takeaway: use the free tools to track the trend, not the exact number. If your bureau-direct score moves from 670 to 720 over six months, the lender-pulled score has also moved up. If you are within a few points of a key threshold (e.g., 680 for a prime mortgage), pull the bureau-direct report and read the detail rather than trusting a single consumer-app number.

Does checking your credit score lower it?

No. Checking your own credit score is a soft inquiry and has no impact on your score. Only hard inquiries (when a lender pulls your credit because you formally applied for credit) affect your score, and even then typically only by a few points for a few months. Soft inquiries include every consumer-facing tool listed in this article, employer background checks, and pre-approved credit offers (FCAC).

The two kinds of inquiry, side by side:

| Inquiry type | Triggered by | Visible to lenders | Impact on score |

|---|---|---|---|

| Soft | Your own check, app pulls, employer screening, pre-approved offers | No | None |

| Hard | Loan / credit-card / mortgage / lease application you submit | Yes, for 2-3 years | Usually 5-15 points, recovers within months |

A common worry is "if I check it multiple times, do those add up." They do not. Soft inquiries simply do not enter the score calculation. You can check your score every day for a year and the score will not move because of the checks themselves.

Where multiple inquiries do matter is during rate shopping. Several hard inquiries for the same product type (mortgage, auto) inside a short window (14-45 days depending on the score model) are typically deduplicated and counted as a single inquiry, so shopping multiple lenders for one loan does not multiply the hit. Different products in the same window (a credit card application during a mortgage shopping window) are each counted separately.

For more on how the score is calculated and what counts as a good number, see what is a good credit score. For what to do if you check your score and find it lower than expected, see how to increase your credit score and why is my credit score going down. If you are checking before financing a vehicle, see what credit score is needed for a car.