Does a balance transfer affect your credit rating?

Yes, a balance transfer can affect your credit score (also called your credit rating), usually as a small short-term dip followed by a larger long-term lift. Opening a new card for the transfer triggers a hard inquiry and lowers the average age of your accounts, which can cost a few points. In the months after, the new card's credit limit lowers your credit utilization, the share of your available credit you are using, and that improvement typically outweighs the early dip.

The key point most explanations skip: a balance transfer does not change how much you owe. It changes how that debt is spread across your available credit. You move the same dollars from one card to another, sometimes paying a fee to do it. Your score moves because that redistribution changes your utilization, your account ages, and the number of recent applications on your file, not because your debt got smaller.

A balance transfer is the act of moving an outstanding balance from one credit card to another, usually to a card offering a low or 0% introductory interest rate for a set period (CFPB). Whether it helps or hurts your score depends almost entirely on one choice: are you opening a new card, or just shuffling balances between cards you already have?

How a balance transfer moves each part of your credit score

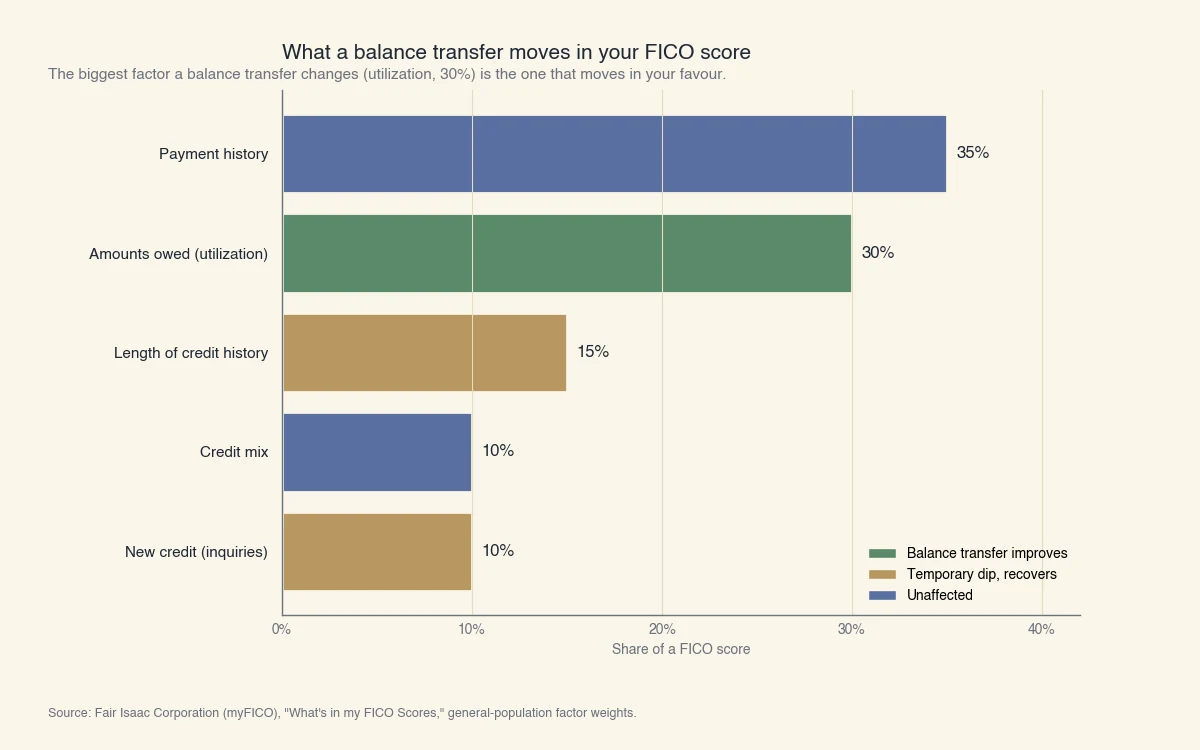

A balance transfer touches four of the five factors that build a FICO score, and the largest one it moves, credit utilization, is the one most likely to push your score up. FICO scores are built from five weighted factors (myFICO). The table below maps each factor to what a balance transfer does to it.

| FICO factor | Weight | What a balance transfer does | Direction |

|---|---|---|---|

| Payment history | 35% | Unchanged at transfer; consolidating to one payment can make on-time payments easier going forward | Neutral, then up |

| Amounts owed (utilization) | 30% | A new card adds available credit, lowering your overall utilization | Down (good for score) |

| Length of credit history | 15% | A new account lowers your average account age | Down (temporary) |

| Credit mix | 10% | No change; you still hold revolving credit | Neutral |

| New credit | 10% | The application adds one hard inquiry | Down (temporary) |

Source: Fair Isaac Corporation (myFICO), "What's in my FICO Scores," general-population factor weights.

The two factors that move down, length of history and new credit, are worth 15% and 10% and recover on their own. The factor that moves in your favor, amounts owed, is worth 30% and responds immediately. That asymmetry is why a single, well-managed balance transfer tends to be net positive for a score over a few months.

Why utilization carries the most weight here

Credit utilization is your reported balances divided by your total credit limits, and lenders read a low number as a sign you are not stretched. The CFPB suggests keeping your utilization below 30% (CFPB). Scoring models look at utilization two ways: per card and in aggregate. A new balance-transfer card raises your total limit, which lowers your aggregate utilization the moment the new limit is reported, even before you pay down a dollar of principal.

Why the hard inquiry is small

A hard inquiry happens when a lender checks your credit to decide on an application, and one inquiry usually costs a FICO score less than five points (CFPB). The inquiry stays on your report for two years but only affects your score for about a year. Checking your own score to compare balance-transfer offers is a soft inquiry and has no effect at all. The same hard-inquiry and new-account mechanics drive other financing decisions too: whether applying for a credit card affects your rating and whether Affirm affects your credit score come down to the same handful of factors.

A worked example: what a balance transfer does to your utilization and your wallet

On realistic numbers, a single balance transfer can cut your utilization from the high-risk zone into the safe zone while costing a fee that the interest savings repay many times over. Consider Maria, who carries debt on three cards.

| Card | Balance | Limit | Per-card utilization |

|---|---|---|---|

| Card A | $2,400 | $3,000 | 80% |

| Card B | $2,800 | $4,000 | 70% |

| Card C | $1,200 | $3,000 | 40% |

| Before: total | $6,400 | $10,000 | 64% |

Maria opens a new balance-transfer card with an $8,000 limit and a 0% rate for 15 months, and moves all $6,400 onto it. Here is the after-state.

| Measure | Before | After |

|---|---|---|

| Total balance owed | $6,400 | $6,400 |

| Total credit limit | $10,000 | $18,000 |

| Overall utilization | 64% | 36% |

Her debt did not shrink, but her overall utilization fell from 64% to 36%, because her total limit rose from $10,000 to $18,000. If she keeps the three old cards open, her utilization keeps falling as she pays the principal down.

The fee math: a typical balance-transfer fee is 3% to 5% of the amount moved (CFPB). At 3%, moving $6,400 costs $192. If that $6,400 was previously sitting at a 22% annual rate, it was costing roughly $1,400 in interest over a year. Paying $192 once to stop a $1,400-a-year interest clock for 15 months is the trade that makes a balance transfer worth it, as long as Maria pays the balance off before the 0% window ends.

After the introductory period, the rate on the new card can rise, so the savings only hold if the debt is gone by then (CFPB).

When a balance transfer helps your score and when it hurts

A balance transfer helps when you open one new card and pay the debt down, and it hurts when you either close old cards or keep opening new ones. The same action produces opposite results depending on how you handle the accounts around it. Three common patterns:

- Helps: You open one new card, move balances to it, keep your old cards open with low or zero balances, and pay the principal down within the intro window. Utilization drops, the inquiry fades, and your score climbs.

- Neutral: You move balances only among cards you already hold. No new inquiry, no change to your total limit, so your aggregate utilization and your score barely move.

- Hurts: You open several balance-transfer cards over a short period, or you close the old cards right after transferring. Multiple inquiries stack up, your average account age falls, and closing cards can spike your utilization.

How it plays out for different borrowers

The transfer behaves differently depending on where you start:

- Near-maxed borrower: If your cards sit above 70% utilization, a new card's added limit gives you the biggest utilization drop, so the upside is largest for you, provided you qualify.

- Thin-file borrower: If you only have one or two accounts, opening a new card has a sharper effect on your average account age, so the temporary dip is more noticeable. It still usually recovers.

- Prime optimizer: If your score is already high and your utilization already low, the upside is smaller and the inquiry is the more visible effect. A transfer here is about saving interest, not lifting a score that is already strong.

What to do after a balance transfer to protect your score

The single most important move after a balance transfer is to keep your old cards open and pay the transferred balance down before the introductory rate expires. What you do in the weeks after the transfer decides whether the score effect is positive or negative.

- Keep the old cards open. Closing them removes their limits from your utilization math and can raise your overall utilization overnight. Leave them open, even at a zero balance.

- Do not run the old cards back up. Freeing up the old cards and then re-spending on them rebuilds the same debt at a higher rate, and doubles your total balances.

- Pay down the principal during the 0% window. The introductory rate is a window to attack the principal, not a reason to relax. Divide the balance by the number of intro months and aim to clear it before the rate resets.

- Avoid new applications for a while. Stacking more inquiries on top of the transfer is what turns a small, temporary dip into a real one.

One persistent myth is worth correcting: you do not need to carry a balance to build credit. Scoring models do not reward leaving debt on a card, and the CFPB lists "you need to carry a balance" among the credit-score myths that hold people back (CFPB). Paying the transferred balance to zero is best for both your score and your wallet. Lowering your utilization this way is one lever among several, so for the full sequence see how to fix your credit score.