Does Klarna affect your credit score in Canada?

In most cases, no. Using Klarna's Pay in 4 plan with on-time payments does not affect your credit score in Canada, because Klarna uses a soft credit check at signup and does not report on-time installment payments to Equifax Canada or TransUnion Canada. The picture changes for two cases. First, Klarna Financing (the longer-term, interest-bearing product) uses a hard credit pull that can knock 5 to 10 points off your score temporarily. Second, any Klarna payment that goes 30 or more days past due can be sent to a collections agency, and that collections entry can stay on your Canadian credit file for six years (Equifax Canada).

The short answer below covers most readers. The detailed sections that follow walk through each Klarna product, the dollar math on a worked example, and a counterintuitive point about whether BNPL is actually building your Canadian credit file in 2026.

The 30-second version

- Pay in 4 and Pay in 30: soft check only, no bureau tradeline, no credit-score impact if paid on time.

- Klarna Financing: hard pull at application, opened tradeline on your file, monthly payments reported.

- Late payments past 30 days: collections entry possible, six-year retention.

- On-time positive history: usually not yet reported in Canada (2026), unlike the US and UK where Klarna started reporting in 2024.

How does Klarna's credit check work by product?

Klarna runs a soft credit check for short-term plans like Pay in 4 and Pay in 30, and a hard credit pull for its longer-term financed loans. A soft credit check is a record that only you and the lender doing the check can see. It does not appear on the version of your file other lenders pull, and it does not affect your score. A hard credit pull appears on the version other lenders see and can lower your score by 5 to 10 points for several months (FCAC).

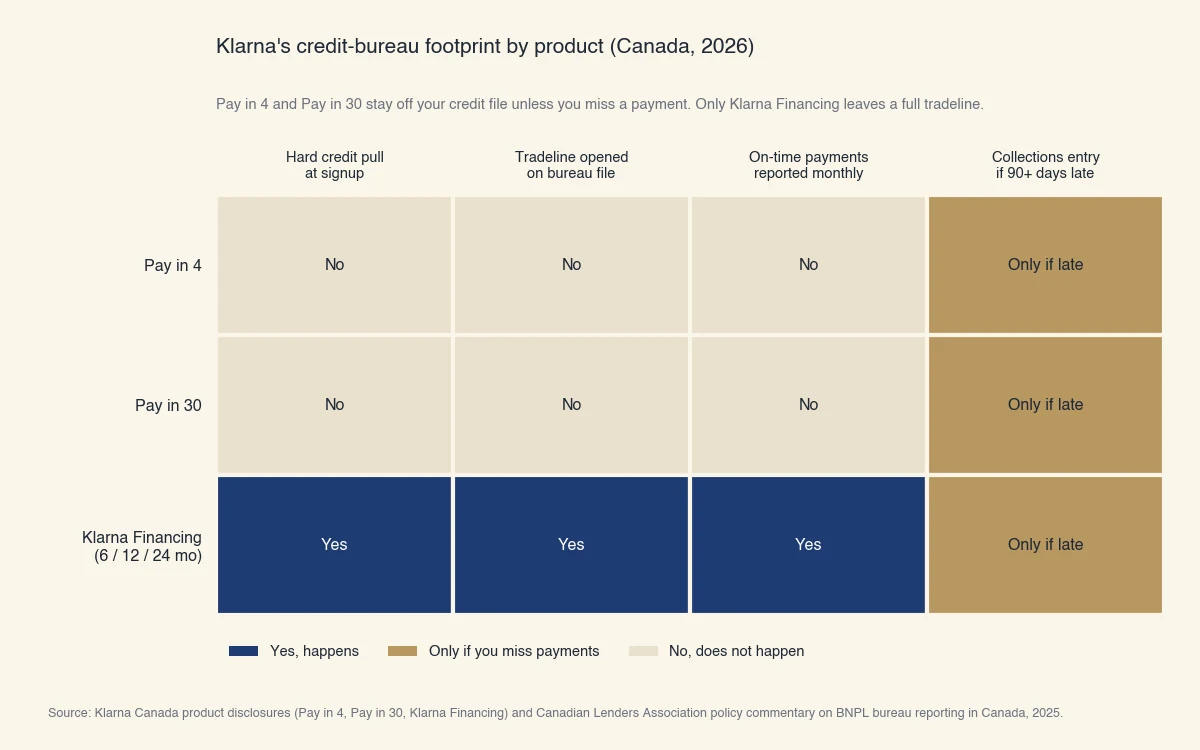

This is the table that does the heavy lifting on this page. Confirm which Klarna product you are about to use before you tap "Confirm purchase."

| Klarna product | Credit check at signup | Reported as a tradeline to Canadian bureaus | Reported on-time payments | Reported late payments | Late fee (CAD) |

|---|---|---|---|---|---|

| Pay in 4 (4 installments over 6 weeks, 0% APR) | Soft | No | No | Only if sent to collections | Up to $7 per missed installment (Klarna CA) |

| Pay in 30 (single payment within 30 days, 0% APR) | Soft | No | No | Only if sent to collections | Up to $7 |

| Klarna Financing 6 months (interest-bearing) | Hard | Yes | Yes, monthly | Yes, monthly | Varies by lender partner |

| Klarna Financing 12 months (interest-bearing) | Hard | Yes | Yes, monthly | Yes, monthly | Varies by lender partner |

| Klarna Financing 24 months (interest-bearing) | Hard | Yes | Yes, monthly | Yes, monthly | Varies by lender partner |

Pay in 4 is Klarna's flagship product in Canada. It splits a purchase into four equal installments, collects the first at order, and the remaining three every two weeks. The annual percentage rate is 0% and the late fee is capped at $7 CAD per missed installment, never exceeding 25% of the installment (Klarna Canada).

Klarna Financing is a different product. It uses a partner lender, runs a hard credit check, and opens an installment loan tradeline on your bureau file. The APR varies based on your credit profile and the term length. On a financed plan, every monthly payment is reported, which means on-time payments help your file and missed payments hurt it.

Why soft pulls don't move your score

A credit inquiry is the bureau's record of someone checking your file. The bureaus track two types. Soft inquiries are invisible to other lenders and are never used in scoring models. Hard inquiries are visible to other lenders for two years and counted in scoring models for the first 12 months. The FICO and Equifax Canada methodology both weight inquiries at roughly 10% of the score, and the typical impact of a single hard pull is 5 to 10 points (FCAC).

Klarna's Pay in 4 uses a soft pull because the credit risk Klarna is underwriting (six weeks, four payments, $200 average ticket) does not justify the hard-pull friction. Klarna's interest-bearing Financing product underwrites a real installment loan with months or years of duration, so the hard pull is justified by the credit exposure.

When can Klarna hurt your credit score? A worked example

The realistic worst case is a Klarna Financing application followed by a missed payment that crosses the 30-day past-due threshold. The combined hit is typically 65 to 110 points on a previously-good Canadian credit file. Here is the math, walked step by step.

Imagine Maya, a 28-year-old in Montreal with an Equifax Canada score of 720. She decides to finance an $1,800 laptop through Klarna's 12-month financing plan. The APR is 19.99%, the monthly payment is about $167, and the lender partner runs a hard credit pull.

Step 1: the hard pull. A single hard inquiry on a clean file drops the score by 5 to 10 points. Maya's score moves from 720 to about 712.

Step 2: the new tradeline. Opening a brand-new installment loan with zero history briefly drops the "length of credit history" and "new credit" factor inputs. The typical impact is another 5 to 10 points. Maya is now around 705.

Step 3: first three months on time. Three months of on-time payments slowly heal the new-credit hit. Maya recovers about 5 points to roughly 710.

Step 4: the missed payment. In month four, Maya forgets a payment. Klarna's lender partner reports it as 30 days past due to Equifax Canada in month five. On a previously-good file, a single 30-day delinquency can drop the score by 60 to 100 points (Equifax: late payments). Maya is now around 620.

Step 5: the collections risk. If Maya does not bring the account current and the balance is sent to a third-party collections agency at 90 to 180 days past due, a separate collections tradeline lands on her file. That entry stays for six years from the date of first delinquency (Equifax Canada).

The total realistic damage from one missed payment on a financed Klarna plan is therefore in the range of 65 to 110 points off Maya's original 720. That is the difference between a prime mortgage rate and a subprime mortgage rate, on a $400,000 mortgage that is roughly $20,000 to $40,000 in extra interest over a five-year term.

By contrast, if Maya had used Pay in 4 for a $240 purchase and paid on time, none of this would have happened. There would be no hard pull, no tradeline, no reporting. If she had missed one Pay in 4 installment but caught up within 10 days, the only consequence would have been a $7 late fee. If she had let that installment go past 30 days and Klarna had sent the balance to collections, the same six-year collections entry would apply, but the $60 outstanding balance makes that scenario much less likely to escalate that far. Either way, a single late payment is one of the most common reasons a credit score drops.

Does Klarna build your credit in Canada? The misconception explained

No. In Canada in 2026, on-time Klarna Pay in 4 payments do not build your credit history, because Klarna does not yet report positive Pay in 4 activity to Equifax Canada or TransUnion Canada. This is a common misconception in BNPL discourse, and it is mostly wrong in the Canadian context right now.

Here is what is actually happening. In the US, FICO announced its FICO Score 10 BNPL and FICO Score 10T BNPL models in mid-2025, which incorporate BNPL loan data into the score for the first time (FICO). Klarna started reporting US customer activity to TransUnion in 2024. In the UK, Klarna began reporting to Experian and TransUnion in June 2022.

Canada is moving more slowly. The Canadian Lenders Association notes that BNPL data in Canada is "still voluntary, variably reported, and not uniformly incorporated into underwriting, creating potential pitfalls for both borrowers and lenders." Equifax Canada has begun ingesting BNPL data into consumer files and TransUnion Canada is "not far behind," but the Financial Consumer Agency of Canada is still in the pilot-research phase on regulatory guidance (CLA).

What that means for a Canadian reader in 2026:

- Even if Equifax Canada has Klarna data in its system, most Canadian lenders do not yet factor it into underwriting decisions.

- Responsible Pay in 4 use is not currently a credible way to build a thin credit file in Canada. A small secured credit card or a credit-builder loan is still the standard path. For the methods that do move a Canadian score, see how to increase your credit score in Canada.

- The asymmetry will probably narrow over the next two to three years as bureau ingestion and lender adoption catch up to the US and UK.

If your goal is to build credit, do not rely on Klarna Pay in 4 right now. If your goal is short-term cash-flow flexibility on a planned purchase that you will pay off in six weeks, Pay in 4 is genuinely zero-impact in Canada.

Source: Klarna Canada product disclosures (Pay in 4, Pay in 30, Klarna Financing) and Canadian Lenders Association policy commentary on BNPL credit-bureau reporting in Canada, 2025.

How does Klarna compare to Afterpay, Sezzle, and Affirm in Canada?

All four short-term BNPL providers use a soft check and avoid reporting on-time installments to Canadian bureaus, but they differ on optional credit-building modes, late-payment handling, and US-versus-Canada parity. Pick the comparison that matches the product you are actually about to use.

- Afterpay (Pay in 4): soft check, no tradeline, no on-time reporting. Late payments capped at 25% of the order value. Operates in Canada with similar bureau-reporting behaviour to Klarna Pay in 4.

- Sezzle (Pay in 4): soft check by default. Offers Sezzle Up, an opt-in product that reports on-time payments to TransUnion in the US. Canadian Sezzle Up rollout is limited and you should verify with Sezzle before counting on it for credit-building.

- Affirm: soft check for shorter plans, hard pull for longer financed plans. Affirm reports its longer financed loans to bureaus in the US. Canadian behaviour is more limited, similar to Klarna Financing.

- Klarna: covered above. Pay in 4 soft, Financing hard, on-time Canadian reporting still voluntary.

The pattern is consistent. Short-term, interest-free, four-installment plans (Pay in 4, Pay later style) use a soft check and stay off Canadian bureau files in 2026. Longer-term, interest-bearing financing uses a hard pull and opens a real tradeline that affects your score in both directions.

For more on a similar BNPL question framed for the US market, see does Affirm affect your credit score? and the underlying piece on how to check your credit score in Canada. For another everyday Canadian banking product, see whether an overdraft affects your credit rating. And because the real risk with any missed bill is a collections entry, it is worth knowing whether medical bills can affect your credit rating the same way.

How to use Klarna without hurting your credit score

Use Pay in 4 only for purchases you have already budgeted for, pay on the original due date, and avoid Klarna Financing unless you have already compared its APR to a low-rate credit card or line of credit. A short checklist:

- Confirm the product type before checkout. Pay in 4 is soft. Financing is hard.

- Set a calendar reminder two days before each installment date.

- Keep your linked debit card or credit card funded for the auto-pay attempt.

- If you do miss a payment, pay it within 10 days to avoid the $7 late fee and stay well below the 30-day delinquency threshold.

- Never use Pay in 4 to build credit. Use a secured credit card or credit-builder loan for that.

- Treat Klarna Financing like any other installment loan. Compare APR, term, and total cost against a low-rate credit-card refinance or a personal loan.

If you are not sure whether a past Klarna account ever reported to your file, request your free Equifax Canada or TransUnion Canada report. It will list every open tradeline and every collections entry currently on file.