When is the next Bank of Canada interest rate announcement?

The next Bank of Canada interest rate announcement is Wednesday, June 10, 2026, at 9:45 AM Eastern Time. It is the fourth of eight fixed announcement dates the Bank of Canada has published for 2026 (Bank of Canada). The current policy rate sits at 2.25% following the April 29, 2026 decision to hold (Bank of Canada).

The Bank of Canada moved to a fixed-date system in 2000. Every rate decision now lands on a Wednesday at 9:45 AM ET, and the full schedule is published the previous August so households, lenders, and markets can plan around it.

The full 2026 schedule

The eight announcement dates for 2026, ordered by date:

| Date | Day | Time (ET) | Publication | Press conference |

|---|---|---|---|---|

| January 28, 2026 | Wednesday | 9:45 AM | Rate decision + Monetary Policy Report | Yes, 10:30 AM ET |

| March 18, 2026 | Wednesday | 9:45 AM | Rate decision only | No |

| April 29, 2026 | Wednesday | 9:45 AM | Rate decision + Monetary Policy Report | Yes, 10:30 AM ET |

| June 10, 2026 | Wednesday | 9:45 AM | Rate decision only | No |

| July 15, 2026 | Wednesday | 9:45 AM | Rate decision + Monetary Policy Report | Yes, 10:30 AM ET |

| September 2, 2026 | Wednesday | 9:45 AM | Rate decision only | No |

| October 28, 2026 | Wednesday | 9:45 AM | Rate decision + Monetary Policy Report | Yes, 10:30 AM ET |

| December 9, 2026 | Wednesday | 9:45 AM | Rate decision only | No |

The four dates marked with a Monetary Policy Report (MPR) include a longer statement, updated forecasts, and a press conference with the Governor at 10:30 AM ET. The other four dates release a short press release only.

Where the policy rate stands right now

As of June 1, 2026, the policy rate is 2.25%, the Bank Rate is 2.50%, and the deposit rate is 2.20%. The Bank has held at 2.25% since April 29, 2026, when it cited heightened global volatility, rising oil prices pushing March CPI to 2.4%, and modest GDP growth of 1.2% for 2026 as reasons to keep rates steady (Bank of Canada). For how today's 2.25% compares with earlier rate cycles, see what the interest rate was in past decades.

How does the Bank of Canada decide whether to change rates?

A six-member Governing Council reviews economic data and votes on the policy rate at each scheduled meeting. The decision is grounded in the Bank's mandate to keep annual CPI inflation at 2%, the midpoint of a 1% to 3% control range agreed with the federal government. The Governing Council includes the Governor, the Senior Deputy Governor, and four Deputy Governors, all appointed for fixed terms.

The Council's job is to forecast where inflation will be in 18 to 24 months and set the policy rate so that the forecast lands near 2%. The mechanism linking that rate to prices is explained in why lower interest rates cause inflation. The Bank publishes its own projections four times a year in the Monetary Policy Report.

What the Council looks at

The main inputs to a rate decision are:

- Inflation: Statistics Canada's monthly CPI release, plus core measures (CPI-trim, CPI-median, CPI-common) that strip out volatile components.

- Labour market: the monthly Labour Force Survey from Statistics Canada, including the unemployment rate, employment growth, and wage growth.

- GDP and output gap: quarterly GDP, plus the Bank's own estimate of how much slack remains in the economy.

- Global conditions: the US Federal Reserve's policy stance (see when the next Fed rate decision is scheduled), commodity prices (especially oil for Canada), and trade policy developments.

- Financial conditions: bond yields, the Canadian dollar, credit growth, and household debt.

The blackout period

In the week before each announcement, the Bank of Canada enters a communications blackout period. During that time, the Governor, Senior Deputy Governor, and Deputy Governors do not give speeches or interviews about monetary policy, the economic outlook, or financial markets (Bank of Canada). The blackout for the June 10, 2026 decision starts Wednesday, June 3, 2026.

The point of the blackout is to prevent any signal that could move markets ahead of the official announcement, which is published at the same moment to all market participants at 9:45 AM ET.

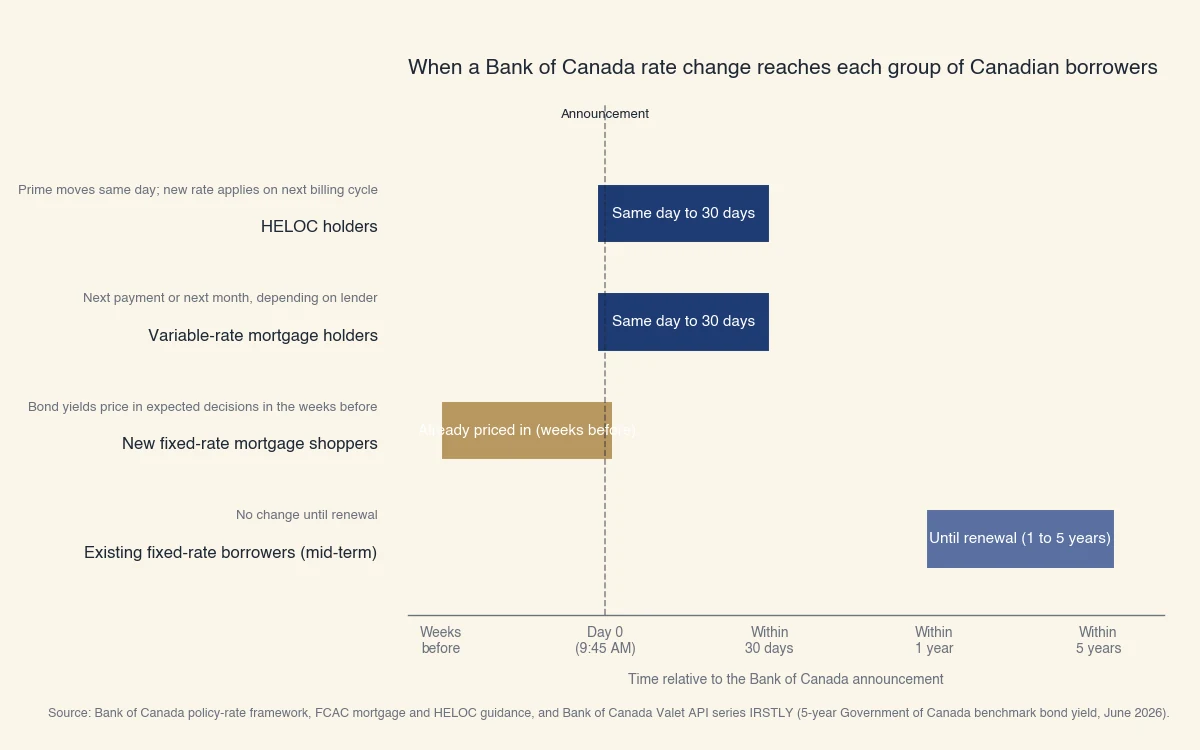

Who is actually affected on announcement day?

An announcement-day rate change affects three groups of borrowers very differently. Variable-rate and HELOC holders feel the change almost immediately. New fixed-rate borrowers usually see little change at the moment of the announcement, because bond markets price in the expected decision weeks ahead. Existing fixed-rate borrowers in the middle of a term see no change until renewal. Understanding which group you are in is the difference between a useful decision and a panicked one.

Source: Bank of Canada policy rate framework, FCAC mortgage guidance, and Bank of Canada Valet API series IRSTLY (5-year Government of Canada benchmark bond yield), June 2026.

Group 1: HELOC and variable-rate mortgage holders

The fastest channel. Canadian chartered banks set their prime rate at the policy rate plus a spread that has been 220 basis points since 2020. When the Bank of Canada moves the policy rate, the major banks almost always match within hours.

A variable-rate mortgage priced at "prime minus 0.50%" means: if prime moves from 4.45% to 4.20% following a 25-basis-point cut, your mortgage rate moves from 3.95% to 3.70%. Depending on the lender, the new rate applies on the next payment date (adjustable-rate variable) or stays the same payment with a longer amortization (fixed-payment variable, where the principal portion shrinks instead).

A home equity line of credit (HELOC) is priced at prime plus a spread, usually prime plus 0.5%. The new rate applies starting the next interest billing cycle, typically within 30 days.

Group 2: People shopping for a new fixed-rate mortgage

The slowest channel for a known event, and the fastest for a surprise. Five-year fixed mortgage rates in Canada follow the 5-year Government of Canada bond yield, not the policy rate directly (Bank of Canada). The bond market is forward-looking: if traders expect a 25-basis-point cut at the next meeting, they bid bond prices up and yields down in the weeks leading up to the meeting.

The result is counterintuitive: a widely-expected cut may move the 5-year bond yield by almost nothing on announcement day, because the cut was already priced in. A surprise decision (a cut nobody expected, or a hold when a cut was expected) moves the bond yield meaningfully and shows up in fixed-rate mortgage offers within a few days.

For fixed-rate shoppers, the practical implication is that "lock my rate the day before the announcement" is usually a coin flip. The expected outcome is already in the rate sheet.

Group 3: Existing fixed-rate borrowers mid-term

No impact until renewal. A homeowner with three years left on a 5-year fixed mortgage is unaffected by the June 10 announcement. The rate, the payment, and the amortization schedule are all locked in until renewal.

The announcement only becomes relevant at renewal time, when the new offer will reflect whatever bond yields are doing then.

Savers see the mirror image. When the Bank cuts, the yield on high-interest savings accounts and TFSAs falls too, which is why the banks paying the highest TFSA rates tend to trim them within days of a cut.

How much could your mortgage payment change?

On a $500,000 mortgage with 25-year amortization, a 25-basis-point cut from 4.50% to 4.25% lowers the monthly payment by roughly $72. A 50-basis-point cut lowers it by roughly $144. A 25-basis-point increase raises the payment by the same amount in the opposite direction. These figures use the standard Canadian mortgage amortization formula and assume semi-annual compounding (FCAC).

The math, for a single example. The standard monthly payment on a fixed-rate mortgage is:

P = L · [ i · (1 + i)^n ] / [ (1 + i)^n - 1 ]

where L is the loan amount, n is the number of monthly payments, and i is the monthly periodic rate. For Canadian mortgages, i is derived from the semi-annual posted rate, not the simple monthly rate. At an annual rate of 4.50%, the effective monthly rate i is approximately 0.003715, and the monthly payment on $500,000 over 300 months is roughly $2,770.

A 25-basis-point change in the policy rate that fully passes through to a 4.25% mortgage rate gives i ≈ 0.003510 and a payment of roughly $2,698, a saving of about $72/month or $864/year.

A 50-basis-point pass-through (mortgage rate of 4.00%) gives a payment of roughly $2,626, a saving of about $144/month or $1,728/year.

A 25-basis-point increase has the opposite effect, raising the payment from $2,770 to about $2,842, an extra $72/month.

The cumulative effect over a five-year term, before considering rate resets, is roughly $4,300 to $8,600 in interest difference per 25-basis-point step on a $500,000 balance. Larger balances scale linearly.

When the math actually applies to you

These figures only apply to mortgages that reprice on announcement day. For variable-rate borrowers, that is the next payment after the policy rate change. For new fixed-rate shoppers, the bond market has usually moved already, so the rate you see on June 10 incorporates much of the expected decision. For existing fixed-rate borrowers, the math only matters at renewal.

What time is the announcement and where can you watch it?

The Bank of Canada publishes the rate decision at exactly 9:45 AM Eastern Time on the announcement date. On the four MPR dates, the Governor holds a press conference at 10:30 AM ET, livestreamed on the Bank of Canada website. June 10, 2026 is a rate-decision-only date, so there is no press conference; the next press conference is July 15, 2026.

The schedule by minute, on a typical announcement day:

- 9:45 AM ET: Press release published on

bankofcanada.ca. The release states the new policy rate, the Bank Rate, the deposit rate, and a paragraph or two of reasoning. - 10:30 AM ET (MPR dates only): Press conference begins. The Governor reads a prepared opening statement, then takes questions from financial-press journalists for about 45 minutes.

- 11:15 AM ET (approximately, MPR dates only): Press conference ends.

The full press release is also distributed by newswire services. Major Canadian banks publish their updated prime rate within minutes of the announcement when the policy rate changes. If the Bank holds the rate, the bank prime rate stays at its current level.

What to do (and not do) on announcement day

For most borrowers, the right action is the same on every announcement day: understand which group you are in, check whether your lender has updated rate sheets, and avoid making impulsive locking decisions on the morning of the announcement. The bond market has had weeks to price in the expected decision; the announcement itself is rarely the right trigger to switch products, refinance, or break a mortgage.

The exception is if the decision was a surprise. If economists expected a hold and the Bank cut by 50 basis points, bond yields will likely move quickly and fixed-rate offers will follow within a few business days. In that situation, asking your lender for an updated quote a few days after the announcement is reasonable.