What does your credit score start at?

Your credit score does not start at any particular number. Before you have a reported credit history, you do not have a score at all, which is different from having a low score. Once you have one, your first FICO Score lands somewhere between 660 and 720 if you have managed one clean account for six months, and the Experian-reported 2025 average for the 18-28 age band is 678 (Experian).

That gap, between "no score" and "low score", is the source of almost every misconception about starting credit. The most common myth is that scores start at zero and climb up. They do not. A credit score is a statistical estimate of your probability of repaying credit, calculated from your credit-bureau file. If your file is empty, the model has nothing to estimate from, so the bureau returns "no score available" instead of a number. There is no zero, no 100, and no 300 starting line.

A few specifics that matter before any of the practical advice:

- The FICO and VantageScore scales both run from 300 to 850. That is the full range, top and bottom. A real score below 500 is rare and usually reflects active delinquencies, charge-offs, or recent bankruptcy. A first score after six months of clean behaviour does not land at 300.

- "Credit invisible" is the official name for an adult whose credit-bureau file is empty. The Consumer Financial Protection Bureau estimates that 26 million US adults are credit-invisible (CFPB). You are not credit-invisible because of bad behaviour; you are credit-invisible because nothing has ever been reported about you.

- FICO and VantageScore have different rules for when a score can exist. FICO requires a credit account at least six months old with reported activity in the last six months. VantageScore can produce a score as soon as any tradeline appears, sometimes within one or two months (Experian).

Why isn't there a single "starting" number?

Because the score is the output of a statistical model, not a counter. The model needs data to produce a number. With no data, no number; with six months of clean payment history on a single card, a first FICO score in the high 600s; with a parent's perfect ten-year-old card as an authorized-user tradeline, a first FICO score in the high 700s on the same day. Every starting score is a function of the data the bureaus already have, not of a fixed initial value.

When do you actually get your first credit score?

You get your first FICO score about six months after your first credit account opens and starts reporting; you can get your first VantageScore as quickly as one to two months after the same event. Most US lenders pull FICO, so for the question "when am I scored for an application," the practical answer is six months (Experian).

The two scoring models' eligibility rules side by side:

| Rule | FICO Score 8 / 9 | VantageScore 4.0 |

|---|---|---|

| Minimum account age | 6 months on at least one tradeline | 1 month |

| Recent activity requirement | Activity reported within last 6 months | Any tradeline ever reported |

| Authorized-user tradelines counted | Yes (FICO 8 fully; FICO 9 with mild adjustments) | Yes |

| Common first-score range with clean behaviour | 660-720 | 620-700 |

| Used by most US lenders | Yes (FICO 8 and 9 dominate) | Less commonly used at application |

The FICO/VantageScore difference is why someone who checks a free credit-score app one month after opening a secured card sees a VantageScore around 650 and then sees their lender pull "no score" when they apply for a car loan two months later. The bank app is showing VantageScore; the lender is pulling FICO; and FICO is not ready to compute yet.

What if I open more than one account at once?

Opening two accounts at the same time does not speed up FICO eligibility, which is gated by the age of your oldest account. It does add data, which can produce a more stable first score once eligibility is reached. The trade-off is that two new hard inquiries and two new accounts will both register as risk factors in the first FICO score that is finally computed, so the score may come in slightly lower than if you had opened just one. Most US credit-building guides recommend one account first, then a second after 12 months (CFPB).

What does a real first credit score look like?

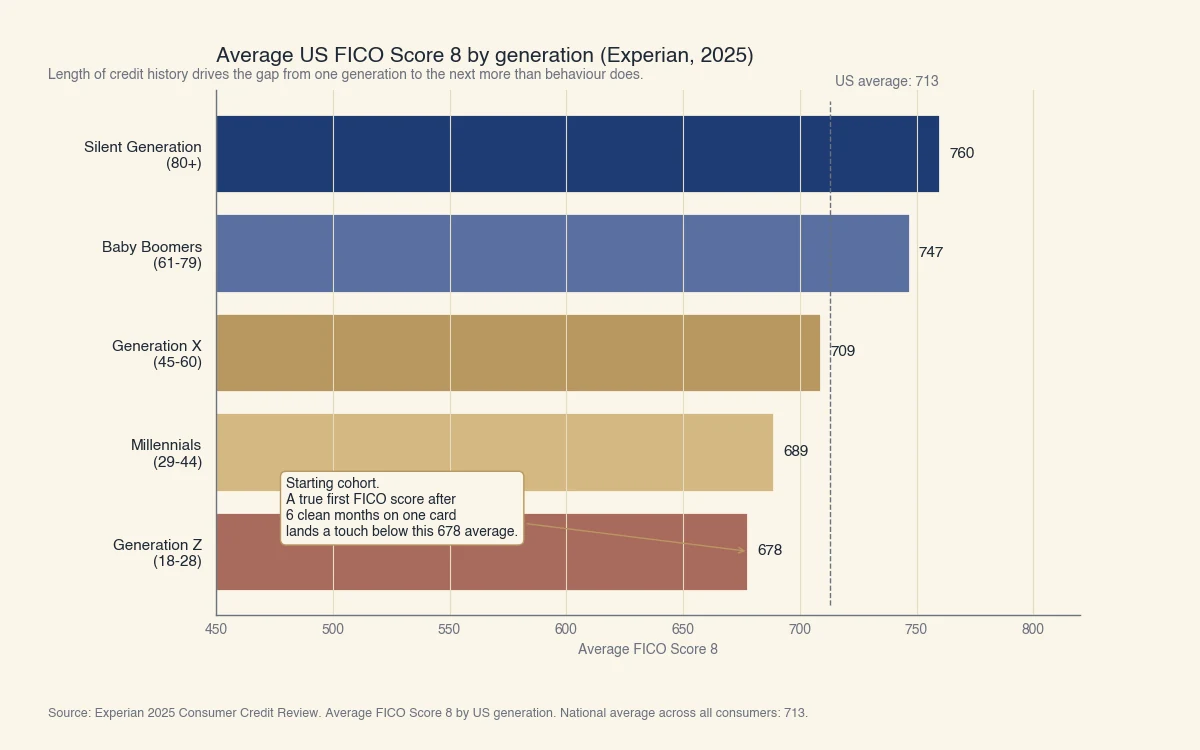

Experian's 2025 Consumer Credit Review reports the average FICO Score 8 for Generation Z (ages 18-28) at 678; that is the closest published benchmark for what a recently-started credit profile looks like in the United States. The full cross-generational picture climbs steadily with age, reflecting the way time and clean repayment accumulate in the score (Experian).

Source: Experian 2025 Consumer Credit Review. Generations defined by Experian: Gen Z (18-28), Millennials (29-44), Gen X (45-60), Baby Boomers (61-79), Silent Generation (80+). US national average across all consumers: 713.

A few calibrations on these numbers:

- Gen Z's 678 is the cohort average, not a true first score. It reflects people who already have one to ten years of credit history. A first score computed at the six-month FICO threshold, on a single clean account, lands lower than the cohort average, typically 660-700.

- The 35-point gap between Gen Z (678) and the national average (713) reflects history length more than behaviour. Length of credit history is 15% of the FICO formula, and Gen Z almost universally has less of it.

- Boomers and the Silent Generation average above 740 because they have decades of clean history compounding inside the model. This is the strongest single argument for opening a first account early; even a single clean card opened at age 18 and kept open through age 28 contributes 10 years of "length of history" by your late twenties.

How does your score actually build, month by month?

A practical timeline from credit-invisible to a first FICO score, using a single secured credit card and clean behaviour, runs about six months to the first FICO number and 12 months to a "good"-band 670+ score. The month-by-month detail varies, but the broad shape is consistent (Experian).

A realistic worked example for someone we will call Sarah, age 18, with no prior credit:

- Month 0. Sarah opens her first secured credit card with a major issuer. The card is reported to all three bureaus by Month 1. She is still credit-invisible at this moment; the bureau file exists but has no scoreable data.

- Months 1-2. The card appears as an open tradeline at all three bureaus. FICO returns "no score" because the account is under six months old. VantageScore can now produce a score, typically in the 600-650 range for a single clean card with low utilization.

- Months 3-5. Sarah pays in full each month and keeps utilization under 10%. Her VantageScore climbs into the 660-700 range. FICO still returns "no score."

- Month 6. Sarah's account hits the six-month FICO eligibility threshold. FICO returns its first score, typically 660-720 for one clean tradeline with on-time payment history and low utilization. This is the number lenders see.

- Month 9. Sarah adds a small credit-mix element by taking out a $500 credit-builder loan from a credit union. Her FICO climbs slightly because credit mix is now non-trivial.

- Month 12. Sarah's FICO is typically in the 700-730 range, inside the "good" band. She is now eligible for most prime unsecured cards, an upgrade from secured, and her credit-utilization patterns are visible across a full year.

Two scenarios that change this timeline:

- If Sarah's parent had added her as an authorized user on a 10-year-old, clean, low-utilization card at Month 0, her first FICO score at Month 6 (or possibly earlier, since the authorized-user tradeline carries the age) could be 720-770 instead of 660-720. Same Sarah, same behaviour, +50 to +100 points on the first computed score from the inherited tradeline.

- If Sarah misses one payment by 30+ days at Month 4, her Month 6 first FICO score lands 60-110 points lower, often in the high 500s. A single 30-day late hits a thin file disproportionately because payment history is 35% of the model and there is no other history to cushion the impact.

What is the authorized-user shortcut?

Adding a young adult as an authorized user on a parent's well-managed credit-card account inherits that tradeline's age, payment history, and utilization into the young adult's FICO score, often producing a first score 50 to 150 points higher than an organic six-month build. FICO Score 8 fully scores authorized-user tradelines for non-spouse adults; FICO Score 9 applies a mild discount but still counts them (myFICO).

The mechanism, in plain terms:

- The parent (the primary cardholder) adds the young adult as an authorized user. The young adult gets a card in their name but the parent remains legally responsible for the balance.

- The card issuer reports the full tradeline (open date, credit limit, balance, payment history) to the bureaus under both the parent's and the authorized user's profile.

- When FICO eventually computes a score for the authorized user, it treats that tradeline as if it were the young adult's own account, including its full age and clean payment history.

- The first computed FICO score reflects the inherited account's strength, often jumping 50-150 points above what an organic six-month build would produce.

Prerequisites for the shortcut to actually work:

- The primary cardholder's account must be at least six months old, ideally several years old. The longer the history, the larger the inherited "length of credit history" benefit.

- The account must have no late payments. FICO weights payment history at 35%, so a single 30-day late on the tradeline applies to the authorized user as well.

- Utilization must stay low, ideally under 30% and preferably under 10%. High utilization on the parent's card reduces the boost.

- The card issuer must report authorized users to the bureaus. Most major US issuers do (Chase, American Express, Discover, Citi, Capital One); a few smaller issuers do not.

Things to know before relying on this:

- The primary cardholder remains responsible for all charges. The authorized user is not legally on the hook for the debt, but if they use the card and do not reimburse the cardholder, the relationship can fracture and the cardholder will pay.

- The primary cardholder can remove the authorized user at any time. When this happens, the inherited tradeline typically falls off the authorized user's report, and the score can drop sharply.

- "Tradeline rental" services that charge to add unrelated users to strangers' accounts are not the same thing. The legitimate pattern is parent-adds-child or close-family, where the relationship is real and the cardholder retains control. The CFPB has explicitly warned against paid tradeline services.

What do you do if you have no credit score yet?

The fastest legitimate paths to a first credit score are: authorized-user tradeline from a family member, secured credit card with a major issuer, student credit card if you are in college, or credit-builder loan from a credit union. The four options differ in starting-score impact and in how quickly they let you graduate to standard unsecured credit (CFPB).

The practical comparison:

| Option | Typical first FICO score (after 6 months) | Time to mainstream unsecured card | What you need to start |

|---|---|---|---|

| Authorized user on a parent's clean aged card | 700-770 | Often eligible immediately at Month 6 | A willing primary cardholder with a clean aged account |

| Secured credit card (major issuer) | 660-720 | 12-18 months of clean use | $200-$500 cash deposit, government ID, US address |

| Student credit card | 660-710 | 12-18 months of clean use | Proof of enrollment, US address, sometimes a co-signer |

| Credit-builder loan (credit union) | 640-700 | 12-24 months; usually need a card alongside | Credit-union membership, $500-$1,000 loan amount |

A few notes on combining these:

- The authorized-user + secured-card combination is the most common high-end starting setup. The authorized-user tradeline carries the bulk of the early score; the secured card builds your own primary tradeline so that when the authorized-user relationship eventually ends, your score still has a foundation.

- The secured-card-only path is the most common stand-alone setup for adults without family support. Six months of clean utilization typically produces a 660-720 first FICO score; 12-18 months of clean utilization typically clears the issuer's threshold for an upgrade to an unsecured card.

- Avoid opening too many accounts in the first 12 months. Two new accounts plus two new hard inquiries on a thin file produces a worse first score than one new account, even though it adds more data.

For where the starting score fits on the broader scale, see what is a good credit score and what is the max credit score. For the day-to-day mechanics of moving your number up once you have one, see how to boost your credit score. If you already have a score and want to confirm where you stand, see how to check your credit score.