How do you fix your credit score?

You fix your credit score by correcting what is dragging it down: dispute inaccurate negative items, bring any past-due accounts current, pay your credit card balances below 30% of their limits, and then keep every payment on time going forward. There is no secret product and no fee required. The Federal Trade Commission is direct about this: you can repair your credit yourself, for free (FTC).

The reason these specific moves work is that two factors do most of the scoring. In the FICO model, payment history (whether you pay on time) is 35% of your score and amounts owed (mostly how much of your credit limits you are using) is 30%. Length of history is 15%, new credit is 10%, and credit mix is 10% (myFICO). Fixing your score means improving the two factors that together control 65% of the number.

The core repair checklist, in priority order:

- Pull all three reports. Get your Equifax, Experian, and TransUnion reports free at AnnualCreditReport.com. This is the only federally authorized free source.

- Dispute inaccuracies. Wrong late payments, accounts that are not yours, or balances that are already paid can be removed.

- Bring past-due accounts current. A late account that you make current stops aging into worse delinquency.

- Cut utilization. Pay revolving balances down under 30%, and under 10% if you can.

- Keep old accounts open. Available credit and account age both help.

- Slow down on new applications. Each hard inquiry can shave a few points and signals risk in clusters.

It helps to know which actions move the number and which only feel productive. The table below sorts the common moves, drawing the "does not help" column directly from the CFPB's published list of actions that do not rebuild credit (CFPB).

| What actually helps | What does not help |

|---|---|

| Paying every bill on time | Using a debit card (it never reports to the bureaus) |

| Lowering credit card utilization | Loading a prepaid card |

| Disputing inaccurate negative items | Taking a payday loan |

| Keeping old, paid-off accounts open | Paying a company to "boost" your score |

| Adding a secured card or credit-builder loan | Closing cards to "clean up" your file |

What does fixing your credit look like for your situation?

The right first move depends on why your score is low, so start by reading your report to identify your situation, then act on the cause rather than running a generic checklist. A score of 540 caused by one missed payment needs a different fix than a 540 caused by three accounts in collections. Below are the four most common starting points and the highest-impact first step for each.

You have one isolated late payment

Ask the lender for a goodwill adjustment and make sure it never happens again. A single 30-day late payment on an otherwise clean file can cost a meaningful number of points, but it also recovers as it ages. If the lateness was a one-time slip on an account you have otherwise paid well, a written goodwill request asking the creditor to remove the mark sometimes succeeds. Set up autopay for at least the minimum so it cannot recur.

Your balances are high but your payments are on time

Pay your cards down before the statement closes, because the balance on the statement date is what gets reported. This is the fastest fix available. If you carry $4,000 across cards with a $5,000 total limit, your 80% utilization is heavily penalizing your score. Paying that down to $500 (10%) can lift the score within one to two billing cycles, because there is no waiting period: utilization is recalculated each month from fresh data.

You have accounts in collections or charged off

Verify the debt is yours and accurate before you pay, and get any pay-for-delete agreement in writing. Under the Fair Credit Reporting Act you can request validation of a collection account. Newer scoring models (FICO 9 and VantageScore 4.0) ignore paid collections and weigh medical collections less, so paying a legitimate collection can help under those models. Do not let a debt collector talk you into restarting the clock on a very old debt by making a partial payment, which can re-age it.

You have little or no recent credit history

Open a secured credit card or a credit-builder loan and let on-time payments build a record from zero. A secured card requires a refundable deposit, often a few hundred dollars, and reports like a normal card. A credit-builder loan, usually $1,000 or less, holds the money while you make payments and releases it at the end (CFPB). Both create the payment history a thin file is missing. If you are building credit from scratch, it helps to know what a credit score starts at so you can measure real progress against that baseline.

How fast can you fix your credit score?

Some things move in weeks and some only heal with time, so honest "fast" credit repair means pulling the levers that recalculate quickly while letting derogatory marks age out on their own schedule. Anyone promising to erase accurate negative information quickly is describing something that is not legal and does not work.

Here is a realistic timeline for a worked example. Imagine a borrower with a 580 score, a credit card at 75% utilization, and one 90-day-late payment from eight months ago:

- Within one to two billing cycles: paying the card from 75% down to under 10% utilization is the single biggest fast lever, because the bureaus rescore from the new statement balance with no delay.

- Within about 30 days: if any negative item on the report is inaccurate, the bureau must investigate and respond, typically within 30 days, and remove anything it cannot verify (CFPB).

- Over 6 to 24 months: the 90-day-late mark keeps fading as newer on-time payments accumulate, but it remains on the report until it ages off.

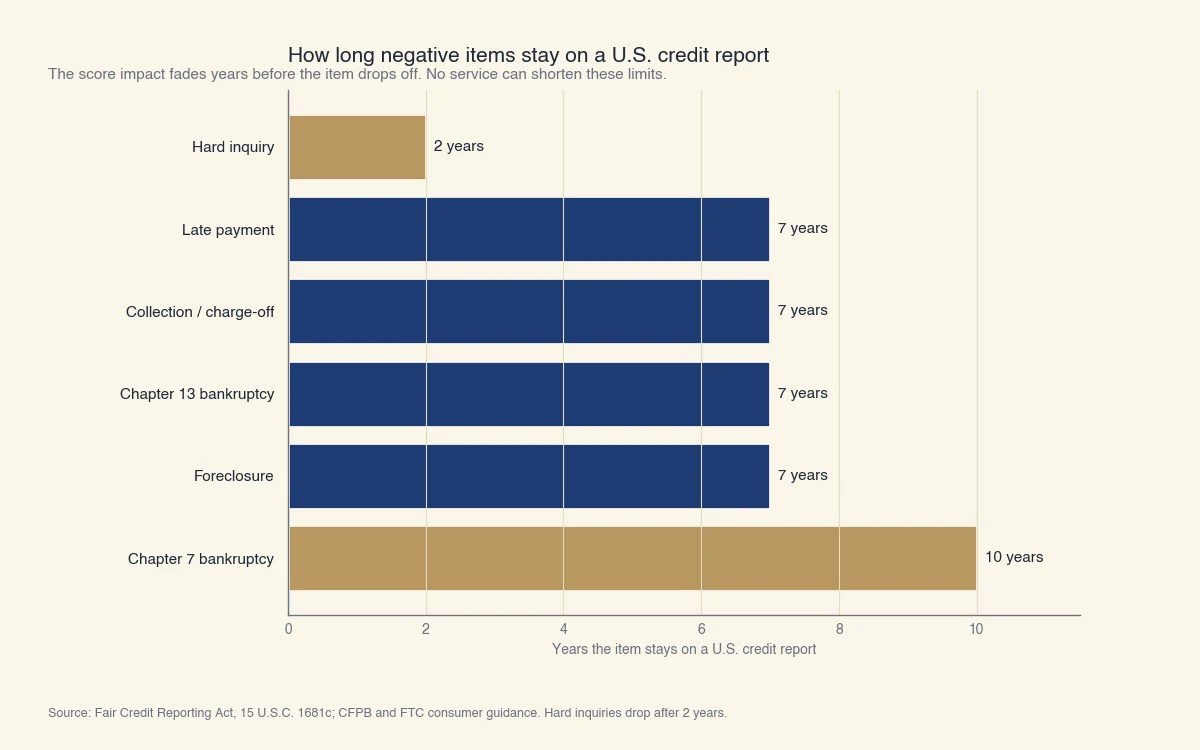

That last point is where most "how long to fix credit" questions actually land. Federal law sets fixed reporting limits, and no legitimate service can shorten them. The chart below shows how long common negative items stay on a U.S. credit report.

Source: Fair Credit Reporting Act, 15 U.S.C. § 1681c; CFPB and FTC consumer guidance.

The practical takeaway: a negative item's drag on your score shrinks long before the item disappears. A two-year-old late payment hurts far less than a fresh one, even though both sit on the report for seven years. Time plus consistent new positive history does most of the repair work that no shortcut can replace. If you are repairing credit with a target in mind, like a mortgage, it helps to know what credit score is good enough to buy a house so you can measure how far you still have to climb.

How do you dispute errors on your credit report?

You dispute an error by filing it with the credit bureau that shows it and, ideally, with the company that supplied the information, then the bureau must investigate within about 30 days and correct or delete anything it cannot verify. Errors are common enough that this is one of the first things to check: a single wrong late payment or a stranger's account on your file can suppress your score for no real reason.

The process:

- Get your report from AnnualCreditReport.com and read every account, balance, and status.

- Identify the specific error and gather proof: a paid receipt, a statement, a letter showing the account is not yours.

- File the dispute with the bureau (Equifax, Experian, or TransUnion) online, by mail, or by phone, and separately notify the furnisher.

- Wait for the result. The bureau generally has 30 days to investigate. If it agrees, the item is corrected or removed and your score updates.

Disputing does not cost anything and does not lower your score. If the item is verified as accurate, it stays, but you have lost nothing by checking.

Do you need to pay a credit repair company?

No. The FTC states plainly that a credit repair company cannot do anything for you that you cannot do yourself for free, and the Credit Repair Organizations Act makes it illegal for them to charge you before they deliver a service. If a company asks for payment up front, tells you to dispute accurate information, or offers to create a "new credit identity," those are warning signs of an unlawful operation (FTC).

Legitimate help does exist, and it is usually free or low cost. Nonprofit credit counseling agencies can review your full picture and set up a debt management plan; the CFPB and FTC both point consumers to accredited nonprofit counselors rather than for-profit repair firms (CFPB). The money you would spend on a repair company is almost always better used to pay down the balances that are lowering your score in the first place.

A fair score also matters because the score itself is only an estimate of risk. At Sphera Credit we build credit-decision technology that helps lenders look past a single number and assess a borrower's real ability to repay, so that an accurate, well-documented file gets a fair read. Fixing your report is the part you control, and an accurate report is what lets any honest evaluation work in your favor.