Is a 900 credit score possible in the United States?

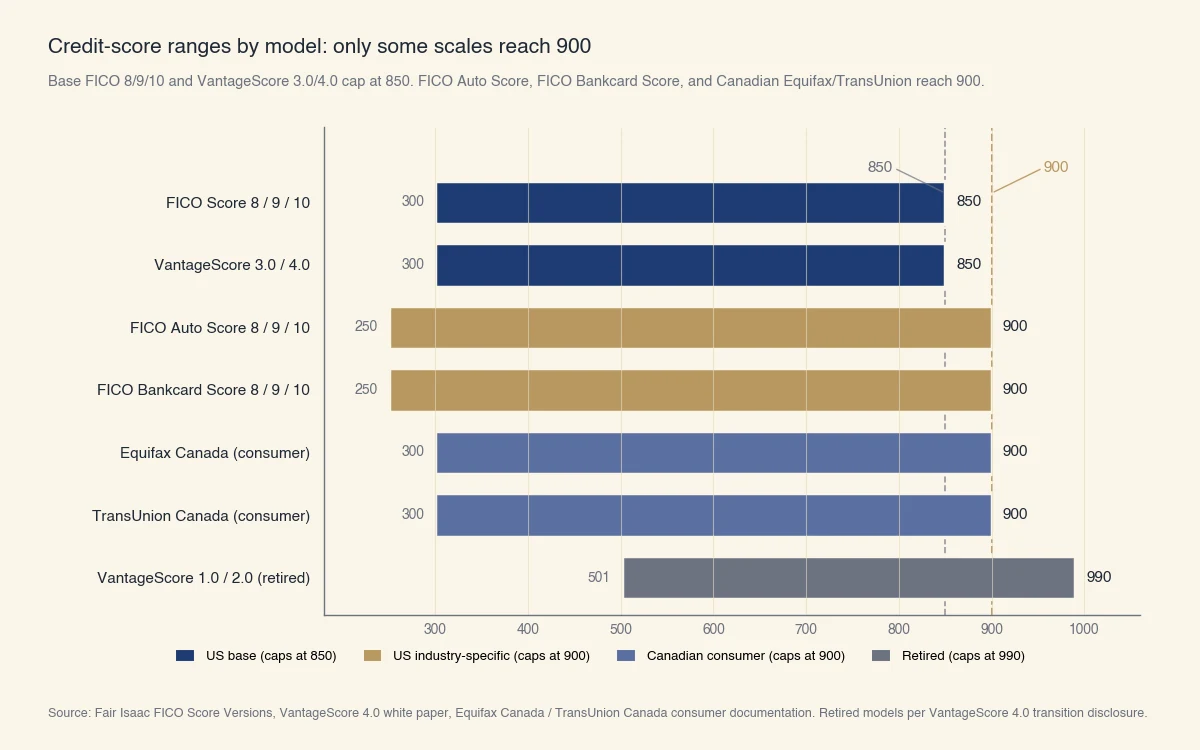

On the base FICO Score and VantageScore scales that almost every consumer sees, no. A 900 is only reachable on industry-specific FICO Auto Score and FICO Bankcard Score, which use a 250 to 900 range that very few people ever view directly. Base FICO 8, 9, and 10, along with VantageScore 3.0 and 4.0, all cap at 850 (Fair Isaac, VantageScore).

The distinction between base and industry-specific FICO scores is the source of most of the confusion. Base FICO Score is the general-purpose score used for most consumer decisions: it summarizes your overall credit risk and is what you see in your bank app, on Credit Karma, or in your annual free credit report. Industry-specific FICO Score is a separate model calibrated for a particular product type (auto loans, credit cards). It uses the same underlying credit-file data but weights factors differently and reports on a wider 250 to 900 scale.

If you have only ever looked at a free credit-score service, your score cannot exceed 850. If a lender pulled an industry-specific score during an application, that score could theoretically reach 900, but in practice fewer than 1% of consumers ever see one.

Quick reference: every score scale and where it caps

| Scoring model | Status | Range | Max | Where you see it |

|---|---|---|---|---|

| FICO Score 8 | Current base | 300 - 850 | 850 | Free services, bank apps |

| FICO Score 9 | Current base | 300 - 850 | 850 | Some mortgage lenders |

| FICO Score 10 / 10T | Current base | 300 - 850 | 850 | Newer lender pulls |

| VantageScore 3.0 | Current base | 300 - 850 | 850 | Credit Karma, Borrowell USA |

| VantageScore 4.0 | Current base | 300 - 850 | 850 | Newer fintech pulls |

| FICO Auto Score 8 / 9 / 10 | Current industry-specific | 250 - 900 | 900 | Auto-loan underwriting |

| FICO Bankcard Score 8 / 9 / 10 | Current industry-specific | 250 - 900 | 900 | Credit-card underwriting |

| VantageScore 1.0 / 2.0 | Retired | 501 - 990 | 990 | Not in active use |

| Equifax Canada (consumer) | Current (Canada only) | 300 - 900 | 900 | Canadian credit reports |

| TransUnion Canada (consumer) | Current (Canada only) | 300 - 900 | 900 | Canadian credit reports |

Source: Fair Isaac "FICO Score Versions" methodology page, VantageScore 4.0 white paper, Equifax Canada consumer documentation. Retired models per VantageScore 4.0 transition disclosure.

Three reasons people think 900 is possible

Almost everyone searching for "is a 900 credit score possible" arrives from one of three specific points of confusion. Naming each one is the fastest way to settle the question.

You saw a 900-scale score on a Canadian credit-bureau dashboard

Equifax Canada and TransUnion Canada both report consumer scores on a 300 to 900 range. The systems are independent of the US FICO 300 to 850 scale (Equifax Canada). A snowbird, a recent immigrant, or anyone who has ever logged into a Canadian credit-monitoring app and then searched the question in English will see a 900 ceiling that genuinely exists in Canada but does not exist in the United States.

If your credit file is in Canada, 900 is the real ceiling on your consumer score. If your file is in the United States, the same number is unreachable on every score a typical consumer ever views.

You saw a FICO Auto Score or a FICO Bankcard Score

Fair Isaac publishes two families of FICO scores. The base family (FICO 8, 9, 10) is the general-purpose score that most lenders and all consumer-facing services use. The industry-specific family (FICO Auto Score, FICO Bankcard Score) is calibrated for one product type and runs from 250 to 900 instead of 300 to 850.

If a car dealership ran a credit check before financing a vehicle, the score on that lender's screen was very likely a FICO Auto Score 8 or 9, not the same number you see on your bank app. The 900 ceiling on that screen is correct for that specific model but is not the same scale as the score you check at home.

You remember an older model that went up to 990

VantageScore 1.0 launched in 2006 with a 501 to 990 range. VantageScore 2.0 used the same range. Both were deprecated when VantageScore 3.0 launched in 2013 on the 300 to 850 range to align with FICO (VantageScore).

If you remember "scores go up to 990" or saw it referenced in older personal-finance writing, that information was correct at the time but is no longer in use. The current VantageScore 4.0, like FICO 8, 9, and 10, caps at 850.

How do industry-specific FICO scores actually work?

Industry-specific FICO scores use the same credit-file data as base FICO but predict a narrower outcome, which is why their score range is wider. Base FICO predicts the probability that a consumer will become 90+ days past due on any credit account in the next 24 months. FICO Auto Score predicts the same outcome specifically on an auto loan. FICO Bankcard Score predicts it on a credit card (Fair Isaac).

The narrower outcome lets the model use scorecard segmentation more aggressively. A scorecard is a separate sub-model trained on a specific population (in this case, applicants for a specific product type). Segmenting by product lets the model give finer discrimination among the borrowers who matter for that lender's decision, which is why the score range expands from 550 points (300 to 850) to 650 points (250 to 900).

Three practical consequences follow:

- Your auto-loan history weighs more in FICO Auto Score than in base FICO. A spotless string of auto-loan payments lifts your FICO Auto Score by more than it lifts your base FICO. A missed auto payment hurts FICO Auto Score by more than it hurts base FICO.

- Your credit-card history weighs more in FICO Bankcard Score than in base FICO. The same logic applies in reverse: credit-card behaviour matters more in the score the issuer pulls.

- The number itself is not directly comparable across scales. A 750 base FICO and a 750 FICO Auto Score do not mean the same thing about your risk. They are scored on different ranges and against different reference populations.

A consumer who has never had an auto loan can have a strong base FICO but a relatively undefined FICO Auto Score, because the model needs auto-loan-relevant data to discriminate at the high end of its range. The reverse is true for someone who has never used a credit card and is being evaluated for one.

When do lenders actually use the industry-specific scores?

The pattern in the US auto and credit-card markets is roughly:

- Auto lenders. Most US auto lenders pull FICO Auto Score 8 or 9 from one or more of the three bureaus during a loan decision. Some also pull base FICO for context.

- Credit-card issuers. Many large US card issuers pull FICO Bankcard Score 8 in addition to (or instead of) base FICO when deciding on a new application or a credit-limit change.

- Mortgage lenders. US mortgage lenders pull the older "classic" FICO 2 (Experian), 4 (TransUnion), and 5 (Equifax), each on a 300 to 850 scale, per longstanding Fannie Mae and Freddie Mac underwriting rules. They do not use industry-specific scores.

- Personal-loan and BNPL lenders. Most use base FICO 8 or VantageScore 3.0, both 300 to 850.

So while a 900 is technically possible on the auto and bankcard scores, the lenders who pull those scores are the only ones who care about the 900 ceiling, and they only care during their specific product decision.

How rare is a perfect score on any model?

About 1.6% of US consumers reach 850 on base FICO, and the share who reach the corresponding maximum on FICO Auto Score or FICO Bankcard Score is similar. A perfect score is statistically rare because every factor in the model has to be near its best at the moment the score is generated (Experian).

Recent Experian and Fair Isaac figures place the 850-FICO share between 1.3% and 1.7% of US scoreable consumers, depending on the reporting quarter and the credit bureau. The Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit shows a similar concentration at the top of the distribution: most US consumers cluster between 700 and 800, and the share above 800 is roughly 22% of scoreable adults (Federal Reserve Bank of New York).

Reaching the max on any of these models requires a specific combination of factors that few files hold at the same time:

- A credit history longer than 15 years.

- Zero late payments on any account in the bureau's full reporting window.

- Credit utilization below 5% on every revolving account when the score is pulled.

- A healthy mix of revolving and installment credit, with several accounts older than 10 years.

- No new credit applications in the past 12 to 24 months.

Even one slightly elevated utilization month, one new account, or one card under three years old will keep an otherwise spotless file in the 820 to 840 range instead of touching the maximum.

What can you actually do with a top-tier score?

Above roughly 760, lenders stop differentiating. The same advertised rate goes to a 760 borrower as to an 850 borrower, on every major product. This is the most useful counter to the "I need 900" mindset: pushing past 760 captures no additional financial benefit on a mortgage, auto loan, credit card, or personal loan (CFPB).

Two narrow exceptions exist:

- Niche mortgage rate-sheet tiers. A small number of US lenders publish an extra 0.05% to 0.10% rate concession at 780+ or 800+. On a 30-year $500,000 mortgage that totals a few thousand dollars over the life of the loan, but the lenders offering it are not the major banks. Most rate sheets treat 760+ as a single best-rate tier.

- Premium credit-card approvals. Some invitation-only US cards (top-tier Amex products) reference an excellent credit file as a factor in underwriting. Income, banking relationship, and existing card history usually matter more than the precise score number, but a higher score raises the odds.

Outside those two cases, the financial reward of going from 800 to 850 (or, on FICO Auto Score, from 850 to 900) is essentially zero. If you want a fuller picture of how the maximum score is built and why it is rarely worth the effort to chase it, see what is the max credit score.

The myths that misallocate effort

A short list of beliefs that push people to optimize for the wrong number:

- "Carry a small balance to show activity." False. A $0 statement balance does not hurt your score. A reported balance increases your utilization ratio, which hurts it.

- "Closing old credit cards helps." False. Closing an old card reduces your average account age and your total available credit, which raises utilization and lowers the score.

- "FICO Auto Score is the score that matters." Only when you are applying for an auto loan. For every other product, base FICO or VantageScore is the relevant number.

- "Higher is always better." Above 760, the marginal score point earns nothing measurable on a typical lender's pricing sheet. The score is a signal, not the goal.

Reaching a perfect score is a long-tail achievement that requires near-perfect file management over more than a decade. For almost everyone, hitting the "excellent" band at 760+ and holding it is the practical maximum worth chasing. If your score sits well below that band, the moves that genuinely raise it are laid out in how to fix your credit score.

The number is one of several inputs lenders use, alongside income, debt-to-income ratio, employment stability, and product-specific underwriting. A higher score helps, but it is rarely the deciding factor once you cross into the excellent range.