Is a FICO score the same as a credit score?

No. Every FICO score is a credit score, but not every credit score is a FICO score. "Credit score" is the umbrella term for any three-digit number that statistical models calculate from your credit report. FICO is one brand of credit score, made by Fair Isaac Corporation. VantageScore is the main alternative. Each credit bureau also publishes proprietary internal scores (CFPB).

The practical consequence is the most counterintuitive part of US consumer credit: the credit score you check on your phone is almost certainly not the credit score your lender will pull. Both are real, both are accurate, both are called "credit scores." They just come from different models, different bureau data files, and different refresh dates.

This page explains exactly which score your lender will see for the decision you care about, why the free score on your phone usually reads higher, and how to check the right score before you apply.

What is a FICO score, and what is a credit score?

A credit score is any algorithmically generated three-digit number a lender can use to estimate the probability that you will repay a debt. A FICO score is the specific brand of credit score made by Fair Isaac Corporation since 1989. Fair Isaac was the first company to standardize statistical credit scoring across all three US bureaus, and by the mid-1990s Fannie Mae and Freddie Mac had adopted FICO for conforming mortgage underwriting (myFICO). That early-mover position is why "FICO" became a near-synonym for "credit score" in everyday usage, the same way "Kleenex" stands in for "tissue."

Today there are three meaningful families of credit scores in the US:

- FICO (Fair Isaac): base scores FICO 8, FICO 9, FICO 10, FICO 10 T. Industry-specific variants FICO Auto Score, FICO Bankcard Score, FICO Mortgage Score. Used in roughly 90% of US lending decisions according to Fair Isaac's own market data (myFICO).

- VantageScore (joint venture of Equifax, Experian, TransUnion): VantageScore 3.0 is the model behind most free consumer apps (Credit Karma, NerdWallet). VantageScore 4.0 is the current latest version.

- Bureau internal scores: each bureau also publishes its own proprietary scores (Experian National Equivalency Score, TransUnion CreditVision, Equifax Risk Score). Most consumers never see these; they are sold to specific lenders for specific product lines.

The five factors every model uses are roughly the same (payment history, amounts owed, length of history, credit mix, new credit), but the weightings differ. FICO 8 weights payment history at 35% and amounts owed at 30%; VantageScore 4.0 weights payment history at 40% and shifts the rest of the weights (VantageScore). On the same credit file the two models often produce scores 10 to 30 points apart, and sometimes more.

Why "is FICO the same as credit score" is a real question

The terms get confused because the consumer-facing world has standardized on the word "score" without specifying which model. A credit card issuer might say "your FICO 8 score is 720." A free app might say "your credit score is 745." A mortgage broker might say "your credit score is 692." All three statements can be true at the same time, for the same person, on the same day. They are measuring overlapping but non-identical things.

The single best mental model: the word "credit score" is like the word "temperature." It only tells you the genre of the measurement. To compare numbers, you also need to know which thermometer (which model) and which weather station (which bureau).

Which FICO version does your lender actually pull?

Different lender products pull different FICO versions. The version determines the score's number scale, the formula weights, and which kinds of behaviour move the score most. Here is the version most US lender products actually pull when you apply.

| Product | Score model the lender uses | Range | Source / authority |

|---|---|---|---|

| Conforming mortgage (Fannie Mae / Freddie Mac) | FICO Score 2 (Experian), FICO Score 4 (TransUnion), FICO Score 5 (Equifax) | 300-850 | Fannie Mae Selling Guide B3-5.1-01 |

| FHA / VA / USDA mortgage | Same FICO 2 / 4 / 5 trio | 300-850 | HUD, VA, USDA program handbooks |

| Auto loan | FICO Auto Score 8 or FICO Auto Score 9 | 250-900 | myFICO |

| Credit card (new account) | FICO Bankcard Score 8 or FICO Bankcard Score 9, or FICO 8 base | 250-900 (industry) or 300-850 (base) | myFICO |

| Personal loan / unsecured installment | FICO 8 or FICO 9 base | 300-850 | myFICO |

| Free score on Credit Karma | VantageScore 3.0 (Equifax + TransUnion) | 300-850 | Credit Karma |

| Free FICO on a credit card statement | FICO 8 (usually Experian or TransUnion data) | 300-850 | Issuer disclosure |

A few things to notice in that table:

- Conforming mortgages still use the classic FICO trio (2 / 4 / 5), which Fair Isaac shipped in the late 1990s. FHFA approved FICO 10 T and VantageScore 4.0 in October 2022 for eventual use, but as of 2026 the GSE transition is still in implementation phases (FHFA). If you are applying for a mortgage today, the version that decides your rate is still the 25-year-old FICO 2 / 4 / 5 family.

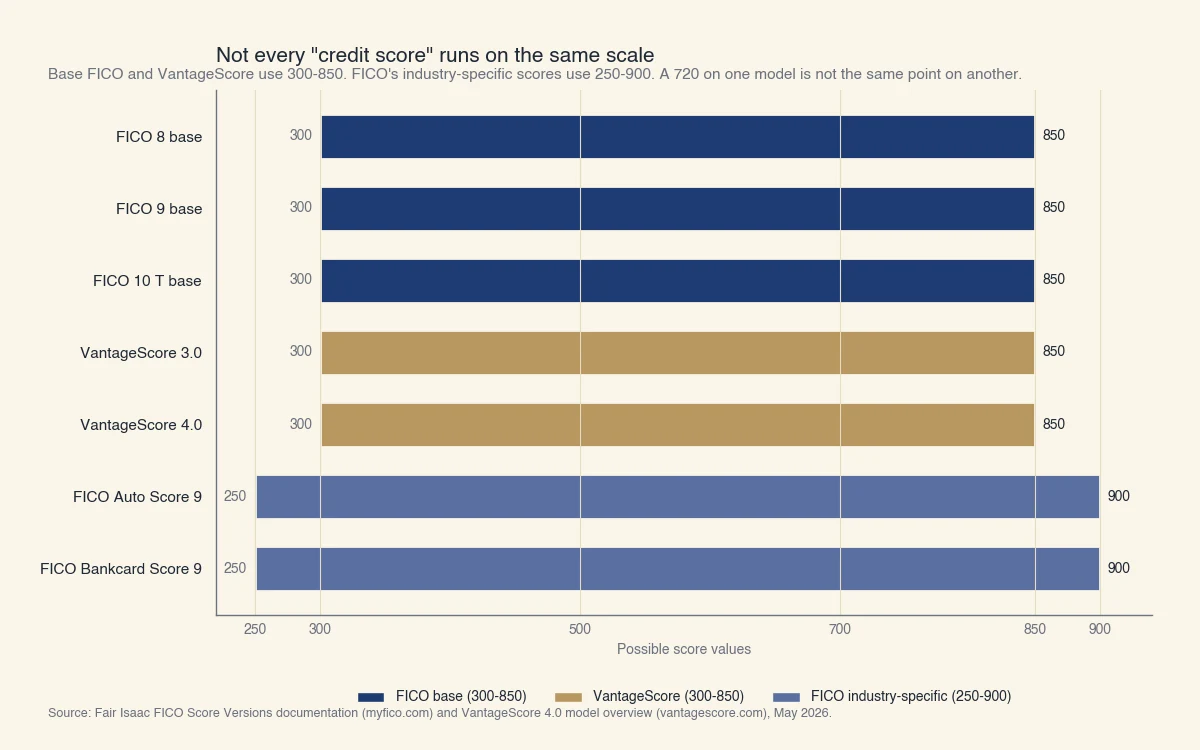

- Industry-specific FICO scores use a 250-900 range, not 300-850. A FICO Auto Score 8 of 850 is roughly equivalent to a FICO 8 base score of about 770, so 850 is only the highest credit score you can have on the base 300-850 models. The numbers are not interchangeable without translation.

- The free score on Credit Karma is a real VantageScore 3.0, not a FICO score. It is informative for tracking trends in your file, but it is not the number your auto or mortgage lender will see.

Source: Fair Isaac FICO Score Versions documentation and VantageScore 4.0 model overview, May 2026.

How to find out which model your lender uses

Three options, ranked by ease:

- Read the application disclosure. Federal Reserve Regulation B requires lenders to disclose the credit score they used in the adverse-action notice if you are declined or repriced. The disclosure names the model (for example "FICO Score 8" or "VantageScore 3.0") and the bureau.

- Ask the loan officer directly. Mortgage lenders, auto dealers, and credit unions will tell you which version they pull. They are not allowed to share the score before the inquiry, but the model name is not confidential.

- Use myFICO's product page. Fair Isaac publishes a free chart of which lender categories typically use which FICO version. The categories match the table above and are updated when the GSEs change policy.

Why your free score does not match the lender's score

The credit score on your phone almost always reads different from the one your lender pulls because the model is different, the bureau data source is different, and the refresh date is different. Each of those three things can move the number by 10 to 30 points on a typical thick-file consumer.

Here is a worked example using a hypothetical consumer named Sarah.

Sarah opens Credit Karma. It shows a 720. She applies for a 30-year fixed mortgage. The lender's loan officer comes back and says her qualifying score is 695, which bumps her into a higher mortgage-rate tier. Why the 25-point gap?

| Layer | Sarah's free score | Sarah's mortgage score | Gap contribution |

|---|---|---|---|

| Model | VantageScore 3.0 | FICO Score 2 (Experian) | ~15 points |

| Bureau data file | TransUnion (Credit Karma's default) | Experian | ~5 points |

| Refresh date | Last Tuesday's snapshot | Pulled fresh today, includes a credit-card balance posted Friday | ~5 points |

| Total | 720 | 695 | 25 points |

None of these gaps mean either score is wrong. They mean the two numbers are answering slightly different questions:

- VantageScore 3.0 vs FICO Score 2 (the model gap). VantageScore 3.0 penalizes recent credit-card balance growth more aggressively than FICO Score 2 does, but VantageScore 3.0 is more forgiving on thin-file consumers. On a thick-file consumer with a recent balance increase, FICO 2 will usually read 10 to 20 points lower than VantageScore 3.0.

- TransUnion vs Experian (the bureau gap). Different bureaus receive different tradeline reports. A creditor that only reports to Experian (some credit unions, some niche lenders) will appear in the Experian-derived score but not the TransUnion-derived one. The CFPB estimates that around 80% of consumers see their FICO scores agree across bureaus within 20 points, but the remaining 20% see meaningful divergence (CFPB analysis).

- Refresh date (the timing gap). Most free apps refresh on a weekly cadence. A lender pulls a hard inquiry on the live bureau file, which includes everything reported up to that day. A credit-card balance that hit the bureau on Friday is on the lender's score but not yet on Tuesday's free-app snapshot.

The CFPB studied this exact mismatch in 2012 and found that for roughly 19% of consumers, the score they buy from a bureau-direct product differs from the score lenders use by more than 50 points (CFPB Analysis of Differences between Consumer- and Creditor-Purchased Credit Scores). The 2012 study used older FICO and bureau-direct products, but the structural reason for the gap (different models, different bureau data, different refresh) has not changed.

What to do about the gap

If you are within a few months of a major credit application, pull the right score before you apply. The cheapest path:

- For a mortgage: subscribe to myFICO 1-Bureau or 3-Bureau for one month. It is the only consumer product that shows FICO Score 2, 4, and 5 simultaneously. Cancel after the application closes.

- For an auto loan: check FICO Auto Score 8 on myFICO, or ask the dealership F&I manager which model and bureau they will pull.

- For a credit card: the free FICO 8 score on your existing credit card statement is usually within a few points of what a new issuer will see.

Knowing the right number in advance does not change the application decision. It does let you decide whether to apply now or to pay down a balance for a billing cycle first, and it removes the surprise of seeing a different number on the loan estimate. If high card balances are what hold the number down, weigh how a balance transfer affects your credit rating before you apply, since shifting balances changes the utilization every one of these models reads.

How the model landscape is changing

FHFA approved FICO 10 T and VantageScore 4.0 in October 2022 for use in conforming mortgage underwriting, with a multi-year implementation timeline. The transition began with the GSEs publishing acceptance criteria, then moves to phased lender adoption, and ends with the classic FICO 2 / 4 / 5 family being retired for new originations (FHFA).

The two new models are meaningfully different from the classic FICO trio:

- FICO 10 T is the first FICO model to use "trended data," meaning it looks at 24 months of balance history per account rather than only the current month's snapshot. A consumer who carries a $5,000 balance for two years scores lower under FICO 10 T than under FICO 2, even if both end-of-month balances are identical.

- VantageScore 4.0 uses machine-learning-derived weights and includes rent and utility payments where the data is reported. It treats medical collections under $500 as zero-impact, matching the bureaus' 2022 medical-debt reporting policy change.

Mortgage applicants in 2026 are still seeing classic FICO 2 / 4 / 5 in their underwriting in most cases. By the end of the GSE transition (currently targeted for the late 2020s), the same applicants will see FICO 10 T and VantageScore 4.0 on a bi-merge credit report. The transition will move some borrowers' qualifying scores up and others down; the FHFA validation testing is what determined that the new models predict default at least as accurately as the old ones.

For a more general overview of credit scoring, see our learn page on what is a good credit score or what is the max credit score.