What is a good credit score to buy a house?

A good credit score to buy a house is 740 or higher, because that is the level at which most lenders give you their best mortgage rate. You can be approved for a mortgage with a much lower score, but the question hiding inside "what is a good score" is really two questions: the score that gets you approved, and the score that gets you priced well. They are different numbers, and the gap between them is worth tens of thousands of dollars.

Lenders read your FICO score, a three-digit number from 300 to 850 that estimates how likely you are to repay debt on time. For home buying, the standard bands look like this:

| FICO range | Label | What it means for a mortgage |

|---|---|---|

| 800 - 850 | Exceptional | Best available rate; smoothest approval |

| 740 - 799 | Very good | Best-price tier at most lenders |

| 670 - 739 | Good | Qualifies easily; rate is solid but not the floor |

| 580 - 669 | Fair | Qualifies via FHA or with overlays; higher rate |

| 300 - 579 | Poor | Limited options; large down payment or repair first |

So "good" in the everyday sense (670+) is enough to qualify comfortably, but "good" in the sense of good pricing starts at 740. Most approved buyers are already there: the median score on newly originated US mortgages was around 772 in early 2025 (Federal Reserve Bank of New York).

What score do you need just to qualify?

The minimum score to qualify is far below the score that earns a good rate, and it depends on the loan program. The common floors:

- Conventional loan: historically about 620. Fannie Mae removed its hard 620 minimum middle-score rule on November 16, 2025 in favor of a more complete risk assessment, but most lenders still apply their own 620 overlay (Fannie Mae).

- FHA loan: 580 with a 3.5% down payment, or as low as 500 with 10% down (HUD).

- VA and USDA loans: no government minimum; lenders typically want 620 to 640.

- Jumbo loan: usually 700 or higher because the loan exceeds conforming limits.

If your only question is whether you can get in the door, our companion page on the credit score needed to buy a house breaks down each program. The rest of this page is about the more expensive question: what score gets you a good deal, not just a yes.

Why the jump from 680 to 740 saves more than 620 to 680

Mortgage pricing does not rise smoothly as your score falls; it steps down at fixed breakpoints, so a few points in the right place can change your rate while a bigger move elsewhere does nothing. This is the part almost no buyer is told.

Fannie Mae and Freddie Mac, which buy most US mortgages, charge lenders a Loan-Level Price Adjustment (LLPA), a risk fee set by your credit score and down payment. The fee is read off a grid with discrete credit-score rows (Fannie Mae LLPA Matrix):

| LLPA credit-score row | Position |

|---|---|

| 780+ | Lowest fee |

| 760 - 779 | |

| 740 - 759 | Best-price threshold |

| 720 - 739 | |

| 700 - 719 | |

| 680 - 699 | |

| 660 - 679 | |

| 640 - 659 | |

| Below 640 | Highest fee |

Because the fee only changes when you cross a row boundary, the value of one extra point depends entirely on where you sit. Going from 695 to 700 crosses a boundary and can lower your fee. Going from 700 to 719 stays in the same row and changes nothing. That is why the move from 680 to 740 (crossing three boundaries) usually saves more than the move from 620 to 680, even though both are 60-point jumps.

The practical takeaway: do not chase a perfect 800. Find the next breakpoint above your current score and aim for that. A buyer at 735 has the single highest-value five points in the whole system, because 740 unlocks the best-price tier.

How much does a lower credit score cost you?

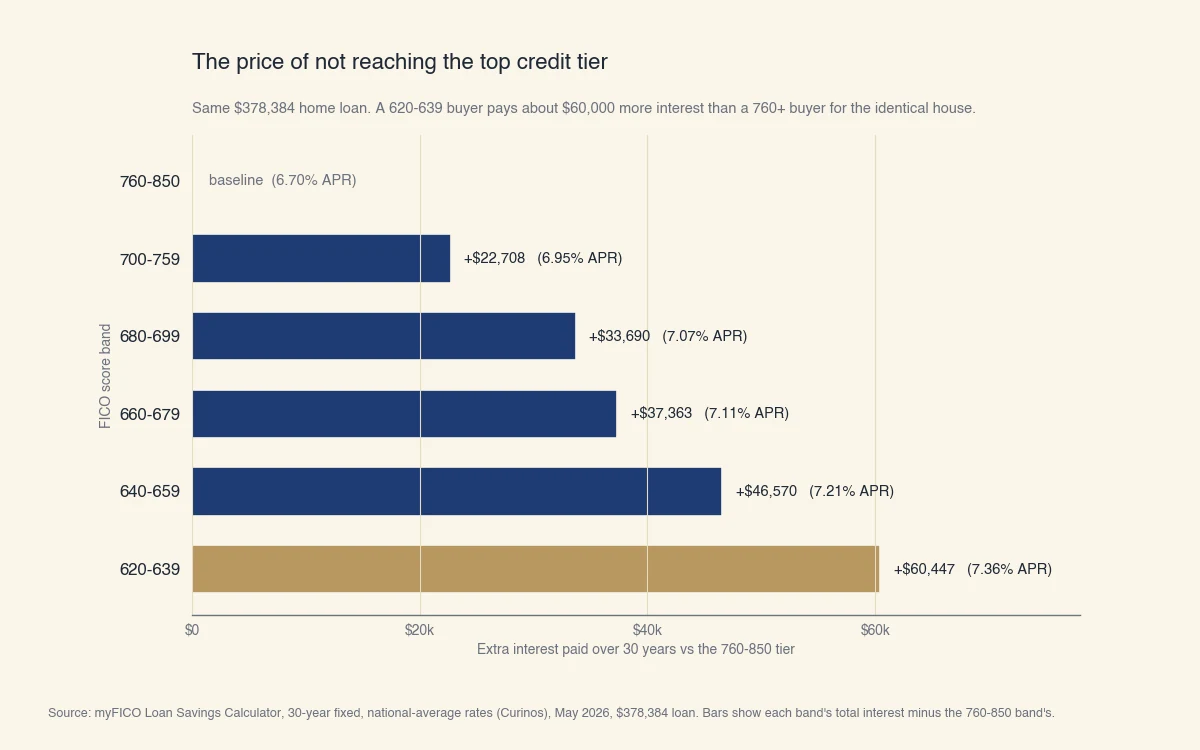

On a typical home loan, the difference between the top credit tier and the bottom qualifying tier is about $60,000 in interest over 30 years, for the exact same house. The score does not change the price of the home; it changes the price of the money.

Here is the cost laid out across the FICO bands on a $378,384 loan (the average US loan size in spring 2026), using national-average rates from the myFICO Loan Savings Calculator:

| FICO band | APR | Monthly payment | Total interest (30 yr) | Extra vs 760+ |

|---|---|---|---|---|

| 760 - 850 | 6.70% | $2,442 | $500,602 | baseline |

| 700 - 759 | 6.95% | $2,505 | $523,310 | +$22,708 |

| 680 - 699 | 7.07% | $2,535 | $534,292 | +$33,690 |

| 660 - 679 | 7.11% | $2,545 | $537,965 | +$37,363 |

| 640 - 659 | 7.21% | $2,571 | $547,172 | +$46,570 |

| 620 - 639 | 7.36% | $2,610 | $561,049 | +$60,447 |

The chart below shows the same numbers as the extra interest each band pays compared with a 760+ buyer.

Source: myFICO Loan Savings Calculator, 30-year fixed, national-average rates (Curinos), May 2026, $378,384 loan.

Is it worth waiting to improve your score?

Waiting a few months to cross a pricing tier is usually worth it; waiting to reach an already-excellent score is not. Run the comparison on your own numbers. If you are at 695 and three months of paying down a card lifts you past 700, the table above shows roughly an $11,000 swing in lifetime interest, which dwarfs three months of rent in most markets. Fair Isaac's own analysis shows reaching a 760 score can save a borrower between about $9,500 and $46,000 over the loan, depending on state and loan size (myFICO).

But if you are already at 760, pushing to 800 changes your rate by little or nothing, and home prices or rates can move against you while you wait. The math favors patience only when a clear breakpoint is within reach.

What's a good score for your situation?

The score that counts as "good" shifts with your borrower profile, because lenders lean on it differently depending on how the rest of your file looks. Every competitor page treats the buyer as a single salaried borrower, but the real answer depends on who you are.

First-time vs repeat buyers

A first-time buyer with no mortgage history is judged almost entirely on the credit score, down payment, and income. A repeat buyer often carries an existing mortgage, so the score interacts with debt-to-income ratio (your monthly debt payments divided by gross monthly income) and current obligations. If you are a repeat buyer, a good score still helps, but a lender will also weigh whether you are carrying two mortgages during the transition.

Self-employed, gig, and 1099 buyers

If your income is harder to document, your credit score does more work as a compensating strength. Self-employed and gig buyers usually show income through two years of tax returns and bank statements, which underwriters scrutinize closely. A score comfortably in the very good tier (740+) gives the file a cushion that can offset variable income, where a 660 score plus irregular deposits invites tougher conditions. For this profile, aiming higher than the minimum is not vanity; it is leverage.

Thin-file and new-to-credit buyers

If you have little credit history, the issue is less "what is a good score" and more "do I have a usable score at all." Conventional and FHA lenders can use manual underwriting with alternative tradelines such as rent, utilities, and insurance payments. Building three to six months of on-time history on a single account often produces a first score in the fair-to-good range, enough to start the FHA path.

How to reach the next credit tier before you apply

The fastest way to move up a pricing tier is to cut your credit-card utilization and stop opening new accounts in the months before you apply. None of these steps require gimmicks:

- Lower your utilization. Pay revolving balances below 30%, and ideally under 10%, of each card's limit. This is the change that moves a score quickest, often within one statement cycle.

- Make every payment on time. Payment history is the largest single factor in the score. One missed payment can undo months of progress.

- Do not open new credit. A new card or auto loan adds a hard inquiry and lowers your average account age right when a lender is looking (CFPB).

- Dispute errors. Pull your reports and challenge inaccuracies; a single corrected late payment can lift you across a breakpoint. Medical collections deserve a close look here, since recent scoring changes affect whether medical bills hurt your credit score.

- Keep old accounts open. Closing a long-held card shortens your history and raises utilization, both of which can cost you points.

For a deeper plan, see our guide on how to boost your credit score. And if you want to understand how a lender actually reads your file beyond the score, our explainer on what an underwriter does in a mortgage loan walks through the full decision.

A good credit score to buy a house, in the end, is the one that lands you in the best pricing tier you can realistically reach: 740 or above for the floor on rates, with 670 to 739 still firmly "good" enough to own a home. Knowing where the breakpoints sit turns a vague target into a specific, affordable goal.